An increasing number of India’s populace and small businesses from its rural hinterlands are coming online through a series of digital pushes, including programs like Digital India and Startup India. The world’s second-most populous country is now experiencing exponential growth in its digital lending sector, whose market size is predicted to exceed USD 100 billion by 2023, according to a joint report by Omidyar Network and Boston Consulting Group (BCG). And Alibaba-backed Paytm is the latest to tap into this rosy sector.

Paytm, the digital payment services provider, said on Tuesday that it has inked a partnership with Clix Finance, a non-banking financial company, to provide digital loans to consumers and small businesses via its platform.

The two companies said in a statement that they are using proprietary artificial intelligence technologies, such as “machine learning models” and “credit tested algorithmic lending products,” to aid the loan application and approval process. As a result, individual consumers and India’s millions of MSMEs, or micro, small and medium enterprises, would get instant digital loans from Paytm’s service offerings. This includes post-paid deferred payments and merchant lines, targetting consumers and merchants respectively.

Nitin Misra, Paytm’s senior vice president, said that the company has seen significant responses to its postpaid and merchant lending services, and aim to bring their new AI-powered offerings to a larger customer and merchant base.

There are more than 60 million MSMEs In India, and they are playing an important role in the country’s GDP growth. However, they are usually underfunded due to insufficient financial access to traditional banking channels despite their significance in the economy.

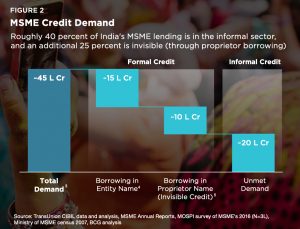

Due to the lack of proper and convenient access to loans, almost 40% of Indian MSMEs chooses to raise cash from informal sources and have to pay interest rates that are usually 250% higher than what proper channels would charge.

The Omidyar and BCG report estimated that in 2018 the Indian MSMEs total credit demand is USD 600 billion. However, according to Roopa Kudva, Omidyar’s India partner and managing director, most of the demand for that amount is “being met through informal sources”.

The financing conundrum has given rise to India’s fintech industry. Over the last seven years, the same BCG report states that more than 1,000 fintech startups have been established in India, with a total of USD 2.5 billion of venture capital being raised.

The tie-up between Paytm and Clix echoes a previous report by The Economic Times saying that Paytm might transfer its online loans businesses, including its Post-Paid operation, to Clix Capital. People with knowledge of the matter quoted by ET suggested that the move could be the result of regulatory scrutiny. KrASIA has reached out to Paytm for a comment.

The rumor came on the heels of a case of public interest litigation being filed with the Delhi High Court against Paytm, which has been accused of skirting lending regulations.

The Reserve Bank of India (RBI), the country’s central bank, forbids the extension of credits to clients by payments banks.

India’s payments bank came into birth under the inclusive financial idea. RBI approved the first batch of 11 entities, including the Department of Posts, also known as India Post, and mobile carrier Airtel, to start payments banks in India.

A payments bank, is usually smaller than but similar to a traditional banking institution in many ways except for one major difference: it is not supposed to extend any form of loans or issue a credit card, which is also a form of loan.

Paytm isn’t the only firm that has dipped its toes into India’s lucrative digital lending sector. Ola, India’s answer to Uber, also launched its credit product Ola Money Postpaid, giving its passengers a 15-day billing cycle. Ola has applied for a non-banking lending license from the RBI, according to multiple media reports.

Paytm has been taking cues from its backer Alibaba to branch out into a variety of businesses in India, with mixed results, from mobile payment to e-commerce and wealth-management. The company currently claims more than 300 million registered users in the country.