The Indian smartphone industry that bore the brunt of the two-month-long nationwide lockdown followed by the economic slump in the second quarter of 2020, is expected to make a recovery in the second half of the year on the back of pent up demand. Amazon India and Flipkart’s sporadic sales events, and festive season sale that usually kicks off starting September would also help the sector get back on track.

According to the data collated by various research firms, the smartphone shipments in India declined by over 50% in the three months ended June. The major reason for this poor performance in the world’s fastest-growing smartphone market was the disruption in supply chain and curtailed domestic production in the first half of the quarter due to the lockdown.

Massachusetts-based research and consulting firm International Data Corporation (IDC) on Friday said India’s smartphone market registered a sharp year-on-year (YoY) decline of 50.6% in the second quarter to 18.2 million units.

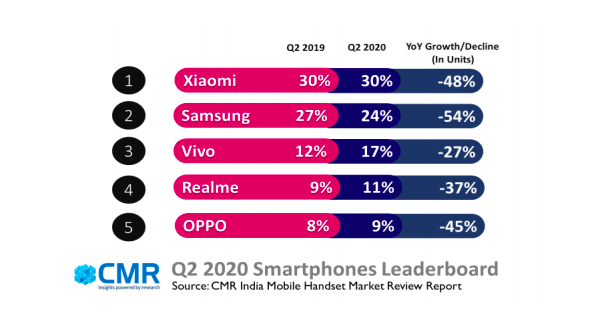

Gurugram-based CyberMedia Research (CMR) said the smartphone market slumped by 41% quarter-on-quarter (QoQ), and 48% YoY, while Hong Kong-based research firm Counterpoint pegs the fall at 51% YoY to just over 18 million units sold in Q2 2020.

“The quarter was marred by both demand and supply constraints which led OEMs to rethink their go-to-market strategies,” Prachir Singh, Senior Research Analyst at Counterpoint Research, said in a note. “On the supply side, the factories were shut down in April and started operating in May, which resulted in supply shortages for some manufacturers. Some brands maintained the supply of their products by importing fully assembled handsets.”

Meanwhile, IDC stated, brands were forced to increase prices due to the GST (Goods and Services Tax) hike in April and the depreciating rupee.

“Vendors faced major supply chain disruptions at the beginning of the quarter, and the shortage continued into the rest of the quarter as factories operated at partial capacity even after the lockdown was lifted,” IDC noted in the report. “Components and parts remained at the ports waiting to be cleared, especially for China-based vendors.”

However, by June, as the country opened up, sales increased due to the pent-up demand from the lockdown period, IDC said, adding, these purchases were mainly driven by availability rather than choice.

According to Amit Sharma, Manager-Industry Intelligence Group, CMR, the initial consumer demand in the unlock phase was driven predominantly through online channels and driven by need for urgent replacements.

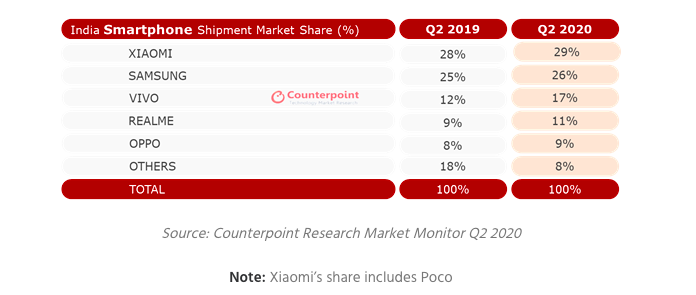

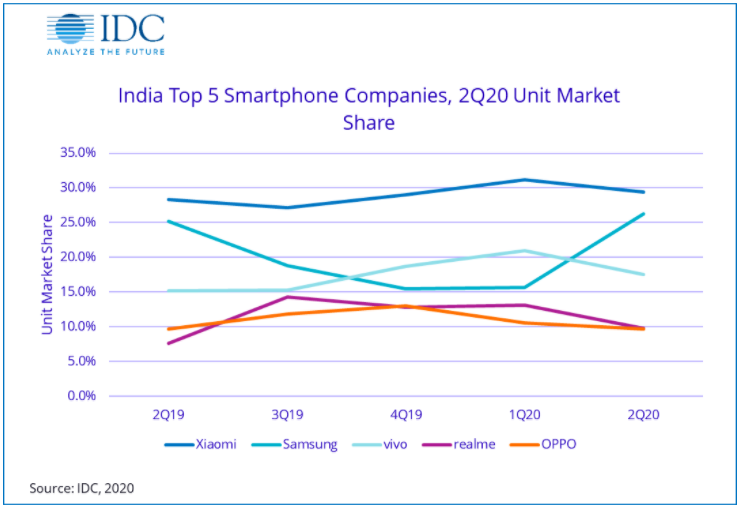

Data collated by IDC, CMR, and Counterpoint shows Xiaomi continued to be the number one player, with about 29% market share, followed by Samsung and Vivo. While IDC and Counterpoint put Samsung’s market share at roughly about 26%, CMR data puts it at 24%. Vivo, on its part, holds approximately 17% market share.

The combined market share of Chinese smartphone brands, which have been on a growth trajectory in India since 2017, also saw a fall.

“The contribution of Chinese brands fell to 72% in Q2 2020 from 81% in Q1 2020,” stated Shilpi Jain, Research Analyst at Counterpoint Research.

According to Jain, this was mainly due to stuttering supply for some major Chinese brands such as Oppo, Vivo, and Realme. Growing anti-China sentiment and delay in the import of goods from China amid extra scrutiny also led to the slump in sales, she said. “This all resulted from the India-China border dispute during June.”

Analysts believe Samsung has emerged as a beneficiary of the challenges being faced Chinese smartphone brands However, CMR said almost three in four phones shipped in the Q2 were still Chinese.

“With a resilient supply chain, Samsung was able to arrest its declining market share and improve upon its market share,” said CMR’s Sharma. “It remains to be seen if Samsung is able to maintain its market performance in the coming quarters, garner consumer demand, and compete against, and challenge the dominance of Chinese smartphone brands.”

The optimistic outlook

According to Navkendar Singh, Research Director, Client Devices & IPDS, at IDC India, the supply chain challenges forced brands to go for direct imports to meet the pent-up demand in June, which added extra cost pressures.

“IDC expects the market to show signs of recovery in the second half of the year, as we approach the festive quarter with the majority of the consumers looking to buy low-end and mid-range devices,” he said. “However, this will be dependent on brand marketing and channel initiatives, especially by e-tailers during the festive sales.”

CMR believes the mobile market will improve in mid-Q3, spurred by early online sales fests, setting the smartphone market on a potential path to recovery towards the festive season. The Bengaluru-based research firm estimates the market to recover by over 40% in H2, in comparison to H1.

“The path to potential recovery will be led by pent-up consumer demand, driven by the need for upgrades,” said CMR’s Sharma. “In the run-up to the festive season, consumers will seek to go for meaningful value propositions, that bring devices and compelling content ecosystem offerings, together.”