Inke, a Chinese mobile live streaming platform, is set to list on the Hong Kong Exchange (HKEx) in a public float forecast to raise up to HK$1.21 billion ($152.9 million) and its shares priced between HK$3.85 to HK$5, according to details in its prospectus.

The midpoint of the initial public offer (IPO) price range will see it float with a market capitalisation of $1.2 billion, while media reports cited by Smartkarma, a Singapore-based investment research platform that services asset managers, suggest that at the upper end of its public float, it could raise up to $300 million in capital, with IPO proceeds to finance business expansion, marketing and potential acquisitions.

Despite one analyst indicating the firm has a “healthy net cash position and positive free cash flow”, the assessment on Inke is negative due to being the only listed live streaming platform to report a decline in revenue, as well as reporting the lowest profitability amongst it listed live streaming peers, reflecting “lower scale and higher streamer payouts”, which is expected to see it profitability gap with its peers likely to expand.

The Hong Kong IPO will reportedly see it sell between RMB 9.6 to 11.2 billion worth of shares at about 12 to 14 times its price-to-earnings (P/E), raising between$200 to $300 million. The company reportedly commenced its international placement on 27 June, with its shares ready for subscription in Hong Kong since 28 June.

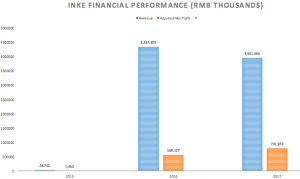

Founded in 2015, Inke lets Chinese youth view live karaoke singing among other live performances from their mobile devices. Details in its filing with the HKEx claim it was the second largest mobile live streaming platform in China by revenue in 2017, posting revenue of RMB 3.94 billion ($595 million) and holding 15.3% of the market.

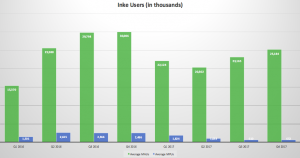

User-wise, its flagship Inke app’s monthly active users peaked in Q4 2016, preceding a 26% decline in early 2017 from 30 million to 22 million, though its earnings have been on the increase since Q2 2017, with Q1 2018 seeing its monthly active user base standing at 25.3 million individuals.

The company is currently at a pre-profit stage, with its losses for the year narrowing to RMB 239 million in 2017 from RMB 1.5 billion in 2016 following reductions in sales & marketing expenditures and its adjusted profit increasing to RMB 791 million from RMB 568 million.

However, the company saw its revenues decrease to RMB 3.9 billion in 2017 from RMB 4.3 billion in 2016.

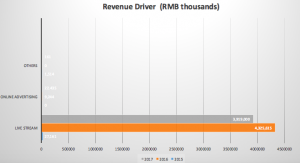

Currently, its business model sees it generates most revenues from its live-streaming business; users purchase its virtual currency, Inke Diamonds, in order to access virtual items and services while virtual items streamers receive can be converted to Inke Coins and can be exchanged for RMB up to a point.

Chinese live streaming platforms tend to rely on virtual gifting, a process in which users send virtual gifts to others via in-app purchases while hosts can enhance the viewing experience by buying interactive stickers.

Inke initially filed for an IPO in March 2018, while its competitor Huya listed on New York Stock Exchange (NYSE) earlier in May in a public float that has seen its share price rise from $23.27 to a peak of $48.57 on 18 June, with the shares trading on the NYSE at $32.10 as at 2 July.

Despite its revenue and operating profit growing over the last three years – its revenue increasing by 136 times that of 2015’s revenue and operating profit surged to 541 times that of 2015’s operating profit – it has seen a 10% decline in revenue, withs its operating profit seeing reduced growth in the 2016/2017 period.

Details in its IPO prospectus indicates this declining performance is rooted in the past eight quarters seeing a decline in the volume of monthly active users, as well as paying users. Despite the overall growth in its number of monthly active users, it posted a 16% YOY decline in the number of monthly active users.

Unlike other social networking platforms, Inke monetises through a paying user base rather than the use of targeted advertising; its base of monthly active paying users has declined 60% over the past two years.

This suggests that future profitability will be impacted, given its declining user base and competition with other social networking platforms such as Douyin and Weishi. The company also has to deal with broader market conditions, which have reached an inflection point and is seeing greater consolidation among live streaming operators, as well as regulation from Beijing aimed at curbing undesirable content.