China Renaissance, China’s boutique investment bank, filed Monday with the Hong Kong Exchanges and Clearing (HKEX) for an upcoming IPO tipped to be as early as October this year.

BAO Fan, the founder and CEO of China Renaissance, has revealed in the company’s prospectus the purpose of this listing. He sees a 2018 IPO as timely for the investment bank to keep pace amidst the growing appetite and pace amongst Chinese unicorns. The company’s calling to champion the causes of entrepreneurs and new businesses remains to be the key driver for the company’s future growth.

While no explicit numbers were mentioned in its initial prospectus, the company is rumored to be looking to raise as much as $800 million with the Hong Kong bourse – making it the third HKEX IPO for this year.

The funding will be used to make hires, develop new services and invest in the technology and infrastructure, as well as, finance overseas businesses as some of its clients are mulling over cross-border businesses. Words on the street are that the bank has been considering launching businesses in Southeast Asia as a slew of Chinese tech giants and startups are increasingly making their impacts in the region.

Some of the joint sponsors include Goldman Sachs and ICBC International.

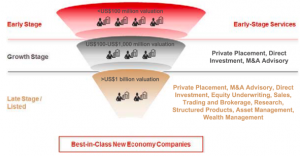

China’s largest new economy investment bank

Bao Fan, an ex-investment banker with notable American banks such as Morgan Stanley and Credit Suisse, founded China Renaissance and has led his company in a stellar growth trajectory thanks in part to its unique positioning to dedicate itself to China’s new economy businesses.

China Renaissance’s growth is also a reflection of the Middle Kingdom’s prosperous new economy, driven by the likes of Didi, Meituan and Xiaomi, all are the boutique bank’s clients.

This boutique investment bank has three core business lines namely investment banking, investment management and Huajing Securities.

Per its prospectus, by 2014, it was already ranked first place among the list of banks to assist Chinese companies selling their share in the U.S.

It is a significant private equity financing player in China, accounting for 20% of the country’s private equity deals.

Furthermore, in China’s merger and acquisition sector, it also accounts for a whopping 12% of China’s M&A market. Some examples of its notable M&A participations include the likes of Meituan-Dianping (former Group buying platform Meituan & Yelp-like website Dianping) and Didi Chuxing (former Didi Dache and arch-rival Kuaidi Dache).

That said, its financial performance over the past three years from its prospectus seems to tell but a different story.

Weakening financial performance

While adjusted revenue grew by an eye-popping 47.2% from 2016 to 2017, the firm’s revenue barely grew from 2015 to 2016.

China Renaissance’s adjusted profit, on the other hand, fell by 21% from 2015 to 2017. The marginal USD3 million improvement from 2016 to 2017 was a far cry from the huge profits back in 2015 at USD73 million.

Importantly, this trend seems like its going to persist. In 2015, profits make up more than 50% of its revenues but this ratio has since fallen to just close to 39% for Q1 this year. The lowest profit margin was registered in 2017 at a low 27%.

The dismal financial performance could be attributed mainly to poor investment banking performance and the loss-making multi-licensed platform.

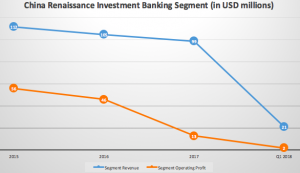

Poor investment banking performance due to previous IPO drain

Investment banking was the key driver of China Renaissance’s revenue but has experienced the same declining trend in both its segment revenue and operating revenue.

The company itself explained in the prospectus that the revenue sliding is due to the transaction volume drop in 2016 and 2017, and to cope with that, it has expanded its services of scope to cover early-stage startups, scale up equity research, and extend sector coverage.

Despite the fact that Q1 2018 actually roped in higher revenue compared with a year ago, specifically a 40% year-on-year growth, the cost too also grew larger, resulting in only marginal improvements in its operating profits.

It still remains to be seen whether the firm’s investment strategies during this time of market adjustments would propel it for further future growth.

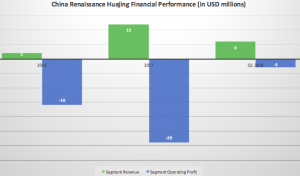

Huajing’s Losses

This was a new investment by China Renaissance, Wuxi-based investment firm and Shanghai Enlight Investment Holding Co to serve the nation’s new economy and to get ready for the long-term growth opportunities in China’s onshore securities.

Like all initial long-term investments, the losses have been burgeoning since its inception in late 2016. However, a silver lining exists – its revenue is on the rise.

This quarter, for instance, Huajing has already made half of last year’s revenue.

In spite of this weak profitability and mounting losses in its latest investments, China Renaissance has the comparative advantage like no other – both in its expertise in China and the U.S. and also the knowledge in technology firm. This itself can be the moat against other financial veterans in the market.

Most importantly, in its prospectus, it was highlighted that in 2015 – markets were favorably buoyed by strong market momentum and the market now has entered into the ‘adjustment phase’.

Amidst rife speculations of the drying up of capital markets in Hong Kong, this latest bid towards IPO might just be what China Renaissance to expand beyond the shores of China and cement its dominance at home, awaiting the returns from its series of investments into the long-term technology trend.

Editor: Ben Jiang