Chinese companies have long been the scrutiny of corporate fraud and malfeasance. However, the recent scandal involving Luckin Coffee, an upstart domestic rival to Starbuck, along with allegations against iQiyi, a popular Baidu-owned video platform accounting for around a quarter of Baidu’s revenue, has shaken international investor confidence.

Amidst a broader downturn for Chinese ADRs in the US, a capital market rebalancing may occur, with mainly Chinese companies opting for domestic exchanges to avoid stigmatization and enhanced scrutiny from the US investor community. In fact, China-based companies listed in the US this year are trading at 12% below their IPO price on average, compared to an average decrease of 7.5% for all listed companies.

Following the Luckin Coffee (NASDAQ: LK) scandal involving RMB 2.2 billion in fabricated revenue, the China Securities Regulatory Commission (CSRC) announced an investigation into the company. The concerning trend raises questions as to how and why Chinese companies are so frequently engaging in fraud, and what regulatory policies can make a difference going forward.

The slew of Chinese startups seeking to raise capital in the US is unabating, as a total of 67 Chinese companies have listed on either the Nasdaq of the NYSE since the beginning of 2018, with notable names including Tencent Music Entertainment (NYSE: TME), social e-commerce company Pinduoduo (NASDAQ: PDD), promising streaming platform Douyu TV (NASDAQ: DOYU), and China’s leading podcast platform Lizhi (NASDAQ: LIZI).

For companies currently listed in the US, and those in China seeking to become part of what has previously been a prestigious group, the recent fraud scandals may impact the future of cross-border capital markets between the US and China.

“It will certainly shake investor confidence and makes it harder for Chinese companies to seek IPO in the US. We may see a new wave of going private deals for ADR companies,” China Renaissance CEO Fan Bao said, as reposted by Bloomberg TV anchor Selina Wang on Twitter.

Cross-border securities frauds are nothing new

As the ashes of the 2008 financial crisis cooled, Chinese companies listed in the US were particularly resilient to the recession, continuing to post growth in revenue and earnings while the rest of the market was paralyzed. As domestic companies stagnated, famished US investors satiated their hunger by buying into China’s growth story and the glut of new publicly-listed firms that followed. However, unlike Hong Kong investors who have decades of experience conducting due diligence on Chinese firms, US investors were largely unfamiliar with the potential warning signs that some mainland Chinese companies exhibited.

In 2011 and 2012, over 100 Chinese firms were delisted or suspended from US exchanges for accounting fraud or other corporate malfeasance, destroying nearly USD 40 billion in market value. Many of these scandals were the result of reverse mergers, where a private Chinese company would be acquired by an already listed “shell” corporation.

Amidst cries for increased cooperation amongst governing bodies, China’s regulators offered in July 2013 to release audit working papers to the US Securities and Exchange Commission (SEC) on a case-by-case basis.

By 2014, Chinese company IPOs in the US hit an all-time high, raising USD 29 billion, largely helped by Alibaba’s blockbuster USD 25 billion IPO in September 2014 on the NYSE. The second highest peak was in 2018, when USD 9 billion was raised by Chinese firms on US markets. With some of the biggest names in China tech yet to complete IPOs including ByteDance and Didi Chuxing, what impact will the latest wave of fraud scandals have on the future plans of ambitious Chinese firms?

High-profile cases

Luckin Coffee’s growth story sounded almost too good to be true. From founding to Nasdaq IPO in 18 months, and set to displace Starbuck’s stranglehold on the Chinese coffee sector, Luckin Coffee was the newest darling of China’s tech startups before it spectacularly crashed under the weight of its latest accounting scandal.

US investors were bullish on Luckin prior to the scandal, and many wondered what product would be the next on-demand delivery sensation in China. Luckin even did well to compensate for China’s relative lack of enthusiasm for coffee, branching out to offer food items as well as teas and other beverages to increase their customer base.

Buoyed by their volume-centric business model which featured Luckin kiosks strategically located near massive office plazas and shopping malls, Luckin seemed set to reach profitability in 2020 and provide industry incumbent Starbucks a real headache. Instead, Luckin now represents a cautionary case to Chinese firms looking to list abroad.

Right on the back of Luckin’s disaster, Baidu’s iQiyi (NASDAQ:IQ) was the target of a short report from Wolfpack Research which accused the firm of fabricating DAUs as well as revenue. Wolfpack Research had previously gone after Shanghai-based news aggregator Qutoutiao (NASDAQ: QTT), releasing a short report on December 10, 2019. However, despite requiring two weeks to formally rebut the report, the short attack had little to no impact on Qutoutiao’s stock price, which even increased until the global sell down incurred by the COVID-19 pandemic.

Qutoutiao’s resilience to Wolfpack Research’s short report is likely a good indication for iQiyi, although the company has still not provided a detailed rebuttal of the report as of April 22. Muddy Waters Research, the due diligence firm responsible for first exposing Luckin Cofee’s scandal, has backed Wolfpack Research and endorsed a short position on iQiyi.

Despite Muddy Waters Research staking its credibility on Wolfpack’s claim, the short report fell short of being utterly convincing. On the first charge that iQiyi overstated their DAU numbers, Wolfpack compared their DAU projections based on just four days of sampling data. In their analysis, Wolfpack proceeded with the assumption that iQiyi disclosed 175 million average mobile DAUs in October 2019. However, in October 2019, iQiyi’s chief content officer Xang Xiaohui disclosed that iQiyi had 175 million daily active independent devices, which differs from the mobile DAUs metric specified by Wolfpack Research. Given the longer-form style of iQiyi’s content, it is logical that a more significant portion of DAUs could use devices including TVs, laptops, and tablets.

Further evidence of fabricating user numbers, according to Wolfpack, is on iQiyi’s own popularity heat map, which displayed provinces with low populations in the top charts such as Inner Mongolia, Macau, and Hainan. Alleging the use of click farms, Wolfpack asserted that due to the sparse population in these areas, the heat maps must be indicating fraudulent activity, instead of perhaps using a viewership per capita to create the heat map, which would then explain the presence of low population areas in the top charts.

iQiyi has managed to weather the hit for now, with its stock even increasing in the days following the report’s release on April 7.

Future for Chinese companies seeking IPOs abroad

Amidst the recent shift in investor’s sentiment and major regulatory scrutiny, many firms in China that previously targetted IPOs in New York are now likely to shift plans to domestic exchanges in Hong Kong or Shanghai. Hong Kong’s stock exchange has been overshadowed recently by the debut of the Shanghai’s Nasdaq-like STAR market, which in the first quarter of 2020 topped the global leader board as a total of 33 companies raised USD 7.31 billion, besting New York and Hong Kong exchanges.

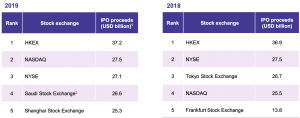

Traditionally, the Hong Kong Stock Exchange has led the way, topping the charts for IPO proceeds in 2018 and 2019. However, in 2019, the mainland Chinese Shanghai Stock Exchange ranked fifth in total funds raised. If the NYSE and Nasdaq become increasingly inhospitable places for Chinese companies to go public, firms will be left with a choice between the up-and-coming Shanghai Stock Exchange or the traditional route to Hong Kong, which has seen massive Chinese tech giants like Tencent, Xiaomi, and Meituan-Dianping all thrive.

(left) and 2018 (right) Source: KPMG

For the next generation of Chinese tech giants seeking an IPO, it seems that the glamour of the New York listing may be fading. The Financial Times reported in October of 2019 that the world’s most valuable startup, Bejing-based ByteDance, was considering a public offering in Hong Kong, but a company spokesperson denied the reports of a planned Hong Kong IPO in the first quarter of 2020. ByteDance, responsible for hugely successful apps in China like Jinri Toutiao and Douyin, as well as international sensation TikTok, has come under intense scrutiny from US regulators touting user security and privacy concerns.

Another major name in Chinese tech, Megvii, an industry leader in artificial technology including computer vision and facial recognition, is set for a USD 500 billion IPO in Hong Kong. Similar to ByteDance, the firm faces scrutiny from US regulators and was placed on a US trade blacklist in October of 2019.

Zhu Ning, deputy dean at Shanghai Advanced Institute of Finance at Shanghai Jiao Tong University told Forbes that “there is no denying that investors are now doubting Chinese companies, especially those touting high growth and new business models.”

However, the negative sentiment is not shared by all. Before the latest wave of fraud scandals, Charlie Munger, vice chairman at Berkshire Hathaway and longtime business partner of Warren Buffett, recently said at the Daily Journal Corp’s annual meeting that, “the strongest companies in the world are not in America,” adding that “Chinese companies are stronger than ours and are growing faster,” CNBC reported.

Since the genesis of the US-China trade war, the world’s two most dynamic technology ecosystems have begun to decouple, with certain Chinese firms restricted from access to US components, including Google Mobile Services, resulting in Chinese firms trying to become self-sufficient in technology, for example Huawei, which is now producing its own microchips and operative systems.

The latest wave of Chinese fraud on US exchanges comes at a sensitive time in the economic relationship between the US and China, while the concentration of power in global capital markets may shift towards Chinese exchanges, some analysts appointed. As the global economy plots a revival following the COVID-19 pandemic, the new reality of a post-virus era may well be a further polarization of capital markets, with Chinese firms viewing domestic exchanges as the most attractive option for their public offerings.