Pinduoduo founder Colin Huang’s latest April 2020 letter to his shareholders is a strange but sincere creature. Penned from the confines of his home during the COVID-19 lockdown, he muses on the new normal following the coronavirus outbreak in an almost philosophical way. Huang breezily peppers his letter with discussion on Newtonian physics and equations, before rounding off with casual Latin and French.

It is clear that Huang’s mind works rapidly and in a remarkably different way. Little wonder, then, why he chose “Costco+Disney” as Pinduoduo’s defining tagline in the company’s prospectus and his 2018 letter to shareholders, raising the eyebrows of investors and consumers alike.

At first glance, the direct references to Costco (NASDAQ: COST) and Disney (NYSE: DIS) are shocking, possibly even discomforting. It is common for aspirational startups to make reference to established companies, with hot favorites being Uber and Google as reference points to attract investors looking for the next unicorn (“the Uber of home cleaning” and “the Google of dating”, for example). However, it is less common and possibly even a faux pas for mammoth companies such as Pinduoduo to do so when defining business strategy, especially in official marketing and listing documents.

Why then, does Pinduoduo hold on so strongly to its tagline? What is it trying to achieve, and is this sensible? Let’s find out.

Why Costco?

According to Huang, the allusion to Costco and Disney represents “value-for-money and entertainment” combined. Costco is a fixture in America’s retail landscape. It began operations in 1983 and has since blossomed into a sprawling enterprise comprising at least 785 warehouses globally.

Like Costco, Pinduoduo’s selling point is its ability to offer consumers a vast assortment of quality goods at extremely low prices. Costco adherence to this strategy is reflected in two rules: first, gross profit margins never exceed 14%, and second, if a product is stocked at a lower price elsewhere, Costco will stop stocking it themselves. Likewise, Pinduoduo’s appeal largely arises from its low prices and selectivity in stock-keeping units (SKUs) in order to improve the efficiency and quality of its supply chain.

In some ways, however, the allusion to Costco does not make sense. Pinduoduo leverages network effects and asset-lightness, with a business model that is quite different from Costco’s, which relies on formal membership and heavy capital expenditure for its warehouses.

Pinduoduo undersells itself when it comes to highlighting the cost savings of its e-commerce operation. Costco is very much a brick-and-mortar operation. It aims to increase the number of direct-owned warehouses it owns, rather than rents. Net cash used in investing activities, which primarily consists of capital expenditure on new and remodeled warehouses, has increased steadily over the years and shows no signs of stopping.

Pinduoduo, in comparison, operates on an asset-light model with no plans to open its own warehouses or operate its own logistics fleet. The firm’s cash investing activities mostly involve short term investments (i.e. highly liquid investments in wealth management products in financial institutions). In addition, a quarter of Costco’s sales come from its in-house brand, Kirkland, while Pinduoduo has no obvious plans to enter into the first-party retail relationship market, unlike its competitor JD.com (NASDAQ:JD).

Pinduoduo could also be attempting to emulate Costco’s success in retaining customers. The platform has a 7-day retention rate of 77%, which surpasses that of other e-commerce players in China, although Taobao and JD.com come close at 75% and 70% respectively. This metric tracks just how many users still use an app a week after dowloading, and is a key predictor of customer lifetime value for e-commerce.

However, much of Costco’s retention durability comes from its membership model, which is designed to reinforce member loyalty in a very visible way. This is a fundamental value driver Pinduoduo lacks.

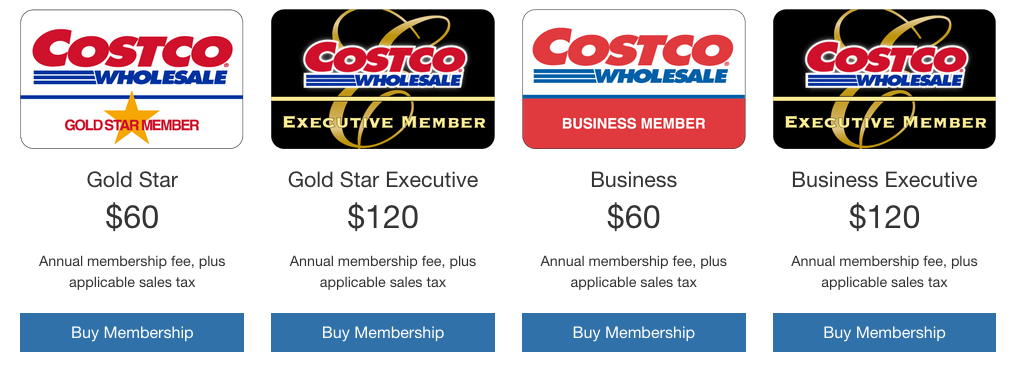

In North America, annual membership fees are USD 60 for normal memberships and USD 120 for executive memberships, with executive members forming 39% of paid members as of 2019. Aside from the benefits reaped by normal members, executive members can get access to complimentary household cards, 2% cashback, and additional savings on numerous other Costco services ranging from real estate programs to roadside assistance.

Sinking money into memberships generates immediate revenue for Costco at a low cost. In 2019 alone, membership fees generated USD 3.3 billion in upfront revenue for Costco. Although merchandise sales formed the bulk of revenues, with membership fees forming an unassuming 2.24% percentage of net sales, this was achieved at a significantly higher cost.

Net sales generated USD 149.3 billion in revenues but at merchandising costs of USD 132.8 billion and selling, general and administrative expenses of USD 14 billion. Costco’s membership model is not a fad: in 2019, it had stunning 91% member renewal rates in the US and 88% globally.

For all of Pinduoduo’s success, it lacks this key value driver that sets Costco very much apart from the flock.

In picking from a menu of value-driven American retailers, Pinduoduo has stayed far away from Walmart (NYSE: WMT). It may be more similar to Pinduoduo as it similarly lacks a reliance on the membership model while emphasizing cost savings, although Walmart has made fitful attempts at starting a membership program (Walmart+) in March 2020. However, Costco’s fresh face in China is also more appealing than Walmart’s rocky road into the country involving mishaps such as food safety issues, poor consumer understanding, labor unrest, and government friction.

Understandably, Pinduoduo kills two birds with one stone with its heavy-handed Costco allusions. Foreign retail investors struggling to make sense of a strange Chinese company instinctively understand Costco and what it is trying to do. What better to ingratiate itself with American investors than a good pinch of wholesome American enterprise?

Within its domestic market, China, Costco also holds luster. One need only remember Costco’s phenomenal success when it set up its store in West Shanghai in December 2019 (such as its 139,000 membership sign-ups on its first day and aisle fights over cartons of Maotai) to realize its appeal even to the average Chinese consumer.

One hundred and one half-priced Dalmations

Pinduoduo’s self-characterization as a Disney imitator is far stranger than its association with Costco. At a stretch, Disney’s tagline, “the happiest place of earth”, possibly holds water when applied to Pinduoduo. Pinduoduo could very well be Disney to middle-aged folk whose idea of a dream come true is scoring a good deal on 50 pieces of fresh-picked cabbage. However, Disney’s mission is to be a mass media company, ostensibly far away from Pinduoduo’s e-commerce ambitions.

Pinduoduo’s ability to leverage the social aspect of commerce, however, stands out from other e-commerce giants. It saves money on marketing costs by turning customers into marketers: the more people one can get to join their shopping group, the cheaper the price of an individual unit will be. This creates an inbuilt frenzy among users to recommend products to those in their social circle.

The unbelievable price of goods is also an addictive form of retail therapy. As anyone who has used Pinduoduo will tell you, its colorful user interface, constant notifications, and time-sensitive deals are all meant to enhance user time spent on the app.

Huang is also no stranger to the world of entertainment. A serial entrepreneur, his third company, Shanghai Xunmeng, was a gaming studio and is currently owned by Pinduoduo’s variable interest entity, Hangzhou Aimi. Duo Duo Orchard is an in-app feature that enables users to grow virtual fruit trees after amassing points through purchases. This joins a series of similar orchard-themed games pushed by Taobao’s Gold Manor Garden, JD.com’s Bean Farm, and AliPay’s Ant Forest, which seem to have struck a chord with consumer preference for games involving the cultivation of crops.

Pinduoduo has also ventured into the livestreaming short-video space, suggesting that its 2018 reference to Disney was either prophetic or strategic. Its biggest competitor may not only be other e-commerce behemoths such as Taobao and JD.com, but also ByteDance and Kuaishou.

ByteDance, in particular, is seeking partners to grow its e-commerce presence. Kuaishou, China’s second-largest short-video platform, has also set an annual target to have live streamers on its platform sell merchandise worth RMB 250 billion (USD 35.2 billion) in 2020. In view of these new competitors, Pinduoduo’s pivot to entertainment is not a moment too late.

In its first-quarter 2020 earnings call, Pinduoduo emphasized that its livestreaming service was found to be particularly effective in lowering consumer aversion to purchasing certain premium categories of goods online, such as high-end jade and Argentine shrimp.

This dovetails with their goal of increasing Average Revenue Per User (ARPU), which has always lagged behind its peers. Pinduoduo’s ARPU growth for 2019, however, increased 53% year on year and outpaced its active user growth (40%). This is an optimistic indicator of its ability to penetrate populations in higher-tier cities with more purchasing power.

Huang, in particular, made mention of how livestreaming was made available to seven major museums worldwide in order for representatives to sell souvenirs to international consumers. Pinduoduo also made broad references not just to livestreaming as a sales channel, but a channel for “shar[ing] personal experiences” and “interact[ing] with [the] users”, hinting at potential entertainment ambitions in the future.

Staying away from Groupon

When explaining Pinduoduo to non-locals, most Chinese prefer to allude to it as the “Groupon of China” rather than borrowing the Costco+Disney tagline preferred by Pinduoduo. So why does Pinduoduo omit official reference to Groupon (NASDAQ: GRPN) when it clearly does not shy away from name-dropping?

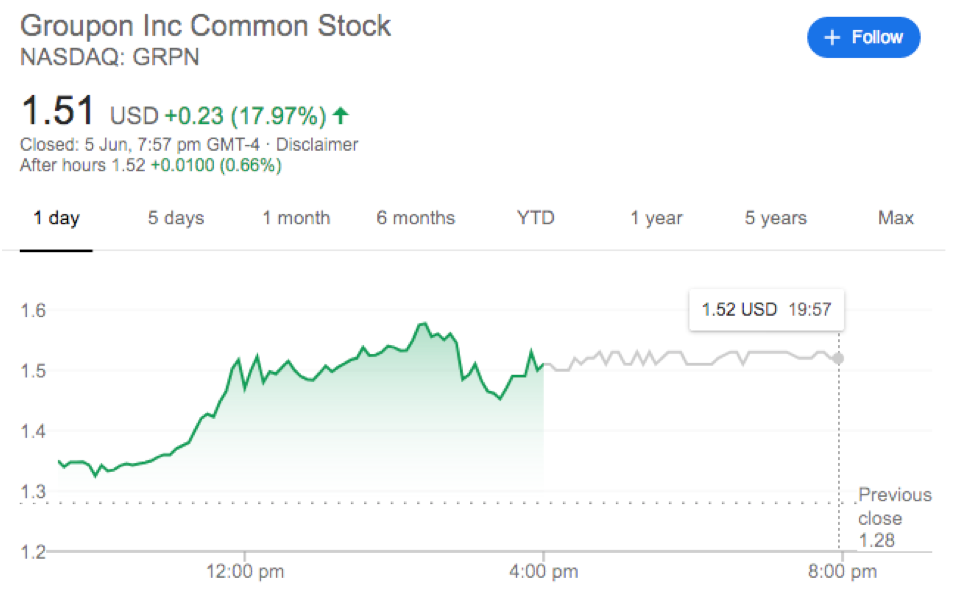

For one, Groupon is more of a has-been then an ascendant star. Making reference to Groupon might actually frighten investors. In 2011, Groupon’s stock traded at USD 28 during its initial public offering. Its descent in little more than nine years has been merciless, with the company’s stock trading at a little over a dollar as of June 2020.

Like Pinduoduo, Groupon relied on discounts and group buying to set it apart. Pinduoduo needs to be wary of rising sales and marketing expenses and control the quality of its merchants.

This is possibly why Pinduoduo is investing heavily in back-end services for merchants: one of the reasons why Groupon failed was the inability of small-business owners to handle large volumes of low-quality, low-margin customers when they flocked to the promise of discounts.

In addition, associating itself with Groupon might be too much of a pigeonhole for the Chinese model of business success to bear. Chinese giants, most notably the traditional BAT (Baidu (NASDAQ: BIDU), Alibaba (NYSE: BABA), Tencent (HKG: 0700), tend to expand horizontally to build ecosystems that augment their success. China’s business landscape is largely a series of proxy wars, with a scarcity of promising companies not at least partially owned by one of BAT.

Alibaba, for instance, started in e-commerce but has since evolved into a massive ecosystem. Even BAT’s newest challenger, ByteDance, has started eyeing edtech among other ventures. In contrast, American giants tend to explore within their core competencies.

Here today and still here tomorrow

The word “technology” itself appeared 106 times in Pinduoduo’s prospectus, compared to a modest 14 and 27 times in Costco and Disney’s 2019 annual reports respectively. In light of this, Pinduoduo’s preference for headlining with traditional companies like Costco and Disney is somewhat insincere.

There is some logic behind Pinduoduo’s self-labeling as a technology company. China’s hypercompetitive tech space crowds out would-be players, which would make differentiation difficult for a pure tech company.

This also sets it apart from the seasonal and the unsustainable: WeWork, for instance, infamously relied on its glorified space-as-a-service concept to trade on tech multiples and justify its massive USD 47 billion valuation. While WeWork’s main product was office space, it tried to set itself apart from traditional real estate by hyping up its “purpose-built technology”, which ultimately led to it being decried by many as the most ridiculous would-be IPO of 2019.

Pinduoduo is doing the exact opposite of WeWork by being mainly a tech platform (“online marketing services” forms the bulk of its revenues) while trying to associate with a different peer group for easier differentiation.

This has its appeal. Compared to many a tech company that has come and gone, Costco has gotten the gold stamp of approval from legendary value investors such as Warren Buffett, who even went out on a limb to express public admiration for its Kirkland brand in 2019. Berkshire Hathaway’s (NYSE: BRK.A) vice-chairman, Charlie Munger, sits on Costco’s board and the company itself has owned the stock for the past two decades.

In fact, Pinduoduo’s core company value, in Chinese benfen, refers to an emphasis on value creation for consumers, honesty, and “doing things out of goodwill and do[ing] no evil.” This is perhaps another tip of the hat to Costco, whose motto is to “do the right thing.”

Associating with blue-chip “traditional companies” that have good fundamentals and a clear eye to profit (which is somewhat lacking among startups) clears the air for Pinduoduo to signal to investors that it is here to stay for the long run.

In the first quarter of 2020, Pinduoduo reported a net loss of USD 581.8 million, despite benefiting from a 108% increase in gross merchandise value year-on-year. In addition, the boost from COVID-19 may also be short-lived if Pinduoduo does not play its cards right.

Pinduoduo faces twin threats from Alibaba and JD.com in defending its core market (lower-tier cities) and expanding into a new market (higher-tier cities). Previously, the company also reported monopolistic behavior from unnamed competitors attempting to pressure merchants into exclusively operating on their platform.

In addition, Pinduoduo’s association with respected industry titans is a clever marketing move to consumers. Compared to e-commerce competitors such as JD.com, Pinduoduo struggles with reputational issues, with consumers having at worst, skeptical, and at best, mixed views on its reliability.

Zhu Qing, a one-time user of Pinduoduo, is not a big fan. “I bought an iPhone on Pinduoduo last year, but I do not think it is reliable. The iPhone was really too cheap, and it has some minor problems, so I am skeptical about whether it is the same quality as those sold in official stores.”

Some consumers, however, are more enthusiastic. “I bought a television from Pinduoduo last year, and it is still working!” said Zhong Zhifeng. “In fact, I bought many fans from them this year.” he brightly continues, offering me a glance at his multitude of Pinduoduo receipts.