Successful tech companies in Asia are dynamic entities, with some formidable startups debuting on public markets less than ten years after their foundation. Amid the breakneck pace of evolution, many tech founders have aimed to safeguard substantial voting rights in the company, even after an IPO, to preserve the company’s purpose and prevent investors from hijacking their creation. But what motivates founders to covet a majority say, and how do investors navigate this scenario?

One of the latest examples is Grab’s founder and would-be “CEO for life” Anthony Tan, who controls a whopping 60.4% of voting power in the company, despite owning just a 2.2% stake. He is not the only one, with Ant Group’s Jack Ma, Facebook’s Mark Zuckerberg, and JD.com’s Richard Liu each controlling over 50% of the voting rights at their respective companies.

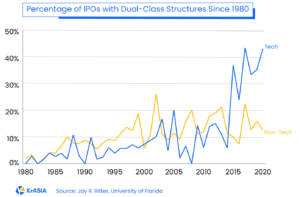

The new normal for tech IPOs

Let’s take a step back, and imagine you’re a founder concerned about protecting your vision for the company and staving off hostile takeovers, while still raising capital and holding a minority stake. What can you do? One way to build a moat around founders’ voices is to enlist dual-class or multi-class shares, granting them greater voting rights than other shareholders.

Since the 1980s, IPOs with multi-class stocks have been on the rise, and the change is even more dramatic in tech than in other sectors, breaching 42.9% of tech IPOs in 2020.

Finance professor Jay Ritter, also known as Mr. IPO, has tracked the rise of dual-class IPOs over several decades. He says although the arrangement isn’t ideal for shareholders, the high returns generated by many of these tech companies have persuaded investors to see past the matter.

“Historically, the returns on IPOs with dual-class stock have been about the same as with just a single class. If the returns were worse, investors would be demanding a bigger discount, and there would be more resistance to buying an IPO that had dual-class stock. But there has been enough success among dual-class companies, like when Google went public in 2004, and Facebook in 2012, so investors have gotten relatively complacent, and don’t demand a big discount in return for having inferior voting rights.”

Think of a founder of a well-known tech company that went public on a US exchange from the last few decades, and there’s a fair chance they’ve protected their voting rights in exactly this way. And it’s an increasingly familiar playbook for high-flying entrepreneurs the world over. Coinbase founder Brian Armstrong, for example, controls 52.2% of voting rights.

But Anthony Tan’s voting power in Grab still far exceeds that of many of his contemporaries. Consider for a moment, that Uber’s Travis Kalanick only held 16% of voting rights before his departure from the company. Didi Chuxing’s Cheng Wei, also looking to take his ride-hailing juggernaut public later this year, would control over 49.19% of the vote.

Southeast Asian companies also typically face more investor skepticism than US companies, which takes the form of a greater wedge or discount in shares without voting rights.

“If you look at Southeast Asia, there is a huge difference between shares that have voting rights and shares that have no voting rights. Because investors do not trust the founders as much as they trust in the North American companies,” said Anup Srivastava, a finance professor who co-authored a Harvard Business School case study on Snapchat’s IPO, which offered shares with no voting rights.

Who the founder is and how well they’re perceived matter more too, because “investors are taking a stake in the founder’s vision, his or her ability, as well as the extent that they have proprietary, specialized knowledge and vision,” said Srivastava. “At General Motors, the CEO comes and goes, but I can’t visualize Facebook without Mark Zuckerberg.”

What if the “benevolent dictatorship” isn’t so benevolent?

In interviews, Tan has sometimes referred to himself as a “benevolent dictator,” which represents a risk for investors.

When a company is so closely tied to the founder, and that founder’s reputation or leadership takes a turn for the worse, investors are left with little recourse. At JD.com, there wasn’t even a formal discussion about removing Richard Liu following serious allegations of sexual misconduct, because the board could not meet—there is a bylaw stating that no meeting can take place without the founder’s presence.

On the benevolent side, ISS, the world’s leading provider of proxy advisor services, found that a higher concentration of CEO voting power generally correlated with strong company performance and lower board turnover, but less board independence and lower gender diversity.

What to expect from Grab

“I can definitely see a scenario with a ‘benevolent dictator’ and employees who are concerned about job security, where dual-class stock might actually enhance firm value,” said Ritter. But there are costs to every benefit, in the form of discounts, among other things, meaning the company would pay a price for Tan’s control. And the fact that Grab is going public via a special purpose acquisition company (SPAC) doesn’t help either.

“The moment that I hear the company is trying to list via SPAC tells me there is something wrong with the company. This tells me they couldn’t have done it [otherwise],” said Srivastava. “Ideally speaking, when a company matures, like when Microsoft or Google matured, they should dilute the dual-class structure. With that said, it is very difficult to determine when a company has matured.”

While Grab has not even been around a decade before its debut on public markets, dual-class stocks concentrating voting rights in the hands of messianic founders are increasingly becoming a staple of the tech world, regardless of geography. Going forward, investors will likely have to accept a strategic backseat in favor of the strong performance tech stocks have displayed since the onset of the pandemic.