It was 2018 when Uber Technologies pulled out of Southeast Asia amid stiff competition with local ride-hailing players. Three years on, the company that took over Uber’s operations has grown into one of the region’s biggest tech groups, nearing a public market debut in the US.

When Grab begins trading on Nasdaq, it will not be a simple transport app. It will come with food and grocery delivery, payments, and insurance businesses, among others, making it a unique alternative for tech investors who might have liked stocks such as Uber, DoorDash, or China’s Alibaba and Didi Chuxing.

And Grab’s public market debut, which is expected by the end of the year via a merger with a special purpose acquisition company, could be only the start of a flood of US listings from Southeast Asia—home to about 650 million people—which has been underrepresented in the global market despite its potential.

In the small city-state of Singapore, the Grab app is a core part of life for many. Motorbikes and bicycles carrying green “GrabFood” delivery boxes zip through the streets, while restaurants and stores accept QR code-based payment via the GrabPay e-wallet. People use Grab’s ride-hailing services to make trips.

Grab started as a taxi booking app in 2012 in Malaysia. In its early days, it grew as a platform for hailing taxis, private cars, and motorbikes. Grab used this network of drivers to add on food delivery services. In tandem with mobile internet penetration in Southeast Asia and funding by prominent investors, including Japan’s SoftBank and Toyota, it expanded rapidly. Uber and Didi are also among Grab’s large shareholders.

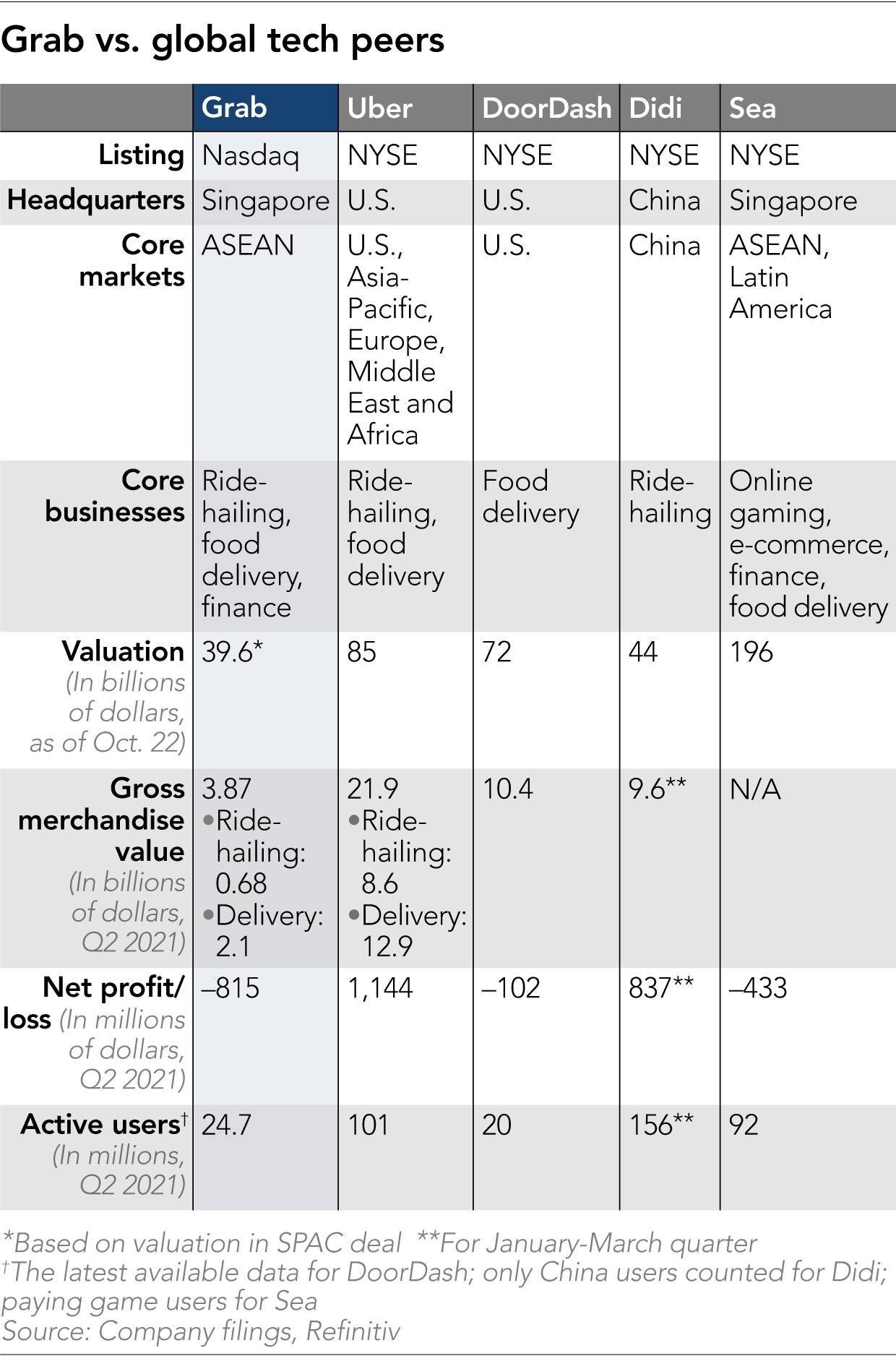

The company now operates in eight countries: Singapore, Malaysia, Indonesia, Vietnam, Thailand, the Philippines, Cambodia, and Myanmar. Grab had around 24.7 million active users in the second quarter of 2021, about 5 million registered drivers, and 2 million registered merchant partners.

In terms of market share, it accounted for 50% of food delivery in the region’s major six markets in 2020, leading Delivery Hero’s Foodpanda, Deliveroo, and others, according to Singaporean consultancy Momentum Works. Other research shows that Grab is the top ride-hailing service in most markets, while GrabPay has the leading share in e-wallets in Singapore and Malaysia.

“I think Grab right now is extraordinarily interesting for investors,” said Howard Yu, a professor at Switzerland’s IMD Business School who watches global tech companies. Beijing’s tech crackdowns have capped the share prices of companies like Tencent, Alibaba, and Didi, he said. “But any international investors, including institutional investors, have to diversify. They cannot put all their eggs in one basket, meaning the US. That makes Grab such an interesting alternative.”

At the same time, Grab’s wider range of offerings makes the company more attractive than its US peers, Yu said. “From a US investors’ angle, we’ve got to figure out the potential space for innovation in each of these companies. Uber is getting into UberEats, but they are not going to be able to go into finance as much as Grab because of regulation.”

The core of Grab’s growth is its superapp strategy, which offers various smartphone-based services. The app homepage shows different icons from “Food” and “Mart” (grocery delivery) to “Transport” and “Shopping.” The mass of data collected through transactions helps the company offer customized financial services such as “buy now, pay later” credit.

Grab won a digital banking license in Singapore, enabling it to take deposits and provide loans and other financial services, capitalizing on the consumer and merchant bases it established through existing businesses. These banking services are expected to launch next year.

“Each of our businesses helps the others scale,” CEO Anthony Tan said in an investor webcast in September, explaining the superapp strategy. “Our superapp flywheel allows us to grow the ecosystem in a vastly accelerated manner, versus other single-vertical players.”

In addition, Grab says it is well-positioned to capitalize on Southeast Asia’s rapid urbanization, supportive regulatory landscape, and large unbanked or underserved population. “Grab believes it is one of the most exciting and dynamic regions in the world,” it said in a US regulatory filing.

Still, Grab is relatively small compared to its US and Chinese peers in terms of financial numbers. For the three months through June, Grab’s gross merchandise value for its ride-hailing business—the total value of journeys made through the Grab platform—was USD 685 million, versus Uber’s USD 8.6 billion. The same metric for its delivery business was USD 2.1 billion, about a sixth of Uber’s USD 12.9 billion and a fifth of DoorDash’s USD 10.4 billion.

Regarding profitability, Grab reported a net loss of USD 815 million for the second quarter, versus Uber’s net profit of USD 1.14 billion and DoorDash’s net loss of USD 102 million, meaning Grab is prioritizing investments for top line growth. Grab’s accounting revenue also looks small—USD 180 million for the second quarter—as it is presented net of incentives for drivers, merchants, and consumers.

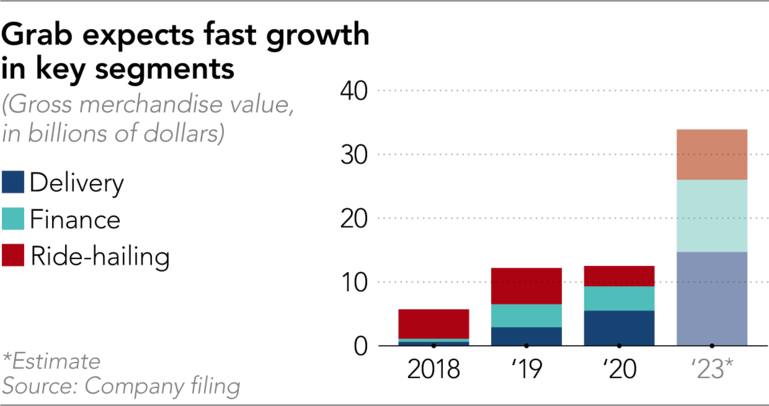

Its pitch to investors talks up a fast pace of growth that it expects to continue over the coming years. According to its own projection, Grab sees gross merchandise value nearly tripling to USD 34.2 billion in 2023 from USD 12.5 billion in 2020. That would represent a compound annual growth rate of 40% over the three years.

“I think Grab has the potential to grow more quickly [than global peers],” said Angus Mackintosh, analyst and founder of CrossASEAN Research. “You’re buying into a higher growth region generally with low rates of penetration for services, and Grab is also pursuing what they call a hyperlocal approach, which gives them access to a broad range of merchants and MSMEs. So, there’s potentially a very high long-term high growth story that you wouldn’t get with Uber and DoorDash.”

And, while investors want exposure to the high-growth Asian region, China presents too many risks, said Mackintosh. “Chinese companies have all been derated massively because of the scrutiny that’s going on within China. There’s still a lot of uncertainty, so I think that in a sense gives Grab an edge.”

But investing in Grab means being exposed to some risks. Southeast Asia’s internet services market size is expected to triple over the five years through 2025, according to projections by Google, Temasek Holdings and Bain & Co, but competition is also set to intensify, threatening Grab’s profitability.

Grab’s most prominent competitors include GoTo, an Indonesian tech group formed through a merger between superapp Gojek and e-commerce giant Tokopedia, which primarily focused on Indonesia, the biggest market in Southeast Asia. Singaporean tech group Sea is also heavily investing in finance and food delivery, and just last month announced plans to raise USD 6.2 billion to accelerate expansion beyond its home turf. Competitors are not only tech players. Malaysia’s AirAsia, which started life as a regional airline, is now investing heavily in food delivery, ride-hailing, and fintech with a superapp strategy of its own to challenge Grab.

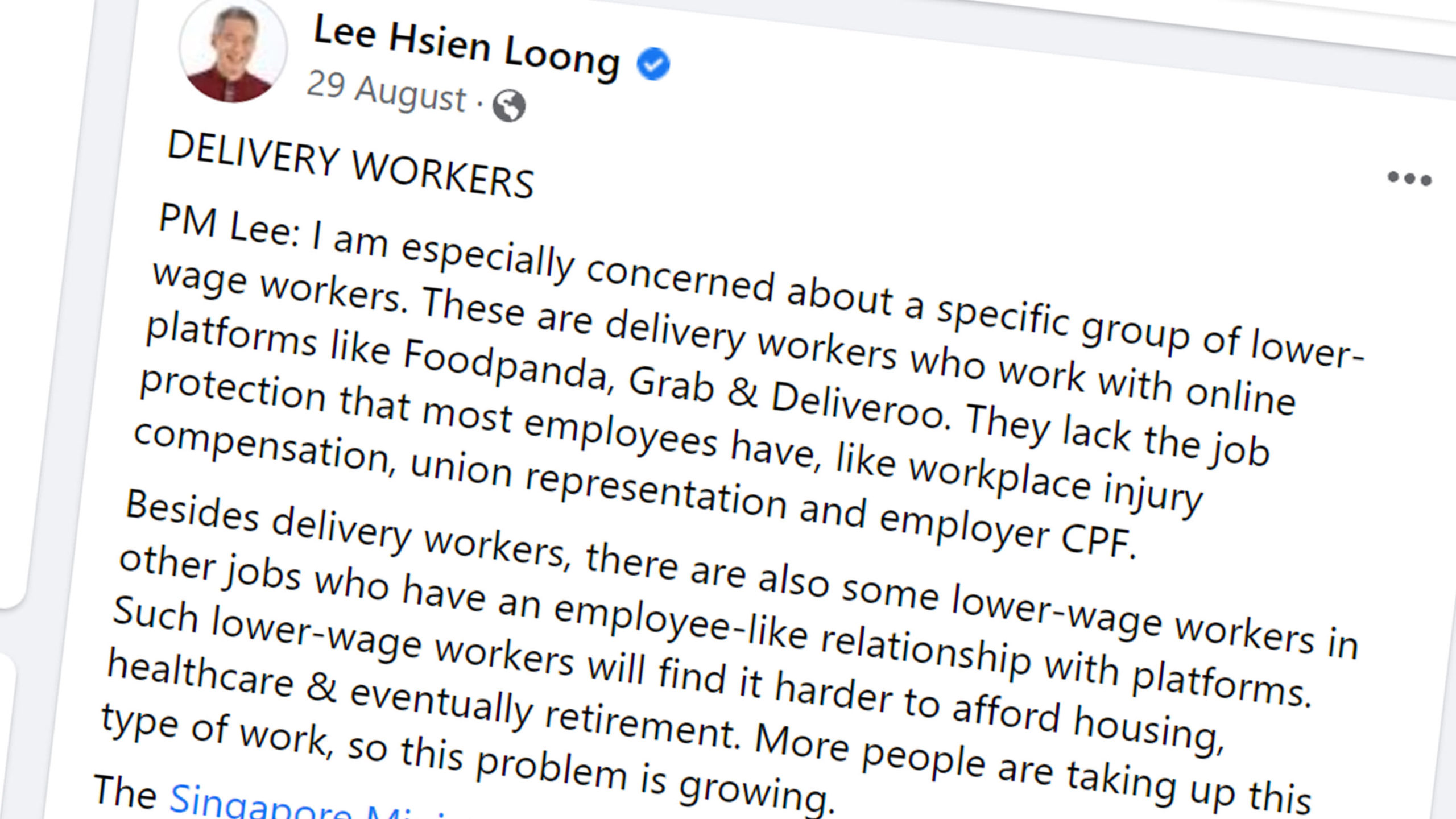

Regulators could also step up oversight of tech companies. In a recent development in Singapore, prime minister Lee Hsien Loong in August expressed concern about delivery workers’ low wages, calling for more protections. Such policies could drive up expenses for platforms like Grab.

COVID-19 also highlighted the region’s risks, with a slow start to vaccination programs resulting in long-term lockdowns, which affected many businesses, including ride-hailing. As a result, Grab in September downgraded its financial projections for this year—its earnings before interest, taxes, depreciation, and amortization is now expected to be in the range of minus USD 900 million to minus USD 700 million, down from the previous minus USD 600 million.

Last month, Grab said it was “on track” to complete its merger with Altimeter Growth Corp., a SPAC that valued Grab at nearly USD 40 billion, during the fourth quarter of 2021. US regulators have ramped up their scrutiny of SPAC deals this year but are working through a backlog.

Professor Yu argued Grab’s superapp strategy and nascent financial services business mean it could make bigger profits than its peers. “But it all depends on whether Grab could execute, implement and realize the strategy that they talk about,” such as the fintech businesses.

Meanwhile, Grab’s market debut could usher in more US listings from Southeast Asia, bankers say, particularly if it goes well. Currently, the only prominent Southeast Asian tech startup listed in the US is Singapore’s Sea, which is now valued at about USD 200 billion. As the region’s tech ecosystem grows, more companies are eyeing a US IPO, including Indonesia’s GoTo and other tech startups.

“There’s a long list of potential listings,” said Mackintosh at CrossASEAN Research, pointing out that companies would get higher valuations and more US tech investors than listing on Southeast Asian bourses. “Once you start to see a critical mass of listings in the US, then there could be a number of different unicorn companies that can move that way.”

This article first appeared on Nikkei Asia. It’s republished here as part of 36Kr’s ongoing partnership with Nikkei.