Zilingo, a B2B fashion e-commerce platform that’s nearing unicorn status, and Luxola, a cosmetics startup that was acquired by luxury brand LVMH might be among Wavemaker Partners’ better-known portfolio companies in Southeast Asia.

But the VC firm, which has one base in Singapore and another in Los Angeles, has developed a knack for investing in so-called deep tech startups—companies that are built around taking new, potentially patented, and highly disruptive technological innovations to market. At least 20% of its portfolio is made up of deep tech investments, while the rest comes from the enterprise and consumer space.

We asked Wavemaker managing partner Paul Santos about how deep tech investment opportunities can be identified in Southeast Asia, a region not known for making strides in R&D (with the exception of Singapore).

KrASIA (Kr): There seem to be different interpretations, ranging from narrow to broad, of what constitutes “deep tech.” What’s your definition?

Paul Santos (PS): We like to use the definition made by BCG and Hello Tomorrow, a non-profit initiative by science entrepreneurs: “Deep tech innovations are defined as disruptive solutions built around unique, protected, or hard-to-reproduce technological or scientific advances . . . They create value by developing new solutions, not only by disrupting business models.”

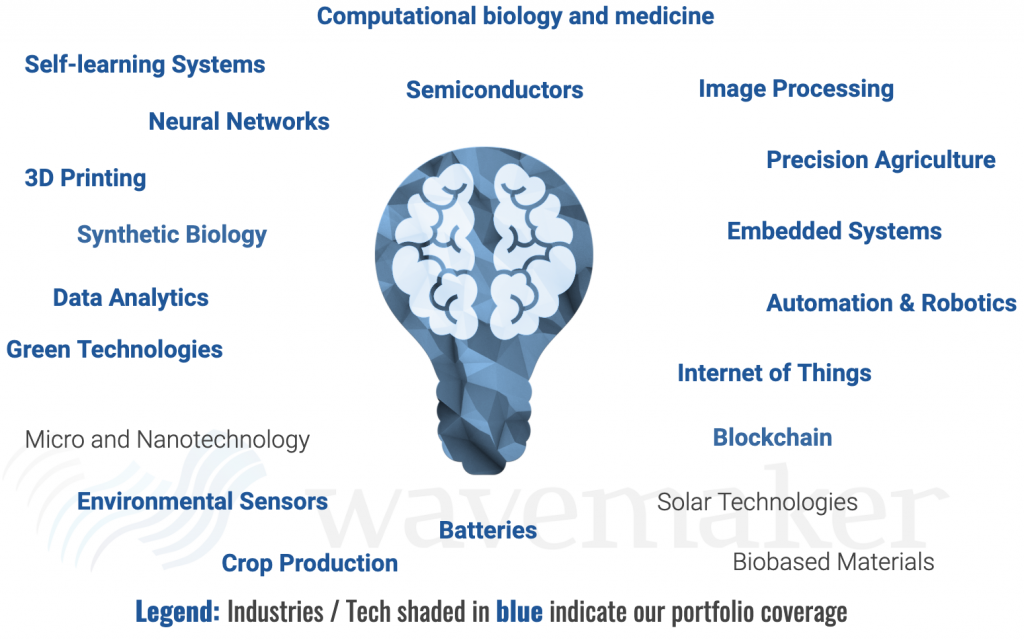

So for us, deep tech is more of an umbrella term. Here’s a working list of what our portfolio spans:

Kr: At least 20% of your investments are in deep tech. Do these startups have a different risk profile? How do you balance this?

PS: We believe every investment has a risk-reward ratio. The rewards for deep tech investments are potentially around:

- Defensibility

- Higher gross margins

- Favorable unit economics

- Higher customer lifetime value

- Exit potential

The risks are:

- Product risk—Will the tech work? Can it be scaled and/or mass produced?

- IP risk—Is it easy to copy or get around the IP? Could the IP actually infringe on someone else’s IP?

- Market risk—Will the market want the tech?

- Sales risk—Can the company sell? Can it close the big contracts?

These things take time. This is an inherent risk which many investors don’t like to take. It’s similar to how you need nine months for childbirth. You can’t get nine mothers to do one month each at the same time.

While we try to be patient, we also invest in deep tech that is closer to commercialization. Through the years we’ve seen that it’s not always the best technology that wins, it’s the technology that gets the most widely adopted.

Kr: At what stage in their life cycles do you normally first identify deep tech startups you are interested in, and at what stage is it then time to invest?

PS: Ideally, we would like to invest once the product and initial market are proven. We can invest earlier but our conviction around the uniqueness and value of the tech, as well as the path to commercialization, must be there.

Kr: For highly technical fields, how do you acquire the necessary skills to differentiate good solutions from truly brilliant ones? Do you have experts at your firm to help make those assessments?

PS: We recognize that technology advances at a rapid pace and that it will be difficult to have all the expertise we need in-house. This is why we leverage our network. We tap our advisors, who have deep domain expertise. We bring in co-investors (from local angels to global institutions and corporates). We can sometimes even get the help of some of our portfolio founders. Finally, we speak with the startup’s existing and/or potential customers. Their willingness to buy is usually a great sign that the company could be on to something.

Kr: Southeast Asia isn’t known for its strength in R&D. How and where do you find deep tech startups worth investing in? Is it all centered around Singapore’s top universities or are there less expected hubs?

PS: I guess we’ve built our reputation as active investors who are truly committed to this space, so the deal flow has been great. We’ve found deals from different places. Structo [a 3-D printer maker] was started as a side project by NUS students. Attonics [a firm that makes spectrometers] and Glissade [scanners for the dental industry] came from local research institutes. Transcelestial [develops a laser-based communications system], Medo [using AI to simplify the use of ultrasound in medical diagnostics] and a few others came from Entrepreneur First. Adatos [satellite image analysis for agriculture] and Saleswhale [AI sales assistant] were referred by existing portfolio founders. ThinCI [chipmaker based in India and the US] and Securezapp [confidential file sharing] were introduced to us by our advisors.

Kr: What are some deep tech strengths that you have seen emerge in the region? Do you see the potential for some world class deep tech breakthroughs coming from Southeast Asia? If so, which fields will they most likely come from?

PS: One area of strength comes from Singapore’s commitment to becoming the world’s first smart nation. You see it in their USD 19 billion commitment to R&D. You see it in the different programs run by the different agencies. All these attract talent, capital, and customers to Singapore, which make it fertile ground to grow deep tech startups.

Another is simply from the needs of the region. For example, agriculture is a major component of Southeast Asia’s economy at 12%, with net production increasing over the years. This creates an opportunity for precision agriculture companies like eFishery [automation for fish farms from Indonesia] and Ricult [farmer information system from Thailand and Pakistan].

Kr: As global investors, do you also look for ways to help deep tech solutions that are being created outside of Southeast Asia? How does that work? Or is Southeast Asia where you identify solutions and nurture domestic growth?

PS: We see both. We obviously see many deep tech startups being created here in Southeast Asia. What’s encouraging is we also see deep tech startups from outside the region wanting to come in, often using Singapore as their springboard. We see them coming from the US like ThinCI, from NZ like The Clinician, or from India like Hospals. They all know that Southeast Asia is open for business.

Kr: What specific deep tech applications will be most disruptive in Southeast Asia in the long run? What will Southeast Asia look like and what will we consider to be the new frontiers then?

PS: I know this may sound ironic, but we don’t feel like we need to look that far. We can only invest in deals that are in front of us, in deals that we can get access to. We have so many interesting things for us to do today. We prefer to focus on these. What will be interesting for us in the future will likely be driven by these opportunities. We take comfort in knowing that there will always be opportunities.

Wavemaker Partners has over USD 265 million in assets under management and has invested in over 300 companies. It’s the regional partner in Southern California and Southeast Asia of the Draper Venture Network (DVN), the world’s leading VC collective comprising ten firms across five continents.

Wavemaker Partners is an investor in KrASIA.