Indonesia’s Tokopedia is said to have closed a US$1 billion funding round led by SoftBank’s Vision Fund at a valuation of US$7 billion. The company hasn’t confirmed the report and declined our request to be interviewed, but it’s safe to say the round is now part of the tech canon. Last year, it got US$1.1 billion from Alibaba.

Tokopedia is often called the “Taobao of Indonesia” because both companies have a C2C online marketplace at their core, a place where individuals and small businesses buy and sell physical goods, like fashion, electronics, toys, snacks, potted plants, and everything else under the sun. But the Indonesian firm is following Taobao’s footsteps in more ways than one, and perhaps even growing beyond.

As Taobao grew bigger, it branched out into many new areas, earning itself the name “All Mighty Taobao” among Chinese online shoppers. The same is happening at Tokopedia.

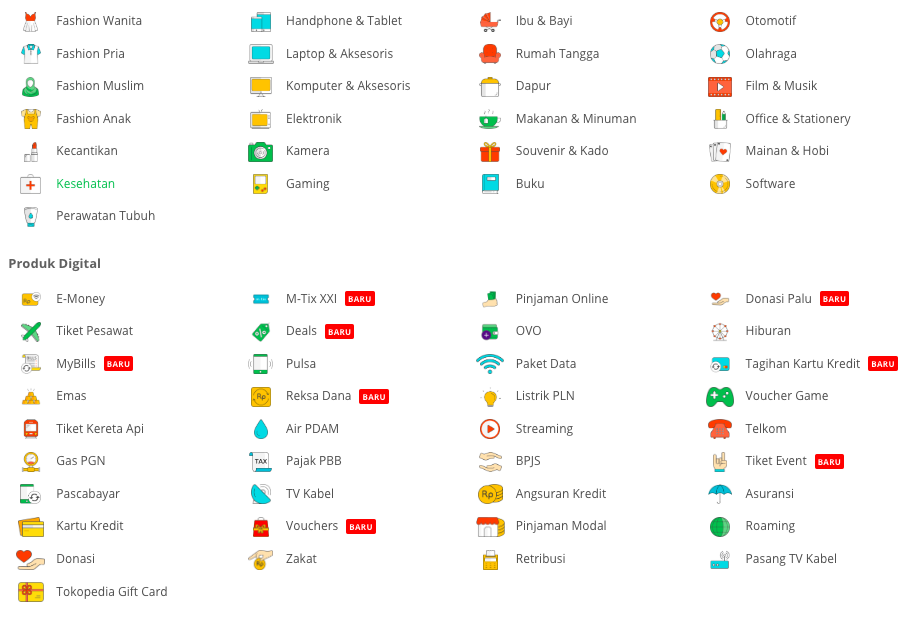

A lot of what Tokopedia offers now are digital goods, financial services, and payment functions. And this segment keeps expanding. It’s very ambitious.

The top section has all the physical goods categories, below is the ever-growing “digital products” section. The red markers say “new”.

In the payments arena, Tokopedia has mobile phone top-ups and bill payments, and vouchers for deals at nearby restaurants — these things are also within the standard repertoire of other apps, like Go-Jek, for example.

Like Taobao, Tokopedia also offers flights and train tickets, as well as tickets for attractions and events – encroaching on the classic domain of online travel agents like Traveloka.

But Tokopedia is a step ahead because it also offers financial services. For example, I can invest in mutual funds, or gold, through the app. (It collaborates with third parties to offer these services).

Taobao didn’t go there because Alipay, its sister company, has that covered. Grab announced plans for financial services tie-ups, but as far as I can tell, it hasn’t launched a product for end customers just yet.

While we don’t know how successful each of these categories is and if they’re actually ramping up Tokopedia’s revenue, it’s worth noting that it seems willing to pick a fight on all these fronts.

Add to that the recent announcement that Tokopedia is now also applying the “agent” model. This means it has launched a separate app that you can download to become a Tokopedia “agent”, or partner, to sell digital products to people in your neighbourhood who may not feel comfortable making a purchase online themselves. This online-to-offline mechanism where individual people become sales agents for digital goods was, in Indonesia, pioneered by Kudo, a company bought by Grab in 2017.

Tokopedia announced its agent network just after Bukalapak did the same. Bukalapak is the Indonesian company that’s quite similar to Tokopedia in that it also started as a C2C marketplace and grew to include digital goods and financial services. But its main investor is a local conglomerate, Emtek, whereas Tokopedia is part of the global empire of SoftBank and Alibaba.

At some point, we stopped viewing Grab and Go-Jek as ride-hailing companies and instead began using “on-demand platforms”, “local services apps”, or even “super apps” to describe what they do. In this sense, Tokopedia is becoming a super app in its own.

Editor: Ben Jiang