With a gavel in his right hand, the founder and CEO of Lakala Payment, Sun Taoran, strikes the Shenzhen Stock Exchange’s opening bell ten times, concluding a long and turbulent journey to its initial public offering (IPO). On the final chime, his company transforms—Lakala makes history by becoming the first third-party payments company to be listed on China’s major stock markets. Behind Sun, on a screen, Lakala’s stock price blinks over a red field. Bids are pouring in. The date is April 26, 2019.

Sun, a 50-year-old Peking University alumnus, is no stranger to the rituals of the stock exchange. Nine years ago, he was in the same hall when BlueFocus Communication, a leading Chinese PR agency he founded with four other friends, went public.

But Lakala’s path to going public was rockier. Its first attempt was overseas and ended in failure in 2010 when the company realized its variable interest entity structure—meaning an investor holds a controlling interest—could be a hurdle to obtaining a third-party payment license from Chinese authorities. Lakala’s second try, which used the shell of Shanghai-listed Tibet Tourism for a backdoor listing, was called off by the market regulator in 2016.

After those two fruitless attempts, Lakala’s IPO application was finally approved by the China Securities Regulatory Commission in March this year.

The listing ceremony stirred up long-bottled emotions in the seasoned businessman. Shortly before he rang the opening bell, Sun gave a heartfelt speech. “For the past 14 years, Lakala has been the one company that I poured most of my heart and soul into,” he told the 200 or so attendants who stood before him. “I hope to make her into a respectable company.”

Lakala’s story began in Beijing in 2005, a little more than one year after China’s flamboyant tech guru Jack Ma founded e-commerce platform Taobao in Hangzhou. China’s e-commerce industry was just taking off. That year, Taobao saw its transaction volume soar from a mere RMB 22.7 million to RMB 8 billion.

Sun aimed to build an expansive third-party payment network with POS terminals installed in the country’s convenience stores, allowing customers to pay utility bills, top-up phone credit, transfer money, and settle credit card bills. He wanted to build new infrastructure to consolidate and handle the most frequent cash transactions that took place around him. That could happen, he thought, if he could connect online spending with offline bank card usage.

Lei Jun, who would later set up the wide-reaching consumer tech company Xiaomi, was helping an old friend with due diligence of Sun’s project. Lei was so impressed by the idea of bridging online and offline payments that he decided to invest in Lakala, using the money he received from selling online bookstore Joyo to Amazon the year before.

In all, Lakala was founded with USD 2 million in seed funding. Lei Jun and Sun each contributed half a million dollars. The rest came from Legend Holdings, Lenovo’s parent company.

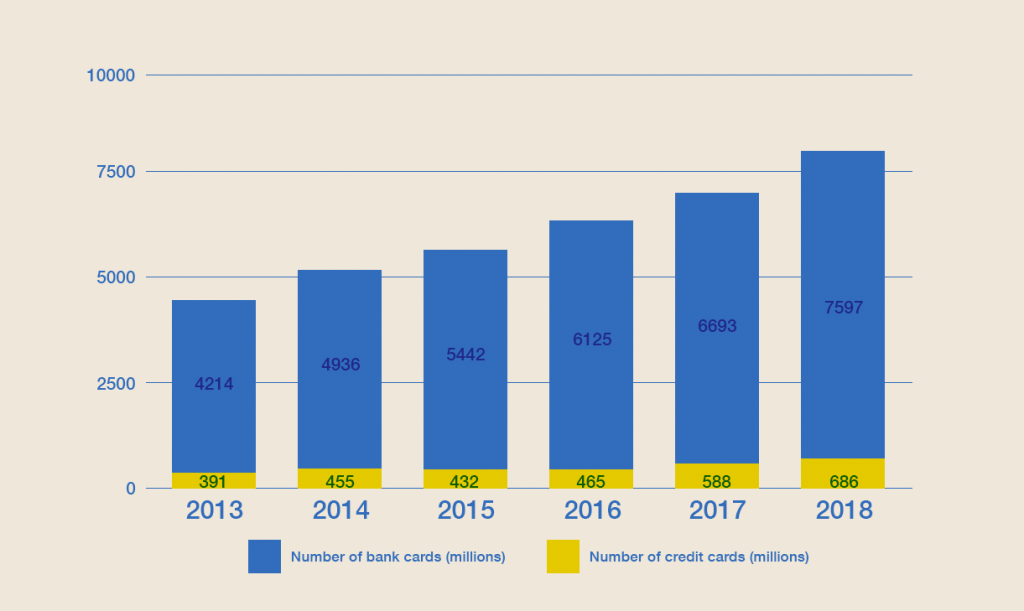

Though China is now known as a forerunner in phone-based payments, things were different 14 years ago, when it wasn’t uncommon to see people paying for new cars or depositing down payments for residences with piles of pink RMB 100 banknotes. At the time, a mere 13% of the country had debit or credit cards issued by banks. Though Bank of China introduced the country’s first nationwide credit card in 1985 — 20 years before Lakala’s inception — credit cards were marketed as shiny new toys for the wealthy rather than tools for payments designed for anyone with a bank account. The idea that cash in hand couldn’t be replaced by magnetic strips (and later, silicon) was at odds with Lakala’s bet that credit cards would become the most important payment method in China.

But Sun found important indicators where others missed them. After China’s accession to the WTO in 2001 and the founding of UnionPay in 2002, the country’s credit card ownership began to take off. Between 2004 and 2009, credit card adoption grew 40% annually on average. Lakala took root as consumers in China became more comfortable with handling their expenditure using bank cards, and the company emerged as one of the leaders in the third-party payments industry. In 2008, Chinese e-commerce top dog Alibaba announced a partnership with Lakala, enabling Alipay users to top up their accounts through Lakala’s POS machines.

By the end of 2009, Lakala had more than 30,000 terminals across 38 Chinese cities, handling six million transactions monthly. Within two years, those machines would be found in 95% of convenience stores in the country. For Lakala, the future couldn’t have seemed brighter.

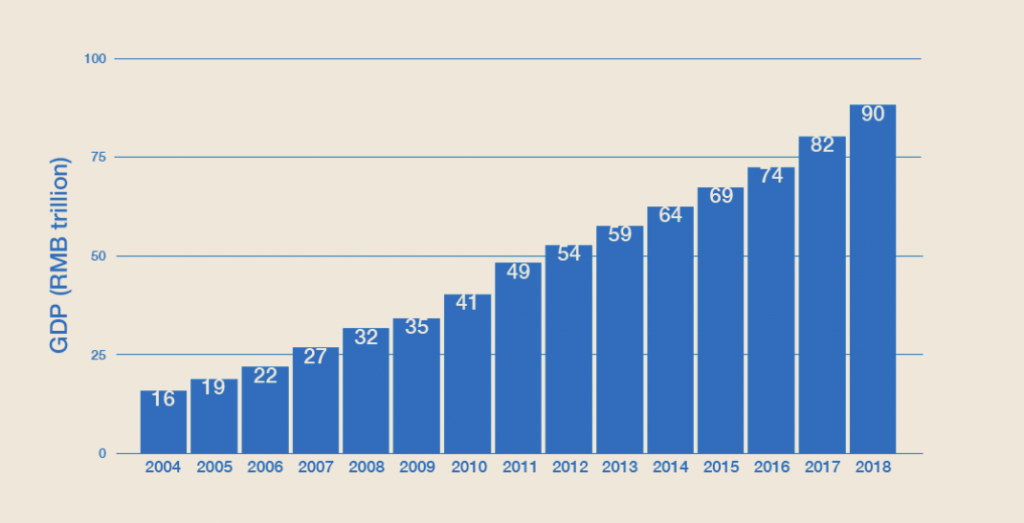

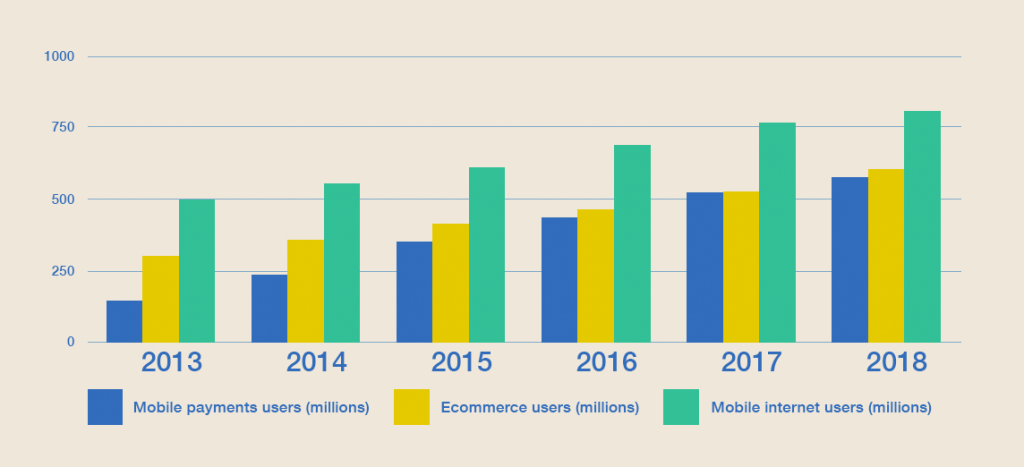

But disruptors can be disrupted too. As smartphones became ubiquitous across China, so did mobile payments. There were fundamental changes taking place in how Chinese consumers handle their money. China’s mobile payments market grew from roughly RMB 100 billion in 2011 to nearly 280 times in size at RMB 277.4 trillion in 2018.

By the time Lakala dived into mobile payments in 2012, Alipay had already secured a comfortable 58% market share, and Tencent’s e-wallet was also gaining traction. Today, Alipay and WeChat Pay hold 53.78% and 38.87% of the market, respectively.

“As long as WeChat Pay and Alipay are active in the personal payments service market, nobody else has a chance,” an industry insider told KrASIA. He said that e-wallets’ ability to transfer funds and pay for purchases wasn’t enough to make people use them, but apps that kept their users engaged within their own networks had a chance of surviving and thriving in the cutthroat industry.

Unfortunately for Sun and Lakala, that realization came too late—and it carried a huge price tag.

In their effort to catch up with the competition, Lakala eschewed an app-based mobile payment solution, and decided to develop a mobile credit card reader that could plug into smartphone headset jacks. They called it Kaola and released it in May 2012.

Lakala was determined to push for Kaola’s adoption by individual users, and expanded its 900-strong sales team in 2011 to 4,000 within a year. For a moment, it looked like the plan worked. By March 2013, Lakala had shipped two million Kaola units.

But that initial success could not reverse Lakala’s decline in personal payment services. In an interview with NetEase in 2015, Sun revealed the anxiety that he was experiencing at the time. “I’ve mostly been thinking about the risk of failing and potential problems that might arise after failing,” he said. Yet Sun saw a way out of the hole: “Lakala has another opportunity . . . that’s smart bracelets.”

This time, Lakala snubbed QR codes and bet on a smart bracelet that works like a Xiaomi Mi Band or Fitbit, but with a built-in wireless payment function. In Sun’s vision, Lakala’s bracelets, which were released in September 2015, could replace travel cards and allow people to easily tap-in and tap-out during their daily commutes. In reality, the piece of hardware failed to garner a fanbase; the company’s flagship store on Alibaba’s Tmall sold less than 50 units in June 2019. Xiaomi’s Mi Band 4 sold 79,000 units on its Xiaomi’s Tmall flagship in the same period.

“Lakala’s whole business strategy was still fixated on bank cards,” an executive at a cross-border payments company told KrASIA. The company was left in the dust when it became set in its ways and refused to face the fact that smartphones and mobile payments were about to displace cash and credit cards.

Sun probably agrees with that assessment. “Being able to change ourselves or change the ways of doing things which have made us successful is very difficult. But it’s very important.” he told a full house of entrepreneurs at an annual gathering in 2015. “I have seen many very successful companies being surpassed or replaced because they were stubborn and unwilling to make adaptions in the face of changes.”

Looking ahead, Lakala announced in June that it plans to set up a securities brokerage with Legend Holdings and VMS Securities, leaping out again from its comfort zone of third-party payments.

Additional reporting by Wu Mengqi and charts/graphs by James Chan.