After a 13-year bull run culminating in a record-breaking funding year in 2021, investors have turned more cautious with their investment strategies.

While exponential growth was what most investors previously looked for in startups, the current horizon of rising interest rates and declining market liquidity has caused them to rethink the funding of profitless futures indefinitely. As investors continue to adapt their funding strategies, industry observers expect further pullbacks in their support of startup funding, valuations, and exits.

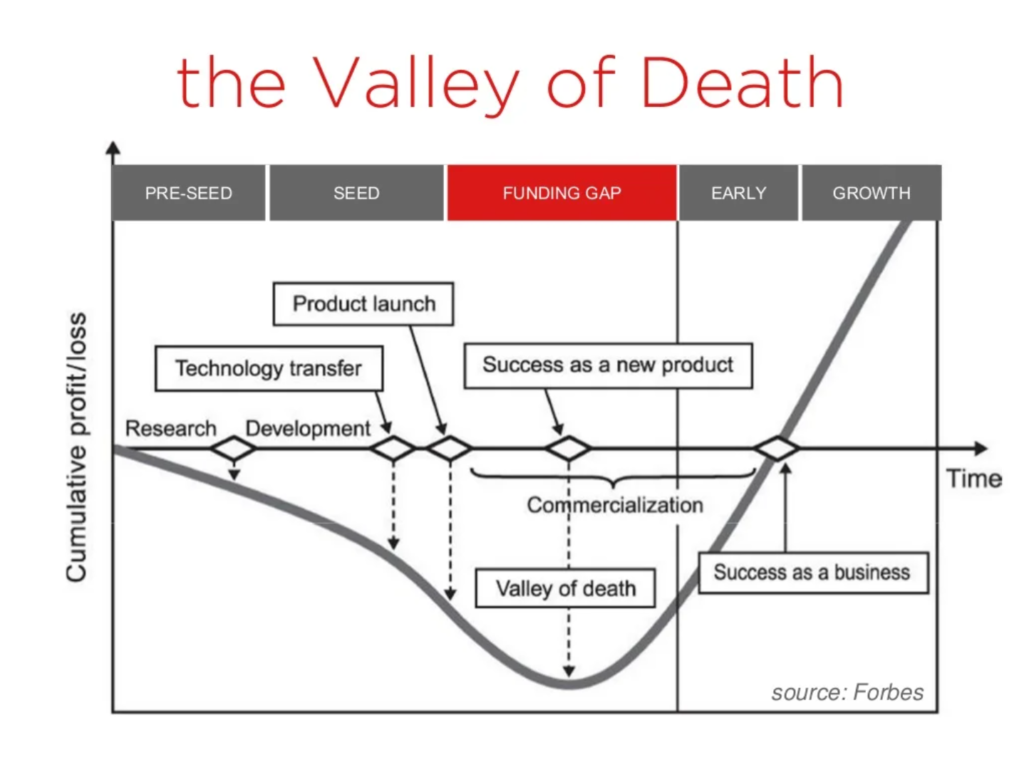

Hence, it is important for startups to ensure they remain commercially viable for investors; otherwise, they will encounter the ‘Valley of Death,’ a funding gap between the seed round and early stages of a startup. The valley visualizes the cash flow and funding difficulties that most startups face when determining their product-market fit for commercialization.

Startups that are unable to understand their market needs and how their business can scale in consideration of these needs typically fall into the Valley of Death and do not prosper after the seed and Series A funding stages. However, once startups successfully secure their Series B funding, their chances of making a successful exit increase significantly.

As the funding winter approaches, this is a good time to unpack why most startups do not survive and identify the traits of successful startups.

Achieving product-market fit

For startup founders, finding the right product-market fit is key to success. The right product-market fit is proof that the startup’s product is an in-demand solution, and there is a sufficient user base to scale a business model and achieve profitability.

The ability to scale is crucial in highly competitive sectors like e-commerce, as illustrated by two startups based in Indonesia, Bukalapak and Stoqo. Bukalapak is a B2B e-commerce marketplace that brings ‘warungs’—mom-and-pop stalls—online, and connects them with suppliers and customers. Stoqo was a B2B platform that provided F&B establishments in Jakarta with daily ingredient deliveries at competitive prices. Although both operate within the same sector, Stoqo encountered difficulties in growing its user base, as most F&B businesses already have existing relationships with their own preferred suppliers. Moreover, Stoqo’s costly labor-intensive operations and mispriced products led to minimal profit margins, which further complicated their ability to scale. In the end, Stoqo was unable to scale its way to profitability and eventually closed in 2020.

On the other hand, Bukalapak’s asset-light and easy-to-use platform enhanced its ability to scale in a market with millions of small retailers looking to digitalize to stay competitive. Bukalapak achieved unicorn status in 2018 and went public in 2021.

On top of having a scalable business model, startups must also understand their market. Emeritus is a Singapore-based edtech startup that offers online executive and postgraduate diploma courses, while Loop is a Singaporean marketplace for online courses. Although both offer similar products, Emeritus partnered with well-known educational institutions, such as Harvard University and the Massachusetts Institute of Technology (MIT), to offer online courses, whereas Loop participated in the Singapore government’s lifelong learning program, SkillsFuture, to ensure that their courses received public funding.

While these government subsidies have made Loop’s tertiary programs more affordable and accessible to the public, issues have been raised about the quality of their educational offerings. By contrast, Emeritus identified that prestigious educational institutions could enhance its standing as a go-to platform for learning since many people who take online courses prefer prestigious institutions and are willing to pay a premium for such courses. With a unicorn status and having secured around USD 803 million in funding, Emeritus’ strategy has clearly worked. By contrast, Loop has yet to receive any funding.

Adaptability

A startup’s product-market fit changes according to market conditions and needs. As a result, startups need to be responsive to such changes. They need to adapt or risk redundancy and obsolescence.

A comparison of Thai retail startups Pomelo and Wearyouwant illustrates the importance of being adaptable. Wearyouwant was an online retail marketplace, while Pomelo is a Thai-based fast fashion brand popular in Southeast Asia. Both started with the same idea—to bring Korean fashion to Thailand. However, Wearyouwant did not evolve beyond their online marketplace business model, causing them to become increasingly redundant in the competitive e-commerce and fashion landscape as rivals like Lazada, Zalora, and Zilingo gained prominence. By contrast, Pomelo was adept at transforming their brand and business model according to new trends and emerging market conditions. They built a recognizable brand that distinguished them from other online fashion competitors by transforming from being an online-only retailer to adopting a more relevant omnichannel approach with new B2B verticals. Pomelo’s agility allowed them to not only retain their market share, but also venture into new markets. This is why they are currently at the stage of raising Series D funds or going public. On the other hand, Wearyouwant shuttered in 2017.

In recent years, the COVID-19 pandemic and geopolitical tensions have wreaked havoc in the business world. The way Bukalapak and Stoqo responded to Indonesia’s pandemic restrictions played a significant role in determining their success and demise, respectively. In the wake of the social distancing measures implemented in Indonesia, Stoqo failed to pivot away from its B2B model to offer B2C services while Bukalapak adapted and capitalized on the growing demand for e-commerce during the pandemic by easing the onboarding process for new users. The latter also generated new revenue streams with new verticals, like partnering with Standard Chartered to offer financial services.

Pitching the unproven

In Southeast Asia, most venture capital firms prefer to invest in startups from familiar sectors, or startups that are carbon copies of successful ones from the US or Europe. New, unconventional businesses may seem too risky for investors, especially when startup founders are unable to pitch their brand story effectively.

Singaporean unicorn PatSnap is one such example. PatSnap provides intellectual property (IP) analytics and intelligence services. Founder and CEO Jeffrey Tiong started PatSnap in 2007. While he had managed to secure angel investments in the early years, it was only seven years later when PatSnap successfully raised its Series A funding. Jeffrey admitted that the initial lack of venture capitalist confidence in PatSnap stemmed from his failure to convince investors of his pitch.

IP analytics was, and still is, a niche space. PatSnap is the first of its kind to gain any kind of global recognition and traction. Back in the late 2000s, this field was ahead of its time. In Singapore, there are only four other similar companies, none of which have received any funding. Three out of the four firms are no longer in operation. The sole surviving Singaporean IP analytics company is GreyB, which operates more like a research consultancy. Based on Tracxn data, similar startups across the world still have not raised funds anywhere close to levels achieved by PatSnap. Most are either unfunded or have raised less than USD 10 million.

Similar to IP analytics, aquaculture tech (aquatech) is another sector that investors are less likely to fund, as opposed to a less risky business with high scalability and low initial costs. The complex and fragmented nature of Asia’s aquaculture sector implies that most Asian aquatech products must be adaptable to different farmed species, farming systems, cultures, and geographies, which makes scalability difficult. Unsurprisingly, aquaculture made up less than 0.02% of the USD 423 million investments raised by Southeast Asian agrifood tech startups in 2019. According to data from Tracxn, 39 of the 47 active aquatech startups in Southeast Asia have yet to receive significant funding.

Nevertheless, in Indonesia, two aquatech startups, eFishery and Aruna, have completed record-breaking funding rounds over the past few years, with eFishery poised to be Indonesia’s next unicorn.

Aruna caught the eye of investors after successfully raising seed funding in 2019. In 2021, the startup raised the largest Series A funding amount (USD 35 million) in Indonesia’s agritech sector to date, with follow-on funding of USD 30 million a year later. eFishery took slightly longer to gain investor confidence, having raised their Series A three years after their seed round in 2018, and their Series B in 2020. This culminated in their USD 90 million Series C round in 2022, the largest Series C investment amount to date for a Southeast Asian agritech startup. Both startups offer products and services with familiar technology and business models, making it easy for investors to understand their businesses. Aruna is a B2B and B2C platform that is similar to an e-commerce platform, and eFishery produces automatic fish feeder devices and offers platform-based software and financial services.

While niche services or products in technical sectors can be difficult to pitch, the success of Aruna and eFishery seems to have given a boost to investor confidence in Indonesia’s aquatech sector. Two of the 24 active aquatech startups in Indonesia, Jala and DELOS, were able to raise their Series A and seed funding in 2021 and 2022, respectively.

The winning strategy

While investors may be initially reluctant to invest in a startup due to the industry’s infancy or a high-risk business model, it does not mean that the Valley of Death is imminent. What matters most are a startup’s fundamentals.

Startups that are dynamic, adaptable, and in tune with their users and market conditions can still achieve product-market fit and sustained growth.

Despite its treacherous terrain, the Valley of Death should not deter startups from pressing on to develop more innovative solutions to real-world problems.

This article is co-authored by Richard Mackender, Tan Shuo Yan, Teo Zhixin, and Nur Hazeem Abdul Nasser.

Richard Mackender leads the Deloitte Southeast Asia Innovation team, a cross-function, cross-country unit dedicated to driving innovation as a long-term value creator across Deloitte’s Southeast Asia operations. Tan Shuo Yan, Teo Zhixin, and Nur Hazeem Abdul Nasser are members of the team.