In its most extreme form, a psychological condition known as chrometophobia — fear of money — can take over the lives of people who suffer from it. They recoil from the sight of cash, flinch when touching or coming into contact with paper bills and coins.

SoftBank Group, Japan’s most aggressive venture capital investor, thinks they might be onto something. Its latest multibillion-dollar technology bet is being marketed on a simple proposition: In the age of the coronavirus, cash is immensely dangerous.

“Many people don’t want to touch paper bills and coins that may have been touched by someone else,” said Ichiro Nakayama, CEO of the new SoftBank-created digital payment app PayPay, in a livestreamed news conference in July. “Cashless is the way to enable touchless and contactless.”

Cash phobia could not have come at a better time for SoftBank’s massive bet on digital payments in Japan. Cashiers across the country have begun asking customers to take extreme sanitary measures when paying, such as placing bank notes on a tray, wiping the tray with a sanitizer after each transaction, often while wearing plastic gloves. In South Korea, people have been cooking bank notes in microwaves to disinfect them.

That is all very encouraging, according to Nakayama. “Sixty-nine percent of respondents said that they felt resistance for bank notes and coins from the viewpoint of public health,” Nakayama told the news conference devoted to PayPay’s progress in conquering cash.

SoftBank has invested over USD 1 billion in PayPay and taken nearly USD 800 million in losses in the year ending in March. It is wagering that it can succeed in popularizing mobile payments in a country where nearly a dozen other competitors have failed. Japan has been famously resistant to mobile payments technology: Consumers prefer withdrawing money daily from convenient ATMs to scanning a QR code on their phone. Unlike in China and India, where mobile payments quickly entered the mainstream, in Japan, they remain 1% of a USD 5 trillion economy.

Curing Japan of its cash addiction would be incredibly lucrative; bringing the mobile payment penetration rate on par with China’s would create a USD 1.3 trillion industry.

SoftBank, meanwhile, desperately needs a win. It is struggling after a series of technology bets gone badly, including troubled office-sharing company WeWork and Uber Technologies’ underperformed initial public offering. Despite vowing to pivot toward a cautious and defensive strategy, it hit headlines this week with reports identifying the company as the “Nasdaq whale,” a massive buyer of tech stock options whose market-distorting activity caused share prices to skyrocket. Undaunted, it is quietly putting its chits on the roulette wheel once again — this time, wagering hundreds of millions of dollars that it can transform Japan from a hinterland of cash hoarding to a digital payments powerhouse. And the coronavirus has become a major talking point for PayPay executives.

“COVID is a gift to cashless payment providers,” said Michael Causton, a retail analyst writes on research platform Smartkarma. “Retailers want to protect staff from unnecessary contact with customers and contactless payments help this tremendously. Consumers, too, of course, want to avoid handling cash from stores to reduce the chances of contamination.”

Winner takes all

At a glance, PayPay is the kind of mobile wallet commonly seen across Asia. Users download the app, link their bank account, and top up money to their PayPay account. They can make payments either by scanning a QR code at a shop or having a clerk scan the app’s unique bar code.

Since launching in late 2018, PayPay has clinched the lead in Japan’s crowded mobile payments market. The app hit 30 million registered users at the end of June, equivalent to a quarter of the Japanese population. PayPay’s distinctive red and white logo is increasingly visible in restaurants, at barbers and dry cleaners, and is now accepted by more than 2.3 million merchants across the country. Over a billion transactions have been processed.

Tangible signs of progress are a welcome sight for SoftBank under the helmsmanship of controversial founder and Chairman Masayoshi Son. Over two decades, Son’s early bet on Chinese e-commerce giant Alibaba forged his reputation as a technology visionary. In reality, his strategy is often centered around endless rounds of financing in companies with unproven business models, from Didi Chuxing in China to Grab in Southeast Asia, which in turn deploy the cash in desperate and expensive fights for market share: “cash burn,” in the parlance of the tech industry. And PayPay’s strategy is solidly part of the traditional SoftBank playbook. The aggressive promotions and sales drive have turned PayPay into a cash cremation machine. The company logged a net loss of JPY 82 billion (USD 771 million) for the year ended March.

The object of cash burn — a strategy of subsidizing the users of a service — is to achieve scale quickly. Users will not use the app if a lot of businesses are not accepting it, and businesses will not start accepting it unless a lot of buyers use it. The solution to this chicken-and-egg problem is solved by buying large numbers of users and merchants, who hopefully will keep using it even when the incentives run out.

Most companies would grow queasy at the thought of losing nearly a billion dollars per year handing out money. But cash burn is part of SoftBank’s DNA. Some employees compare PayPay’s aggressive tactics to the days when SoftBank gave away free modems for its broadband service in the early 2000s. “The ability to scale the service with speed and money is classic SoftBank,” one former executive said.

As an investor, SoftBank has been an enthusiastic proponent of burning cash, spending freely to back its champions in virtually every tech market-share war witnessed in Asia over recent years. Epic losses were endured by both Uber and Didi Chuxing in China; SoftBank backed Didi, which eventually acquired Uber’s China business in exchange for a 19% stake, but not before both sides had spent billions of dollars on incentives. In Southeast Asia, SoftBank has injected about USD 3 billion in ride-hailer Grab since 2014, fueling a brutal price war with Gojek in Indonesia. The competition later spread across the entire region when Gojek launched operations in neighboring countries.

“In our industry, the winner takes all,” Son told investors at a conference in Tokyo last year. “Compared to the physical, real industry, [with] online there is no physical distance, no physical storefronts that [matter]. [In] less than a second, it can go worldwide. So why should a No. 2 exist?”

But after a nearly unblemished track record of picking No. 1s, Son’s record has been tarnished recently with a series of catastrophic decisions.

The company’s performance took a hit last year after SoftBank and its USD 100 billion investment vehicle, the Vision Fund, sank more than USD 10 billion into WeWork, the US shared office operator. When WeWork canceled its initial public offering last year due to weak demand, its valuation collapsed and prompted the largest loss in SoftBank’s history.

Meanwhile, the stock price of Uber, the US ride-sharing company and one of the Vision Fund’s largest bets, remains below its IPO price of last year.

Son was still reeling from his damaged reputation when COVID-19 hit investor sentiment, triggering a sell-off in SoftBank’s shares. He has since pivoted to stockpiling cash, raising more than USD 41 billion by selling assets or pledging them to take out loans and boost share buybacks.

The strategy has helped drive SoftBank’s share price to a 20-year high, and generate a JPY 1.2 trillion net profit for the fiscal first quarter.

But SoftBank cannot afford another WeWork-like stumble. The saga not only led to huge losses but raised questions over Son’s freewheeling investment style. Those concerns are likely to multiply with the revelations about SoftBank’s “Nasdaq whale” strategy.

Meanwhile, the lavish spending on PayPay comes as some SoftBank investors complain about the wisdom of a huge bet on an industry that has proved famously hard to crack.

“SoftBank has been trying for years to create a digital ecosystem in Japan, but it is still playing catch-up,” said one domestic analyst, referring not only to payments but also to e-commerce, which is led by Rakuten and Amazon, and other online services.

If Son’s bet fails, it would be fuel for SoftBank shareholders who want to rein him in, seeing his unpredictable style as a liability. Son, who owns nearly 30% of SoftBank’s shares, has already seen his tight control over the company come under threat. Calls from activist shareholder Elliott Management earlier this year prompted the company to boost buybacks and add independent directors.

“It’s a company that is more vulnerable this year than it’s been for many years,” said one foreign hedge fund manager. “Institutional investors are very keen and strongly feel that a much stronger governance structure needs to be put in place.”

But if it succeeds, the rewards would be immense. PayPay’s aspirations go far beyond mere retail transactions. Its goal is to create the equivalent of Ant Group’s Alipay in Japan — a gateway for all kinds of payments and financial services. Ant Group, controlled by Son’s longtime friend Jack Ma, is planning to raise USD 30 billion in an IPO that could become the world’s largest flotation in history.

“Alipay is going to be bigger than Alibaba,” one person close to SoftBank said. “And it is the basis of PayPay’s business model.”

Meanwhile, the price of not trying at all would likely be oblivion. Failing to build a mobile payments champion in Japan would be a major setback for SoftBank at a time when digital payment is increasingly becoming the entry point for all kinds of online transactions, from shopping to food delivery.

“Becoming a key player in cashless payments is critical for any firm that wants to be a dominant player in digital ecosystems in the long term,” Causton said.

Son has largely stayed behind the scenes at PayPay as Ken Miyauchi, the CEO of SoftBank’s mobile unit, talks about the service in public events. But industry observers say the business model follows Son’s signature winner-take-all strategy.

Follow the money

Son’s journey to PayPay began in India — a country he reckoned was on a path similar to China’s but also held the key to Japan’s own inevitable transformation toward digital payments.

His interest in following China’s model is natural, given that he is possibly the most successful foreign investor there. A USD 20 million bet Son made on Jack Ma’s Alibaba in 2000 is now worth about USD 180 billion. Son had set his sights on India as the next China. In late 2016, he approached Indian tech entrepreneur Vijay Shekhar Sharma with what would turn out to be a very lucrative proposal.

Sharma’s company, the Indian digital payments startup Paytm, was riding a huge economic transformation. Indian Prime Minister Narendra Modi had upended the country’s financial system by rolling out a real-time payments network called United Payments Interface, and then banning large bills, a huge windfall for digital payment companies like Paytm.

“My meeting with Son-san was very, very high-energy,” Sharma recalled in an interview last year. “He obviously knew what was happening in China.” Ant Group, the digital payments affiliate of SoftBank-invested Alibaba, had also become one of Paytm’s largest investors.

“He asked, ‘How much will you raise?’ My answer was, ‘At least a billion dollars this time.’ And then [Son] said, ‘We will invest USD 1 billion, and we will also buy secondary shares.'” SoftBank’s newly launched Vision Fund ended up investing USD 1.4 billion in the company.

Around the same time, SoftBank unit Yahoo Japan had also begun to consider moving into payments. After starting out in 1996 as a local joint venture with Yahoo in the US, Yahoo Japan eventually became more successful than its parent and a leader in online advertising. But despite efforts to expand into areas like e-commerce, it was struggling to break the stronghold of Rakuten and Amazon. It saw an opening in mobile payments.

Yahoo Japan spent about two years preparing a mobile payment service, according to people familiar with the matter. But Son, who wanted to bring global expertise, invited Sharma to Tokyo months before the launch. Sharma was taken by surprise: “We did not have plans to come to Japan earlier. You never see an Indian company expand to a developed market.”

Yahoo had prepared a slide presentation for Sharma. Instead, Sharma asked to see the source code underpinning the app. He quickly identified some issues. “The thing we changed about the technology is that, typically, a Japanese shopkeeper was getting money after four weeks. With PayPay, they get it on the next business day,” he said. The Japanese company also agreed to cut fees to zero and enable all merchants to join first, instead of having each one vetted through a time-consuming approval process. About a dozen Paytm engineers were brought to Tokyo, and they revamped the entire app in about two months.

When PayPay finally launched, it was a late entrant in a crowded market. Japan, the world’s third-largest economy, has all the elements of a lucrative digital finance business. Households stash more than JPY 1 quadrillion (USD 9.4 trillion) in either banks or in cash, more than half of total household assets. Tapping even a fraction of the money would potentially generate huge fees for a financial technology player.

But despite years of efforts by traditional banks, startups and the government, Japanese have stubbornly stuck to cash. Cash accounted for about 80% of consumer spending in 2017, according to a government report, lagging far behind Asian peers like China and South Korea. Fintech startups in Japan have largely watched from the sidelines as even peers in emerging markets like India and Southeast Asia, which are leapfrogging traditional banking services and embracing mobile payments, raise capital at lofty valuations.

Japan’s large elderly population has sometimes been blamed for the country’s addiction to cash. In reality, “cashless payment is not new in Japan,” said Celeste Goh, an analyst at S&P Global Market Intelligence. Credit cards have penetrated deep into Japan, where each consumer owns an average of three credit cards. “Consumers are open to the idea of exploring noncash payment options,” Goh said.

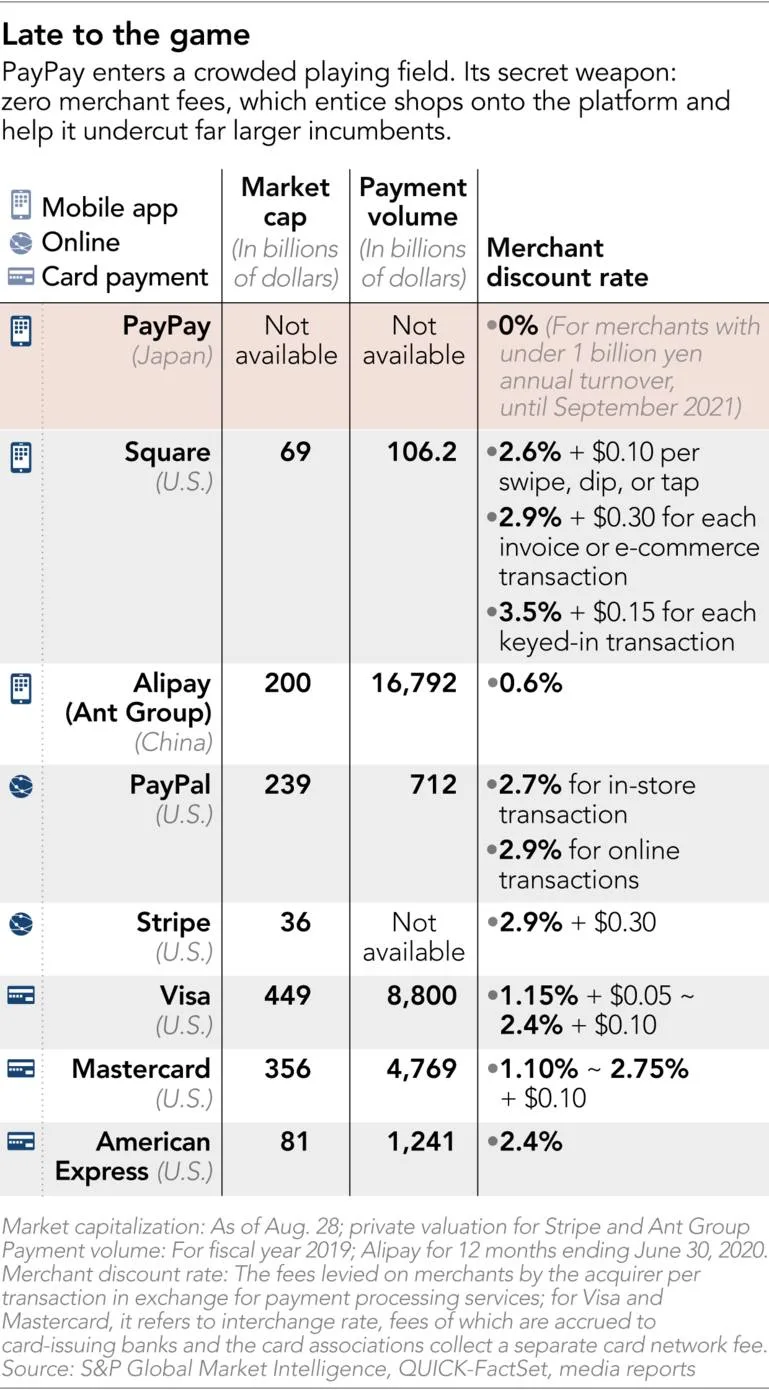

The bigger issue is that cashless payments are not widely accepted by shops, who have long resisted going cashless because of cost and inconvenience. Digital payment providers charge an average of about 3% of retail transactions facilitated through their service, according to Goh. That compares to less than 1% for China’s Alipay and its main competitor WeChat Pay. In addition, the sales are generally wired to the shop owner’s bank account only once or twice a month in Japan.

“The challenge is really for Japan to get merchants on board with this idea, either by reducing the fee charges or finding a way to reduce the settlement cycle,” Goh said.

Sharma explained that to convince merchants to accept PayPay, the service needed to be as attractive as cash, which they can get instantly and with no hidden fee. So PayPay decided to charge nothing for three years as long as they were small businesses — stores with less than JPY 1 billion in turnover — and accepted its QR code payment option.

Today, more than 100 engineers work around the clock to roll out updates at a relentless pace. SoftBank has brought in more Vision Fund companies as part of a burgeoning app ecosystem — as the number of shops accepting PayPay soared, Mapbox, a US mapping technology company, built a customized map so users can filter stores by category. Chinese ride-hailing giant Didi Chuxing was made available directly through PayPay’s app.

SoftBank also bankrolled the venture lavishly, hiring thousands of salespeople across the country that were tasked with bringing shops onboard. The stream of updates from the engineering team caused chaos in the early days, a former employee recalled, “because features that we had described to a client yesterday would be totally different the next day.”

That was combined with eye-popping promotions for users, including a 10-billion-yen giveaway campaign shortly after PayPay’s launch. Aggressive branding raised the app’s profile; SoftBank, which owns a baseball team, even renamed its home stadium after PayPay.

It kicked off its latest series of promotions with a “2000% bonus” campaign in August, in which one in five payments will give back between 2% to 20 times the transaction value.

“There is a lotterylike feeling to it,” said one store manager at a major electronics chain that accepts PayPay. “I think that is why it attracts customers.”

In far outspending its competitors, PayPay has wiped out small players from the market. Starting from nothing in 2018, it had a market share of 55% of the code payments market as of January, according to Japan’s Fair Trade Commission.

But that has provoked rivals to start offering their own lavish promotions. In recent months, major telecommunications carriers NTT Docomo and KDDI have begun investing heavily to catch up. The relentless pursuit of Japanese wallets is shaping up to be a test of how far SoftBank is willing to keep bankrolling the bet, as a series of soured bets prompts its global portfolio to shift away from a growth-at-all-costs strategy.

“They are beating each other with bundles of bank notes,” said Kazunori Ito, an analyst at Morningstar.

On Aug. 4, Miyauchi, CEO of SoftBank’s mobile unit, said PayPay’s “massive losses will peak out” but did not provide a timeline for achieving profitability. At the same time, his optimism seemed undimmed.

“We want the majority of people in Japan to be using it,” he said.

A current senior executive refers to Son’s business philosophy: “If the profit margin is 10%, there will be competition at 9%. … If it is 1%, competition at 0.5%. But if it is zero, there is no competition.”

The trouble with burning cash is that “you are renting users, rather than buying them,” said a Shanghai-based venture capitalist who has worked with SoftBank. “Unless you can change consumer behavior, the users will run out when the incentives do.”

Analysts say SoftBank will likely keep bankrolling the venture until next October, when PayPay starts charging transaction fees from its millions of merchants. If it continues to maintain a dominant position after that, companies will be lining up to pay for access to its large user base. The growing number of sellers, in turn, will attract more and more users to the app.

Creating this virtuous cycle, also known as the network effect, will cement SoftBank’s reputation as a successful investor. Failing to do so will mean it has merely given away hundreds of millions of dollars.

And the kind of investors Son needs to assuage are motivated by short-term profits rather than long-term vision. SoftBank Group has an established track record of building profitable businesses in Japan. While it boasts a portfolio of tech companies around the world, it still relies on a single company for the bulk of its cash flow: SoftBank Corp., its Japanese mobile unit. The parent SoftBank raked in about $20 billion by floating some of its shares in late 2018, and sold some more as part of its recent monetization program.

But it will likely be years before PayPay turns a profit, and it is not clear if Masayoshi Son can wait that long.

“The trouble is,” said Causton, the retail analyst, “no one is going to be making money out of payments for a long time — unless PayPay stops offering all those juicy incentives.”

This article first appeared on Nikkei Asian Review. It’s republished here as part of 36Kr’s ongoing partnership with Nikkei.