Imagine an app that gives you access to messaging, media content, e-payments, ride-hailing services, or even online doctor consultation, among other services —this is the concept of super apps, first popularized in China by Tencent’s WeChat and followed by other players such as Grab and Gojek in Southeast Asia.

Super apps are ingrained into Asia-Pacific mobile users’ daily lives due to their versatility. From only one platform, users can send messages, order food, hail taxis or book plane tickets, and pay for goods and services. Platforms like WeChat and Alipay have amassed 947 million and 647 million monthly users (MAU) respectively in China, according to market research firm QuestMobile. Another super app, Meituan-Dianping, which started out as a group-buying food delivery platform, quickly gained prominence by providing similar services in 2,800 cities across China, with over 457 million MAUs as of Q2 2020, according to the company’s financial report.

The hype quickly caught on in other regions such as Southeast Asia, where rivals Singapore-based Grab and Indonesia-grown Gojek are racing to become the leading super app for 310 million digital consumers. In the past three years, both companies have been actively adding more services into their apps, from financial services to travel arrangements.

Though both firms started from a completely different base compared to their Chinese counterparts, their end goal is the same: board more users into its platform by adding more and more services.

The available routes, from one thing to everything

To become super apps, each company is taking different routes. Some decided to add more functions into their app through in-house development of new functions or the acquisition of existing startups, while other platforms opened their system to third-party companies via mini programs.

While Chinese platforms such as WeChat and Alipay implemented the mini program strategy (small apps within a native app that can be accessed on-demand to perform a variety of functions) Southeast Asian super apps have mostly developed their own services or have been undergoing an acquisition spree in the past years to transform their platforms into super apps.

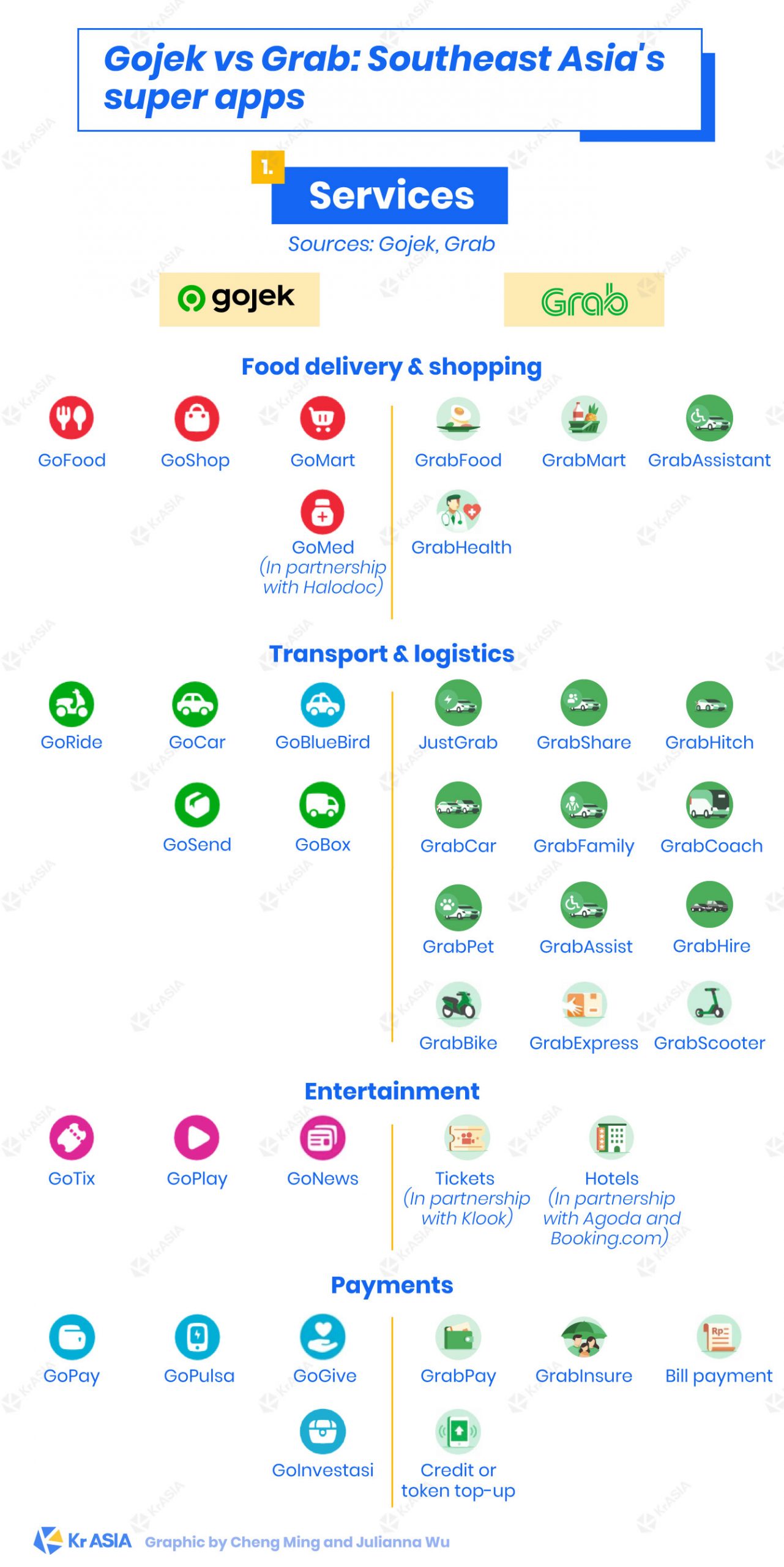

In order to strengthen its financial service arm GrabPay, Grab took multiple fintech startups under its arms such as Indonesia’s Ovo in 2017, Bangalore-based iKaaz in 2018, and robot-advisor wealth management platform Bento in 2020. Grab also partnered with banks across the region such as Thailand’s Kasikorn Bank, UOB, Credit Saison, and Chubb in 2018, while it has also signed partnerships with Agoda and Booking.com for travel services.

As for Gojek, the firm recently acquired point-of-sales platform Moka to enlarge its payment network. It also invested in gold investment platform Pluang and formed a partnership with mutual fund platform Bibit to start an investment service called GoInvest. As for insurance services, Gojek invested in insurtech startup PasarPolis which gave birth to GoSure.

The spree resulted in a vast range of financial services available on both the Grab and the Gojek apps, including digital payments, insurance, lending, and investment, in addition to grocery shopping and medical consultations, among other services.

Both companies also utilize their accelerator programs, Grab Ventures Velocity (GVV) and Gojek Xcelerate, to scout for potential partners to be included in their ecosystems. Through these programs, both companies provide mentorships for selected startups. One example is Sejasa, an on-demand home service platform that graduated from GVV’s first cohort and is now accessible to users on the Grab platform looking to book cleaning or maintenance services.

The Chinese super app model

In short, WeChat and Alipay have been creating an ecosystem similar to operating systems like iOS or Android. WeChat, for instance, allows users to browse the internet, play games, buy products, order tickets for movies or travels, share articles and music through Moments, and text friends without having to leave the app, among many other functions.

Even if both companies have had their fair share of investments and acquisitions in the past to grow their apps’ services, WeChat and Alipay are now bolstering their offerings mainly via mini programs, which could be seen as a faster method to provide more services to the final user. Mini programs allow users to “upgrade” their super apps by installing programs they consider necessary, such as games or services, created by third-party developers.

Watch this: Mini programs are now a big thing in China. So what exactly are they?

In 2019, WeChat hosted over 2.3 million mini programs, while Alipay included more than 200,000 mini apps on its platform. Meituan, which just started to incorporate mini programs in 2019, had not released official numbers.

However, the Chinese super app system also poses a risk of data misuse, as third-party developers can have access to users’ data. Both companies are enforcing rigid data and privacy controls to earn users’ trust and avoid trouble. In early March of 2020, WeChat updated its privacy controls on third-party applications to limit the collection of sensitive personal details, and under the new rule, developers are expected to clarify how and what type of personal information is collected.

Other successful super apps in China using the mini program model include Baidu, Taobao’s Tmall, and Jd.com, while an array of other firms are also implementing mini programs on its main platform.

E-payment services, an essential ingredient

Regardless of the original business core and different routes these companies are taking to expand their ecosystems, many experts attribute the success of super apps to their native payment systems.

By establishing its own financial ecosystem, branching out to other verticals is faster and easier. As 290 million residents in Southeast Asia are still unbanked, apps offering convenient financial services are quickly amassing a large user base, putting them ahead in the race, according to credit research agency Fitch Ratings.

Gojek has envisioned this since its digital inception in 2015, when co-founder Nadiem Makarim laid the ground for a multi-service app, including payment service arm GoPay, while Grab only started in 2017. This resulted in Grab’s difficulty to beat Gojek in Indonesia. GoPay was the country’s most popular e-wallet platform, while GoFood also emerged as the preferred food-delivery service, according to a Nielsen survey in 2019.

Having an own payment system also eases inking partnerships with other service providers, and unlocks major spending potential for customers, as they can spend on more than one vertical in the app. WeChat mini-programs amassed a total of RMB 800 billion (USD 117.1 billion) in sales 2019, with the majority of its merchants reporting that 60% of their users were acquired through the mini-programs feature instead of the merchant’s own platforms.

Different markets, different futures?

Although the blueprint of super apps comes from China, it might come out differently in Southeast Asia, due to differences in market characteristics. Currently, most super apps are doing horizontal expansions covering sectors outside their core business model.

“The likes of WeChat, Alipay, and Meituan-Dianping wield enormous influence in China in due part to China’s size and relative homogeneity as a market. This isn’t the case for Southeast Asia, where the likes of Grab and Gojek will find it difficult to achieve WeChat-level ubiquity,” Insignia Ventures Partners founding managing partner Yinglan Tan told KrASIA.

Each country in the region has different needs, and each platform needs to adjust to address that demand. “Expanding a super app regionally means facing competition that’s either going down to the same super app path or focused on a specific service for that local market,” added Tan.

Furthermore, trying to emulate “China’s everything app” in Southeast Asia can also represent a very expensive strategy. “ It requires developing the super app to the local taste of each new market, putting together a local team to drive distribution and operations, all while competing with local players for each service offered,” said Tan.

Tan suggested a method that might find better success in the region, which he defined as the “hyper-vertical super app” model. Instead of tackling multiple sectors in one app, the hyper-vertical platform focuses on covering the entire customer journey around a singular product or vertical.

“The hyper-vertical model is a way for Southeast Asia’s tech companies to carve out market leadership by drilling down on what they are good at, rather than firing shots in the dark to see what eventually sticks,” said Tan, “This reduces the difficulties and risks that come with the challenging endeavor of regional expansion.”

One example is Carro, which started out as a used-car marketplace, but has since evolved to provide a variety of services for car owners, from repairs and maintenance to same-day insurance and financing. By becoming an all-in-one platform for car owners and dealers, users will repeatedly use Carro’s services for a longer period, Tan explained.

Another example is Tokopedia, which started out as an e-commerce platform but has gradually added more merchant-focused features such as lending service Dhanala and printing service Tokopedia Print. Although they don’t fit yet in the super app category, both platforms are already “super” in their own fields.

“Developing a super app is all about creating optionality for the business,” said Tan.