Nimut Sari had been operating her small kiosk in South Tangerang, Indonesia for six years when she decided to join the GrabKios platform in 2018. Before working with GrabKios, she only sold staple foods and small household items at her shop, but now Sari is able to offer digital payment services to customers, including phone credit top-ups and bill payments. Her customer base has been increasing ever since, Sari said.

Fintech solutions have showcased their potential to drive financial inclusion, which is a key driver of poverty reduction and greater prosperity. Before Indonesians began to leverage technology’s power to democratize access to financing, Chinese tech firms deployed fintech to reach China’s unbanked population, which remains the largest in the world.

Serving the most mobile payment users in the world, the country’s technology giants, namely Alibaba’s Ant Group and Tencent’s WeBank, have grown sizable businesses, partly due to their technology’s ability to provide financial products to people previously underserved by traditional financial institutions.

China’s fintech industry is reaching maturation following a period of explosive growth, which saw Chinese investment value in fintech comprise 46% of all global fintech deals in 2018.

With the third-largest unbanked population in the world behind China and India, Indonesia has increasingly looked to fintech solutions to increase access to financing.

Chinese investors and firms also see Indonesia as a prime market for fintech to excel, recognizing parallels to the Chinese market such as increasing mobile penetration rates among a digitally native, young generation, as well as rising disposable incomes prompting greater demand for fintech products from a growing middle class.

Encouraging growth in Indonesia

Indonesia’s promising fintech future is illustrated by the increasing number of licensed peer-to-peer (P2P) lending operators under the authority of the Financial Services Authority (OJK), as well as mobile wallet providers that are granted licenses by the central bank of Indonesia (BI).

As of June 2020, OJK has licensed 158 fintech lenders, and the number is expected to grow throughout the year. Meanwhile, BI has issued licenses to 51 e-money operators per May 2020, with major players like GoPay, Ovo, Dana, and LinkAja.

This swell of activity over the past few years in the fintech sector has translated into measurable results for Indonesians in search of greater financial inclusion. According to data compiled by OJK, the aggregate amount for loans in Indonesia from the fintech lending in May 2020 increased 166.03% year-on-year. OJK estimated there were more than 25 million borrower accounts, while there were more than 654,200 entities offering loans.

Meanwhile, for fintech payments, the total number of e-money transactions at the end of 2019 reached 5.2 billion, an increase of 79.3% from the previous year’s 2.9 billion transactions, according to BI’s statistics. The total nominal value of transactions reached IDR 145 trillion (USD 10 billion) last year, which was three times higher than 2018’s total amount of IDR 47 trillion (USD 3.2 billion).

This surge can largely be attributed to an influx of players exploring various fintech verticals in Indonesia. In addition to lending and payment companies, who currently dominate the country’s fintech landscape, more players from other segments like remittance, investment, and insurance have emerged in the last two years.

Investment in Indonesian fintech startups in 2020 remains healthy despite the COVID-19 crisis that has gripped the globe since the beginning of the year. Some of the companies that received new funding this year are P2P lender Investree (USD 23.5 million), SME-focused lender Akselaran (USD 8.5 million), and insurtech platform Qoala (USD 13.5 million).

The crisis could be a catalyst for fintech development in Indonesia and Southeast Asia, just as the SARS epidemic in 2003 hastened China’s launching of digital payments and e-commerce. Since Indonesia’s government forced people to limit physical interactions and remain confined in their residences for around three months, mobile wallet platforms like Ovo and GoPay saw an increase in traffic and new users.

The Indonesian fintech lending association (AFPI) also recorded surging demand for productive financing, especially from SMEs that need to keep their businesses afloat as the pandemic rages on.

Chinese entrance into the Indonesian market

Indonesia’s burgeoning fintech industry is attracting Chinese investors and fintech companies alike. Alibaba’s financial arm Ant Financial backs one of the country’s biggest mobile wallet platforms, Dana. In Alibaba-like fashion, Dana rapidly acquired market share in part thanks to partnerships with major e-commerce players Bukalapak and Lazada.

Moreover, Jakarta-headquartered lending firm Akulaku told KrASIA that it has raised USD 89 million from Ant Financial in 2018. Akulaku itself was founded by Chinese entrepreneur William Li, who is a former investment manager at Ping An Insurance Company, one of China’s largest insurers.

Another startup founded by a Chinese technopreneur is Oriente. Headquartered in Hong Kong, Oriente was founded by Hubert Tai, former CEO and CTO of Chinese financial product marketplace Lufax, along with co-founders Geoff Prentice and Lawrence Chu.

Oriente has a presence in three Southeast Asian markets—Finmas in Indonesia, a joint venture with Sinar Mas; Cashalo in collaboration with JG Summit Holdings in the Philippines; and Finizi in Vietnam. The firm is taking a leaf from Lufax’s playbook by teaming up with established businesses instead of entering the market solo.

The firm works with several Southeast Asian conglomerates such as Berjaya Group, JG Summit Holdings, and Sinar Mas to boost penetration by providing affordable financial products to the growing middle class in the markets they operate.

Meanwhile, Alibaba’s archival Tencent, as well as Chinese e-commerce firm JD.com, invested in GoPay’s parent company Gojek in 2017.

A number of Chinese tech giants also have fintech subsidiaries in Indonesia. This includes Xiaomi’s financial division, Mi Credit; JD finance from JD.id; and OneConnect Indonesia, which is a subsidiary of Ping An Group, a Chinese insurance company and consumer financing provider.

Read this: Crack open every wallet | Indonesia’s crowded fintech sector is about to change

Chinese companies’ influence on Indonesia’s fintech landscape goes beyond investment. According to a 2019 fintech lending report conducted by PricewaterhouseCoopers Indonesia, fintech lending in Indonesia is often compared to China. Indonesia has similar macroeconomic and socioeconomic conditions that are comparable to the widespread popularization of China’s fintech industry which began in earnest in 2013.

Nonetheless, there are always a few bad apples in every bunch. After Chinese regulators clamped down on a host of irresponsible online P2P platforms in 2017, many of these malicious firms were forced to explore new markets to find users. Quickly identifying Indonesia as an optimal expansion destination targeting a growing digital-native and mobile-first generation of young urban Indonesians with growing incomes, these unlicensed Chinese P2P players flooded the Indonesian market. In 2018, OJK revealed the existence of more than 100 unlicensed Chinese P2P providers in Indonesia.

Underserved populations, especially in rural areas where financial literacy rates are low, are particularly more susceptible to fraud and false advertising from bad actors.

To curb the mushrooming of illegal lenders, the OJK is collaborating with national police, cyber patrol, and the communication ministry to identify illegal lenders and warn people about them. As a result, the authority has blocked nearly 2,600 illegal fintech lenders in the past three years.

Similar fintech futures?

Even though the Chinese and Indonesian markets share numerous similarities, fintech companies in these countries have different approaches and business models. Chinese fintech firms focus more on short-term consumer loans, targeting hundreds of millions of low-income individuals who do not have credit cards. On the other hand, Indonesia fintech has a more balanced mix, as it focuses on both underserved individuals and micro, small, and medium enterprises (MSMEs).

Given its head start, China’s fintech sector is significantly more developed than Indonesia’s, providing a glimpse into trends and consumer preferences that may materialize in Southeast Asia in the future. China’s current status in fintech development is defined by a prevalence of mutual aid products, growing adoption of wealth management products, and microloans.

To differing degrees, Indonesian fintech players have taken some inspiration from China but have also localized their services to fit the Indonesian market.

Mutual aid

In the face of the COVID-19 pandemic, demand in China for mutual aid programs, viewed as a more affordable alternative to conventional healthcare insurance, has soared. Indonesia is also no stranger to the concept of mutual aid, or gotong-royong. Self-organized mutual aid groups are common in Indonesia, particularly in neighborhood communities and workers’ unions in the informal sector.

This propensity toward mutual aid also helped drive the rapid growth and popularity of digital crowdfunding platforms like Kitabisa, demonstrating the spirit of solidarity shared by Indonesians. According to an insurance tech report by CB Insights, more insurance business models from the US and China will land in Indonesia, and this may lead to the development of new mutual aid platforms.

Insurance penetration in Indonesia is very low, running at less than 3% of the total population. Digital insurance is still in its infancy, but has a promising future as more big tech companies like Gojek and Ovo are making moves in this segment too.

Wealth management

Indonesia has a robust middle class that is accumulating disposable income, leading to booming demand for wealth management products. In China, Ant Group’s Yu’e Bao money market fund and Ant Fortune’s various wealth management products offer Chinese users convenient access to financial options and have gained huge popularity.

Many of these wealth management platforms utilize robo-advisory services to make data-driven lending decisions and streamline the investment management process.

While this segment is still relatively immature in Indonesia, some firms successfully raised capital from big-name investors last year. Among them is Ajaib, which bagged USD 2.1 million from several investors including SoftBank Ventures, and Halofina that raised seed investment from Mandiri Capital, a corporate venture capital firm of state-owned Bank Mandiri. Other startups offering wealth management services are Ant Group-backed Akulaku and Moduit.

As the mass-affluent class in Indonesia is expected to increase by 8% per year from 2017 through 2030, more fintech companies are expected to tap the Indonesian wealth management market in years to come.

Consumer credit

Chinese fintech giant Ant Group’s Huabei Credit program allows users up to USD 7 in monthly credit, enabling them to purchase slightly beyond their means with no-interest installment repayments. Indonesia too has a burgeoning e-commerce sector that has increased the adoption of accompanying financial products, including business loans for MSMEs.

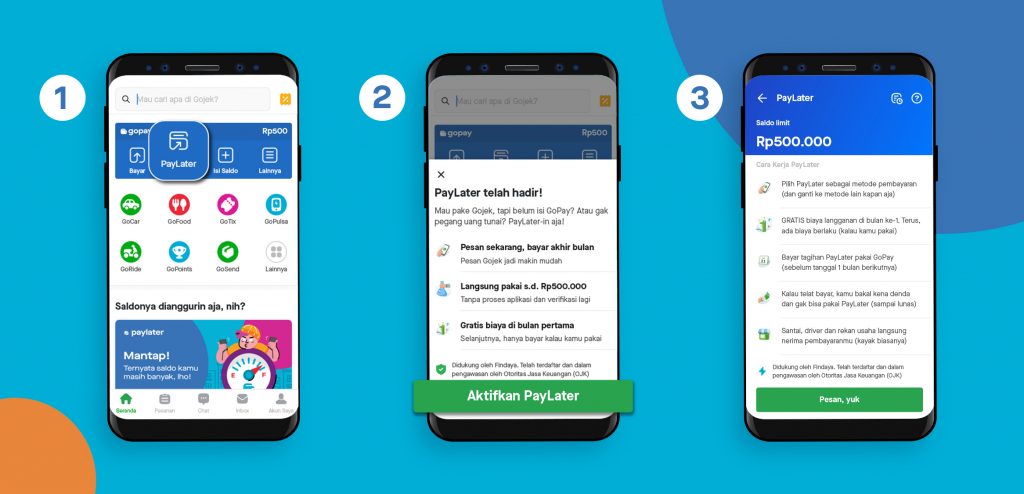

Indonesia’s fintech also has a similar product called “pay-later” that gives customers credit up to a limit, allowing them to shop or make transactions and pay down their balance over time. Pay-later functions as a substitute for credit cards, which are often seen as a luxury among Indonesian consumers.

The product started to take off last year, as it gained popularity quickly due to its flexibility, smaller installments, and affordable interest rates. According to Daily Social’s Indonesian Fintech Report 2019, it was the third most popular fintech product in Indonesia last year after mobile wallets and online investments. Today, nearly all major mobile wallets and their e-commerce partners, as well as online travel agency apps, have this feature on their platforms.

Despite the potential of Indonesia’s developing fintech ecosystem, the availability of these products is still concentrated in the country’s more urban and developed centers. To truly unleash the democratizing power of fintech in Indonesia, companies, and regulators must work together to reach underpenetrated rural areas.

In the second part of this series, we will look at fintech’s role in driving financial inclusion in Indonesia, particularly in the country’s rural areas.

(Correction: According to Akulaku, the firm has raised USD 89 million from Ant Financial (16th paragraph), not USD 40 million as stated before)