Myanmar counts about 80% of its 55 million inhabitants as unbanked, with no access to mainstream financial services such as bank-backed credit and savings accounts. However, as the country’s mobile penetration has risen to 126% in January, startups such as Mother Finance have come up with alternative solutions to lend money to the unbanked—based on smartphone data.

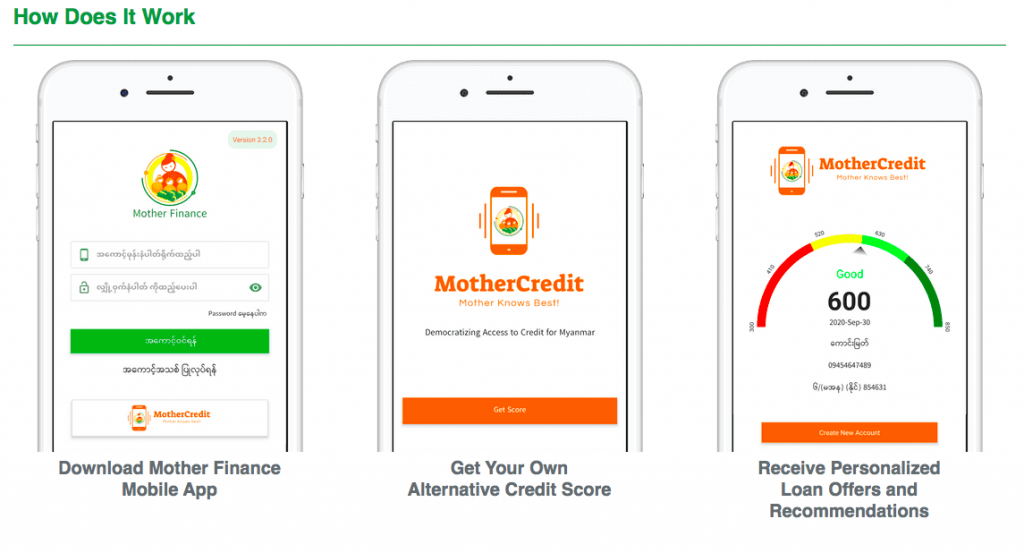

The Yangon-based fintech firm has developed a mobile application for people without credit history or bank accounts, which allows them to register on the platform and receive approval for their loans without stepping into a physical bank or microfinance office, all within 48 hours, according to the company.

The company bases its creditworthiness evaluation on an array of data including mobile data usage, calls, message records, location, browser history, and other vectors, which are collected through the company’s application, in addition to the applicants’ ID card and two guarantor referrals.

“We are the first one to actually do digital lending using smartphone data in Myanmar. We started making loans in 2018,” Theta Aye, managing director of Mother Finance, told KrASIA. Data collected from the app can even show if applicants go to the office during the day, or if any friends of applicants are on Mother Finance’s blacklist, she said.

Targeting the credit vacuum left by banks

When Theta Aye returned to Myanmar in 2016 after 20 years of working abroad, she decided to target the credit vacuum left by big banks, focusing on small and mid-size enterprises (SMEs) and the unbanked, particularly citizens from urban areas, who often found it difficult to acquire loans even when they had full-time jobs.

While Myanmar’s public credit bureaus only began operating this April, many consumers and small businesses still have difficulties accessing credit, and resort to informal lending or other microfinance institutions offering high-risk loans at high-interest rates. “There is no credit data in Myanmar,” Theta Aye said.

In 2018, she founded Mother Finance, supported by funds from local conglomerate Mother Group, which is involved in manufacturing, construction, logistics, and energy. The firm is now among the 27 non-bank financial institutions licensed by the Central Bank of Myanmar capable of offering financial services in the country.

From its founding, Mother Finance had to face many challenges, Theta Aye said. Among them, potential clients doubted the legitimacy of a fintech business in Myanmar without physical offices and were diffident of using mobile data to generate credit scores. The firm, however, gained popularity by first offering employee loans to citizens like civil servants, later expanding to other consumer segments. Currently, loan sizes range from MMK 25,000 to 100 million (USD 38 to 77,400).

To date, Mother Finance has processed over 70,000 loan applications and disbursed over MMK 6 billion (USD 4.6 million), while the default rate stood below 4% during the pandemic, according to Theta Aye. Borrowers with a track record of punctual repayment will be able to borrow more money, with interest rates lowered for subsequent loans. Defaulters, on the other side, will be blacklisted.

Read more: Myanmar’s mobile money services are scattered, spotty, and spirited

The credit score, which only takes 45 seconds to generate, is calculated based on Mother Finance’s credit scoring system. The grade ranges from 300 to 850 points, with higher scores indicating lower credit risk. Each user can check their credit scores up to four times each year to monitor their credit performance.

The interest rates are not fixed but depend on the risk level, personal financial history, and background of the individual borrower. Loan approval is issued within 48 hours, compared to about seven days for other microfinance institutions, according to Theta Aye.

Theta Aye affirmed that the company does not share any personally identifiable information, as the firm complies with local privacy laws and the General Data Protection Law, a regulation from the European Union (EU) that Mother Finance adopts for transparency.

“We also need to abide by central bank regulations to gather borrowers’ personal information as part of KYC [the “know your customer” process]. We do not believe we leverage any more data from your phone beyond what Facebook, Instagram, or Viber do,” Theta Aye said.

The ultimate goal of the company is to make credit available for the unbanked in a faster, cheaper, and creditworthy manner, according to Theta Aye. “Because we know that we are ultimately building an alternative credit scoring model, we set up our loan products to be short term, from a few days to a maximum of one year. We have a lot of repeat borrowers, over 76%, which allow us to derive credit profiles and the probability of defaults a lot faster,” she said.

Read more: The missing piece of Myanmar’s fintech puzzle

Weathering the COVID-19 crisis

While microfinance institutions have been hit hard during the COVID-19 pandemic’s second wave in Myanmar, as many borrowers were not able to repay their debts, Theta Aye told KrASIA that the crisis has helped the company obtain more data on defaults.

The firm, however, had to pause lending in April and May to collect outstanding loans, as the non-performing loan rate rose from 0.5% last year to 4% during the pandemic. Also, Mother Finance tweaked its strategy to adjust to the “new normal,” Theta Aye said. “COVID was helpful for us to get the algorithm calibrated. As with any other lending institutions, our non-performing loans (NPLs) increased five times during the first wave of COVID-19, but we were able to make use of the bad loan case data to improve our algorithm.”

Homegrown banks and other non-bank competitors have also woken up to the opportunity that Mother Finance has tapped into. Wave Money, one of the country’s leading mobile financial services providers, announced its plan to adopt Alibaba’s credit analysis technology and generate new credit scores for Myanmar’s consumers in August this year.

Another bank-led fintech platform, KBZPay, which is backed by KBZ Bank, also launched a loan for consumers in June, leveraging machine learning to determine the creditworthiness of the applications, according to KBZPay’s website.

“WavePay and KBZPay started to roll out digital loans as well, but our advantage is that anyone can receive and repay through multiple channels, not just tied to one bank or one wallet, which adds additional convenience. Bank-backed entities are also heavily regulated with capped lending interest rates, which do not allow them to take on higher risk,” she said.

With approximately 189 microfinance institutions operating in Myanmar, serving more than 5 million people with a total loan portfolio of around USD 500 million, the sector holds great potential for growth.

Theta Aye believes that Mother Finance can be more “adaptive” than its competitors. “We build out our operations, back-end system, and capabilities carefully before launching, instead of putting the feature just for the sake of showcasing. Rolling out a feature or functionality does not always mean that on-the-ground operations are ready and able to execute,” she said.

This article is part of KrASIA’s “Startup Stories” series, where the writers of KrASIA speak with founders of tech companies in South and Southeast Asia.