Ctrip, China’s largest online travel service provider, recently announced its better-than-feared first quarter earnings performance, but has fallen behind its global rivals such as Expedia and Booking.com.

China’s leading travel service provider of accommodation reservation, transportation ticketing, packaged tours and corporate travel management, Ctrip was known as the ‘growth’ star in the Online Travel Agency (OTA) sector, boasting of the ability to leverage its dominant one-stop online travel platform to capitalize on the burgeoning Chinese developing middle class and acquire market share in China’s ‘second-tier’ cities.

Not too long ago, the company was far ahead of even its global competitors, enjoying revenue growth in excess of 40% year-on-year, fuelled by the nation’s rising disposable income over the past decade, alongside travel-hungry Chinese millennials.

The C-trip Problem

China’s online travel Gross Merchandise Volume (GMV) was approximately at RMB738.4 billion in 2017, upped by 24.3% from the previous year, according to iResearch, a market research and consulting company.

Yet in the last quarter of 2017, citing seasonality and product change in domestic air ticketing, the company announced a mere year-on-year growth of 26%, as opposed to the seemingly easy forecast range up to 30%. Furthermore, its revenue figures declined by 19% from the previous quarter.

Ctrip’s snag in performance was a shock amidst very positive growth in China’s online travel retail. The biggest dip in earnings from the last quarter came from accommodation reservation revenue and transportation ticketing, specifically at 18% and 15% respectively.

Fast forward to this quarter, inherent issues that plagued the firm has yet to be completely solved.

According to a recent article by Chinese tech media TMTPost, Ctrip’s accommodation reservation sector growth was only at 23% and it has also been beaten by the company’s other competitors in other comparison metrics. Its transportation ticketing services was also alleged to have notoriously unjust refund policies and highly priced packaged tickets.

It is also interesting to note, despite a good ride till the shock financial performance last quarter, the macro environment for OTA is becoming more challenging – a spillover effect from Trivago, another OTA player, dismal results for the last quarter of 2017.

Higher fuel prices and potentially higher airfare are expected – which will affect Ctrip more, as unlike its peers, its main revenue driver is from transport ticketing.

In spite of all the impending doom and gloom, with some even calling Ctrip a ‘has-been’ and Expedia’s present low valuation looking like a better stock than the former, Ctrip actually beat its own forecast this quarter and is looking for revamp and change – looking to continue to provide excellent service for the huge potential in lower-tier Chinese cities.

How did Ctrip actually performed?

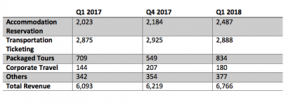

Data from Q1 Recap in Seeking Alpha Article is in RMB (million).

Data from Q1 Recap in Seeking Alpha Article is in RMB (million).

Ctrips’s revenues grew at 11% year-on-year to RMB 6.8 Billion, mainly driven by its rise in revenue from packaged tours and corporate travels, at 18% and 25% year-on-year respectively. Higher margins from these two segments definitely tilted the results to Ctrip’s favor even as core revenue driver – transportation ticketing dipped by 1% this quarter.

In line with the current pessimism, the company could not exploit operating leverage – with Product development, Sales and Marketing costs growing in line with revenue.

However, it managed to keep general and administrative expenses low, to benefit from the shift in product mix to garner profit via growth in the packaged and corporate travels.

This is reflected with its operating margin increasing from 6 to 9% over the past year.

Conclusion

Other than traditional competitors like eLong and Qunar, Chinese unicorn – Meituan-Dianping has also entered the sector to fight for market share, looking to topple the long-timed market leader, Ctrip.

The prospects of rising competition and expected decline in online travel this year, according to iResearch might be negative given Ctrip’s current predicament.

Pessimism, fuelled by negative media probably would burdened the stock price of the company. This story of a great company that stumbled into a low-growth trajectory – is an example of the negative consequences and unforgiving nature of the scrutiny in the public markets.

Nonetheless, with Ctrip data and Jing Travel, a leading voice for news and analysis on Chinese global travel, depicting two dominant trends in Chinese travel industry – namely growth in independent travel and long-term growth in lower-tier Chinese cities, the company is expecting a growth of 12-17%, even as it relies on experiences from past successes to rectify and continue to grow in China’s Online Travel Agency sector.