JD.com (NASDAQ: JD), one of China’s largest retailers, built its brand by cultivating an in-house logistics network that gives its services a sheen of timeliness and reliability. This made it stand out among China’s myriad of retailers, including Alibaba’s popular Taobao.com. Now, JD Logistics operates as a subsidiary that has taken on a life of its own—if all goes according to plan, it will be the fourth company in the JD network to have shares listed on a stock exchange, after JD.com itself, Dada Nexus, and JD Health.

On February 16, JD Logistics submitted its draft prospectus to the Hong Kong Stock Exchange, taking the first step toward an initial public offering (IPO). BoFA Securities, Goldman Sachs, and Haitong International are listed as its joint sponsors, with UBS as the financial advisor.

Reports have suggested the company’s valuation may hit USD 40 billion. This is higher than the market valuation of other logistics companies in China, with the exception of market leader SF Holdings (002352.SZ), which has a market valuation in excess of RMB 500 billion (USD 80 billion).

The details of the spinoff, such as the structure and scale of the issuance, have not been finalized yet. However, JD.com is expected to hold more than 50% of JD Logistics’ listed shares.

Trailing behind an industry leader

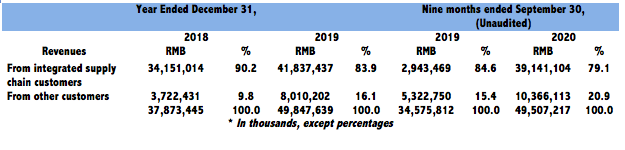

The parent company of JD Logistics deserves much credit for its success, with JD founder Richard Liu insisting on building a proprietary logistics network since 2007 despite the massive capital that it would demand. For the first three quarters of 2020, JD Logistics’ revenues hit RMB 49.5 billion (USD 7.6 billion), marking a 43.2% year-on-year increase from RMB 34.5 billion (USD 5.3 billion) in the nine months ending September 30, 2019, to RMB 49.5 billion (USD 7.6 billion) in the same period in 2019. Nearly half of this is drawn from third parties, while JD Logistics provided RMB 28 billion (USD 4.3 billion) worth of services to JD Group in the first three quarters of 2020, according to its draft prospectus.

SF Holdings’ revenue stood at RMB 90.9 billion (USD 14.1 billion) in 2018, RMB 112.2 billion (USD 17.3 billion) in 2019, and RMB 109.6 billion (USD 16.9 billion) in 2020.

Because this line of business is capital-intensive and carries immense overhead, JD Logistics has consistently been the most taxing operation among JD.com’s affiliates.

Despite its losses, JD has continued to recruit heavily and invest in operations in lower-tier cities and consumer-oriented packaging businesses. Its new lines in the health industry, cloud industry, and international logistics operations have resulted in a deficit of more than RMB 700 million (USD 108.3 million). In addition, its gross profit margins and losses are showing signs of improvement, driven by greater efficiencies in cost-management and economies of scale. Still, this pales compared to competitors SF Holdings’ and ZTO Express’ gross profit margins at 18.12% and 23.46% in the first three quarters of 2020 respectively.

Escalating overhead for labor also strains the company and is a ceiling to unchecked growth in the industry. At the end of 2020, JD Logistics had over 250,000 employees, including more than 240,000 who were involved in warehousing, express deliveries, and customer service operations. The cost of providing employee benefits went from RMB 17.1 billion (USD 2.6 billion) in 2018 to RMB 17.9 billion (USD 2.7 billion) in the first three quarters of 2020, with average salaries reaching RMB 8,287 (USD 1,283), according to the draft prospectus. In the same period, about half of its revenues were spent on employee benefits and outsourcing costs.

Still, employee welfare expenses as a percentage of revenues dropped from 45.1% to 36.1%, with outsourcing costs bumped up from 27.7% to 32.8%. This suggests the company depends more on third-party warehousing teams to reduce cost pressures stemming from an expanding labor force.

This is consistent with JD Logistics’ attempts to rebrand itself as more than a delivery company: it wants to shape an image of a technology-driven supply chain solutions and logistics service provider. The firm’s cumulative technology investments over the past 11 quarters have reached RMB 4.6 billion (USD 710.7 million), suggesting it may be a while before JD Logistics can truly reap the financial benefits of this transformation.

Integrated supply chain services as differentiating factor

JD Logistics says its supply chain is “integrated,” because aside from conventional logistics, it also provides express delivery, vehicle transportation, last-mile delivery, warehousing, door-to-door installation for certain products, and after-sales services. It also wants to be the preferred end-to-end supply chain solutions provider across multiple verticals, such as FMCG, fashion, home appliances, and groceries.

Looking specifically at JD’s POP (Platform Open Plan) program, JD provides four types of warehousing and distribution services for third-party sellers—SOP (sale on POP), FBP (fulfillment by POP), LBP (logistics by POP), and SOPL (sale on POP & logistics by POP) services. These four lines complement each other by carrying clients’ shipments through each link of the supply chain. For example, FBP provides sellers with inventory management and warehousing services; later on, LBP helps sellers pack orders and deliver them to JD’s sorting centers.

The number of customers using JD Logistics’ integrated supply chain services increased 42% from 32,465 at the end of 2018 to 46,083 by the third quarter of 2020.

Separately, a good sign is that JD Logistics is shipping more goods that are not e-commerce orders. The share went from 29.9% and 38.4% of revenues in 2018 and 2019 to 43.4% in the first three quarters of 2020. This is weaning the company off its parent’s e-commerce business – especially important given the intense competition in that sector, which has seen threats like Pinduoduo run neck to neck with it especially in new growth markets in lower-tier cities.

Yet, JD Logistics faces an uphill battle in matching the network density and ground logistics that its competitors have, especially in the skies. As of June 30, 2020, SF Holdings had 73 cargo aircraft and 2,004 flight routes. In contrast, JD Logistics had only 620 air routes and lacks its own planes.

Reaping returns for investors

JD Logistics went its own way to become an independent entity separate from JD Group in 2018. Since then, it has only sealed one financing round in February 2018, counting among its investors Hillhouse Capital, Sequoia China, China Merchant Group, Tencent, China Life, and China Development Fund. One of the stipulations for this investment was that JD Logistics had to go public within three years—by March 2021.

In February 2018, JD Group still held 81.4% of the company, which is valued at USD 13.5 billion. That stake has since been clipped to 79.12%, while Hillhouse subsidiary HHJL Holdings owns 2.9%, and Tencent subsidiary Image Architecture Investment holds 0.24%.

The logistics industry is crucial to everyday commerce, but it became a lifeline for people under lockdown when the pandemic hit in 2020. Many logistics firms have closed fresh financing rounds or performed secondary listings. For example, in May 2020, Suning Finance successfully issued six phases of supply chain finance asset-backed securities, totaling RMB 2.7 billion (USD 410 million) in bonds.

Three months later, Yunda Holding Investment Limited, a wholly-owned subsidiary of logistics provider Yunda, issued RMB 500 million (USD 77.4 million) in bonds too. Meanwhile, YTO pulled in RMB 3.8 billion (USD 588.4 million) in funding from Alibaba. Even market leader SF Holdings reported in November that it is planning for a USD 5 billion secondary listing in Hong Kong.

At present, JD Logistics’ services mainly revolve around warehousing and distribution services, express and cold chain transport, and cross-border deliveries. In August 2020, it acquired KY Express for RMB 3 billion (USD 464.5 million), folding a new footprint into its operations. Yet constant price wars have strained its balance sheet, especially in the hotly competitive grocery delivery market. JD Logistics will need fresh capital to build up its capabilities in lower-tier markets, which are the current battleground.

JD Logistics maintains a reputation for reliability due to its continual operations even during the height of the pandemic in China. Under the auspices of its parent company, JD Logistics has been constantly building new infrastructure since 2007. Still, it is in a race to scale up rapidly. Against a backdrop of logistics competitors looking for a slice of this pie, can JD logistics guard its niche?