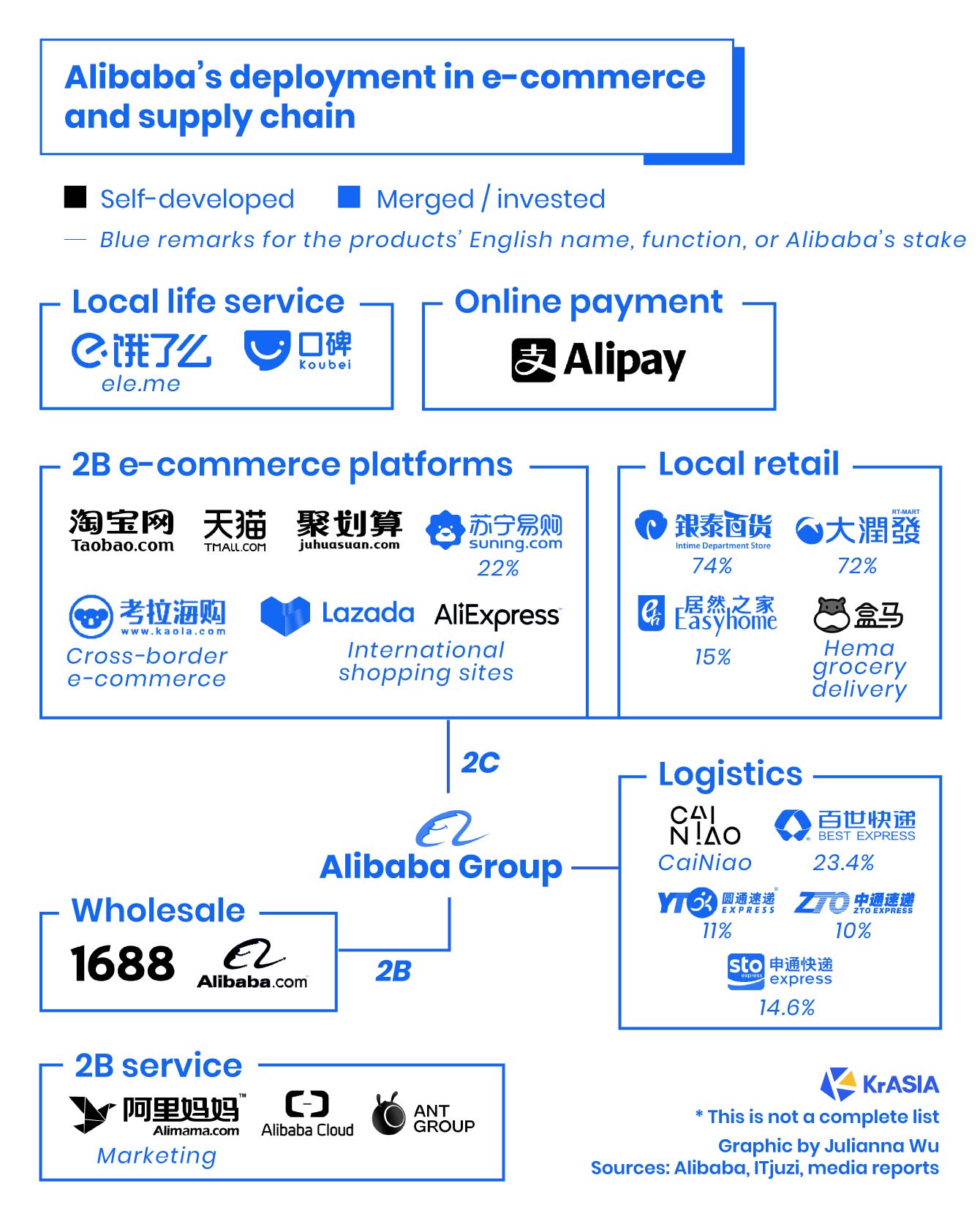

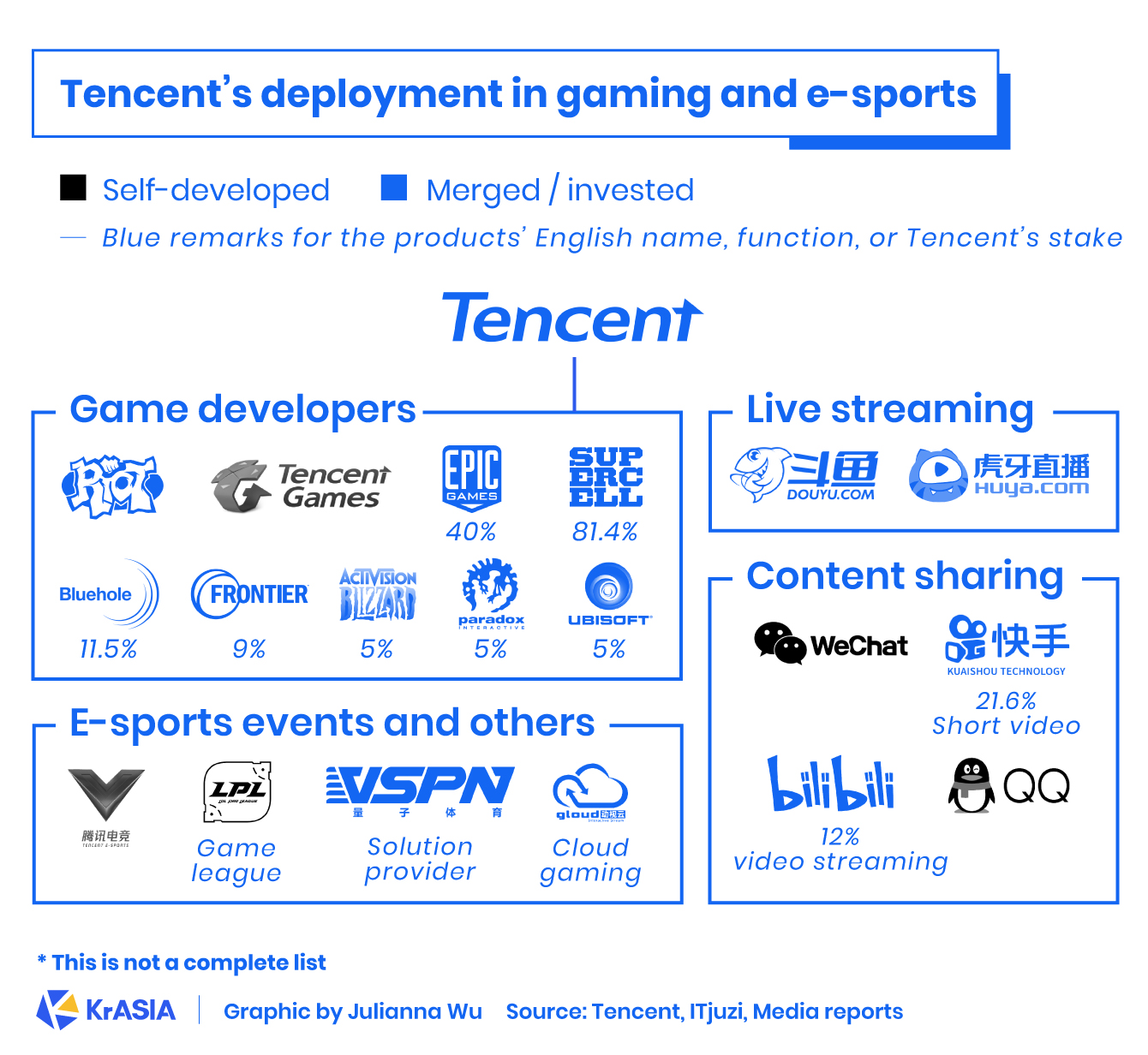

Chinese internet giants like Alibaba and Tencent have long dominated the investment landscape for domestic tech startups. These two firms in particular have created sprawling investment networks across a diverse range of sectors, the scale of which creates a huge demand for financing.

Following new antitrust policy drafts introduced in November 2020, pressure continues to mount on China’s tech giants.

In December 2020, e-commerce giant Alibaba (HKEX: 9988), Tencent-backed online literature company China Literature (HKEX: 0772), and SF Express-owned smart locker Hive Box were each fined RMB 500,000 (USD 76,500) for not reporting past deals for antitrust review, as China’s State Administration for Market Regulation (SAMR) indicated a newfound seriousness in investigating monopolistic practices in the internet industry.

Following the fines, at the Central Economic Work Conference held at the end of 2020, regulators listed “strengthening anti-monopoly and preventing the disorderly expansion of capital” as a key task for 2021.

VIEs come under pressure

Starting with Sina in 2000, Chinese internet giants like Alibaba, Tencent, Baidu, and Meituan have used corporate structures known as variable interest entities (VIE) to circumvent domestic rules on capital activity and pursue an ambitious investment strategy of horizontal expansion.

Chinese regulation bars foreign ownership in certain sectors like the internet, so firms use VIEs to raise capital from overseas investors to expand and grow their domestic business.

But it seems that an era of lax oversight and unencumbered growth is coming to end. In the 12 years since China’s first iteration of antitrust law was promulgated in 2008, virtually none of the deals in the internet sector have been reviewed by regulators.

“The most important change in the 2020 antitrust regulation is that companies with VIE structures were included in the regulatory review for the first time,” Deng Zhisong, senior partner at Dentons China, told KrASIA.

Though the new antitrust guideline didn’t provide a definite conclusion on the legitimacy of VIE’s, a draft of the Platform Economy Antitrust Guidelines published on November 10, 2020, explicitly stipulate for the first time that transactions involving VIE structures must be reported for anti-monopoly review.

“The Chinese government has not given it a definition, you can say it is both illegal and legal,” explained Deng.

For heated sectors like neighborhood group-buying and online education, the new draft suggests the capital inflow into these burgeoning sectors from internet giants will abate slightly, Deng said.

None of this means that Chinese companies’ use of VIEs will come to a halt, but the tide may be stemmed as the transactions fall under increased scrutiny. Beijing still prioritizes attracting foreign investment and business more broadly, and coming down too hard on VIEs would undermine that goal.

Impact on investment activity

The policies are likely to increase the due diligence period for investments from internet giants, according to Deng, slowing down agile investors at top Chinese tech firms.

Transacting companies with an annual domestic turnover of over RMB 1 billion (USD 150 million), or a global turnover of RMB 10 billion (USD 1.54 billion), are required to report their deals.

“The investment activities in the market, in general, would certainly be slowed down,” Deng said. “But we should not say that it is an obstacle to the development of the market, it’s to implement law enforcement and to restore VIE companies’ investment activities to a normal state.”

Companies like Alibaba and Tencent have created robust ecosystems within China’s digital economy, both of which thrived from the digital transition brought on by COVID-19, as demand for cloud computing, e-commerce, gaming, and livestreaming further strengthened the two giants’ duopoly in Chinese technology.

The penalties for any company not reporting deals for review have also increased substantially under the new rules, with a maximum fine of 10% of a violator’s annual sales. The policy goal is to compel companies to adopt a proactive approach to declaring deals.

“It can be predicted that after the formal adoption of this clause, operators will take the initiative to supplement, negotiate, declare, and surrender to a large number of circumstances,” according to a Dentons China report acquired by KrASIA.

The scope of deals that fall under review has also widened, with minority stakes and joint ventures potentially subject to review as well. But that isn’t really what the new regulations are meant to guard against.

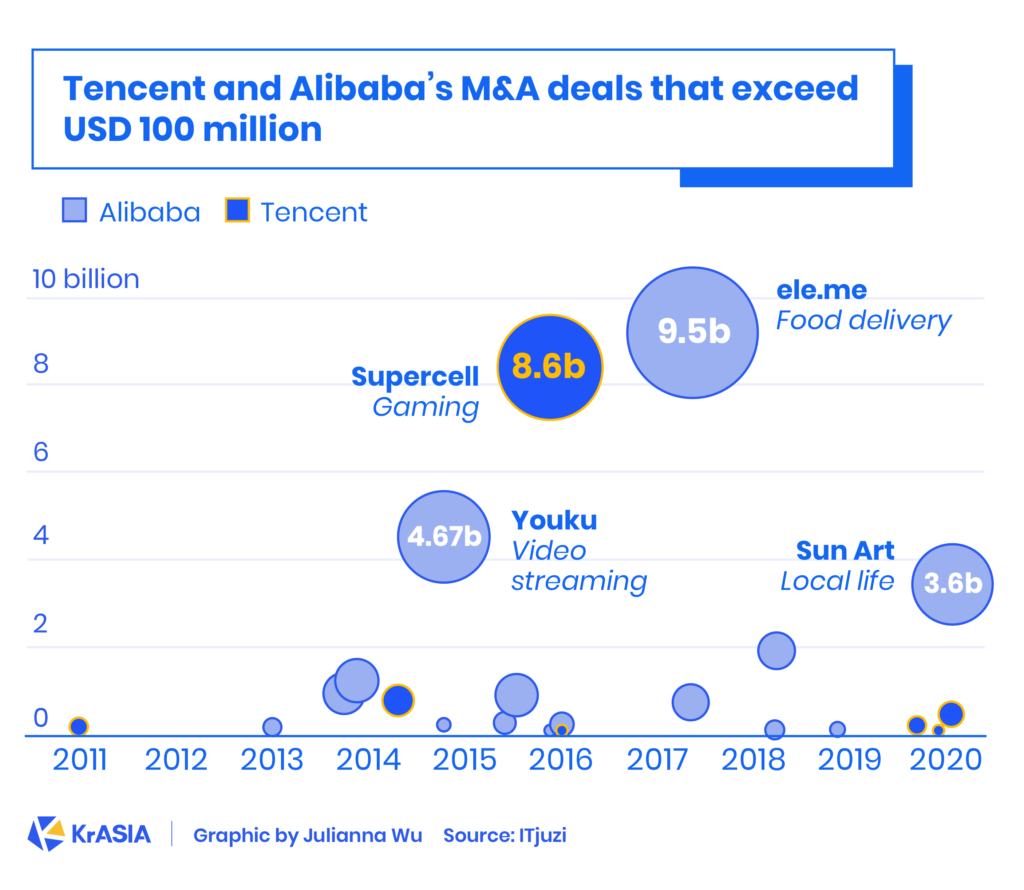

Instead, the days of mega-deals like Didi’s acquisition of Uber China in 2016 or Alibaba’s USD 9.5 billion investment in Ele.me in 2018 are likely coming to a close, as policymakers aim to preserve fairer competition and limit the massive leverage of Chinese tech giants.

In December 2020, regulators launched an antitrust probe into a Tencent-orchestrated deal worth around USD 6 billion to combine China’s two largest e-sports livestreaming platforms, Douyu and Huya. The deal, expected to be completed in the first half of 2021, would cement Tencent’s preeminence in gaming by dominating a game livestreaming market that consists of around 340 million users with a market value of RMB 23.6 billion (USD 3.4 billion).

However, the regulation is not suffocating and is more or less on par with other markets.

Since China began to implement antitrust law in 2008, SAMR has reviewed 4,000 M&A deals so far, banning two and granting conditional approval to four. The ratio of violation is similar to that in other global markets, according to Deng.

While it remains to be seen whether more antitrust violations will occur in a harsher enforcement environment, it may slow the flood of investment from internet giants while encouraging these companies to proactively seek government review of future investment activity.