Environmental, social, and governance (ESG) investing standards have assumed greater importance in recent years across the world. An increasing number of investors, bankers, and customers are demanding that businesses improve their ESG practices.

First proposed in 2005 in the Who Cares Wins report by the UN Global Compact, the idea of social and sustainable investing comes from the thesis that capitalism has obligations beyond creating economic profit. In other words, instead of only considering return on equity, investors and companies also need to weigh in their impact on customers, employees, local communities, the environment, and society in general.

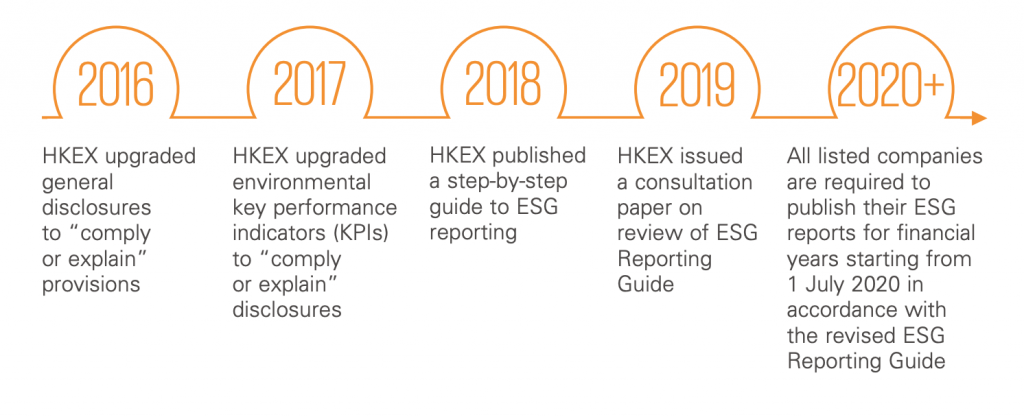

Although ESG standards are not new, Chinese companies have only recently begun to take these measures seriously. Last year, the Hong Kong Stock Exchange (HKEX) announced that starting from July 2020, all exchange-listed companies will have to produce a statement regarding ESG risks, as well as determining what ESG matters are material to the business.

The stock exchanges of Shanghai and Shenzhen are also expected to require all listed companies to increase ESG disclosures, according to The Financial Times.

What do ESG standards consider?

To assess a company based on ESG criteria, investors look at a broad range of behaviors under environment, social, and governance factors. However, there are currently no uniform international standards for ESG.

The environmental factor analyzes the company’s ecological impact and policies such as waste management, emissions impact, energy consumption, and environmental protection. The social factor looks at the company’s labor standards, employee relations, equal employment, and the firm’s impact on local communities. Lastly, the governance factor considers the company’s policies such as ownership and structural transparency, investor voting rights, independence of the board/oversight, business ethics, and executive compensation fairness.

Supporters of ESG standards claim that social investing will finally force companies to become better corporate citizens. “Paying attention to ESG standards does not compromise returns—rather the opposite,” according to a study by analyst firm McKinsey, which found that 63% of companies practicing ESG standards had positive results on equity returns.

How are Chinese companies performing?

There seems to be a growing awareness and appreciation towards ESG investing among Chinese companies. However, many local firms have not yet fully put ESG standards into practice. This is mainly because most Chinese companies and investors do not think about profit and social value together.

“This is a natural result of the Chinese governance model,” says Mathias Larsen, director of International Cooperation at the Institute of International Green Finance, an independent think tank in Beijing.

“While most Chinese companies are very narrow in their focus on doing profit-maximizing businesses, social objectives, such as green development or poverty alleviation, are set by the government. The government is channeling these companies into doing social good by various financial incentives, for example, by giving interest rate subsidies for loans into green categories,” he explained to KrASIA.

Therefore, businesses do not really need to think about their social impact. Instead, the government makes companies invest in sustainable projects by offering certain incentives. However, this system does not really result in Chinese companies embedding ESG standards into their operations successfully.

The social factor of ESG may be the most challenging. Companies need to make some fundamental changes in this area to attract more investors. Chinese technology companies, such as Alibaba (HKEX: 9988), ByteDance, Baidu (NASDAQ: BIDU), Tencent (HKEX: 0700), and Huawei, are known for a ‘996’ workplace culture, meaning employees work from 9 a.m. to 9 p.m., six days a week.

Moreover, discrimination in the job market is another issue. Many ads for companies suggest bias based on appearance, gender, or age. For instance, Baidu listed a job for content reviewers in March 2017, stating that applicants had to be men with a “strong ability to work under pressure, able to work on weekends, holidays, and night shifts.” Moreover, some job postings require women to have certain physical attributes regarding height, weight, voice, or facial appearance, especially for sales related positions.

Also, many Chinese listed companies have an opaque and confusing ownership structure, where investor voting rights have no actual weight.

Huawei is a good example to see how confusing the governance structure of Chinese companies could be, even if the company laid out details of its ownership structure in an attempt to refute critics over the company’s claim that it is owned and run by its employees.

A study called Who Owns Huawei?‘ by scholars Balding and Clarke highlights that Huawei is a company 99% owned by an entity called a ‘trade union committee,’ however, the two academics failed to find any information about the internal governance procedures of the trade union committee, its composition, and how the members are selected.

Another complicated structure in Chinese companies’ governance is the variable interest entity (VIE). Chinese tech companies have set up this system to be able to take in foreign investment, even when the Chinese law bans foreigners from owning stakes in them.

In order to attract foreign investors, many Chinese companies formed holding companies in tax havens and listed their shares in New York or Hong Kong. But the problem is by doing so, they made themselves categorized as ‘foreign firms’ in China. That in turn prohibits them from owning assets in some politically sensitive sectors such as the internet – a vital sector for tech companies.

These companies solved the problem by shifting the sensitive assets, such as operating licenses of the companies, into special legal entities -VIEs- that are owned by Chinese individuals, usually the firms’ bosses. The companies sign contracts with the VIEs and their individual owners. Investors do not have a direct ownership stake in the entity but rather have special contracts, which enables a controlling interest. Alibaba and Tencent are using this structure.

Perhaps, the environmental factor could be the most achievable for most companies, as the Chinese government has also made sustainable development a top priority. For example, the country established a carbon trading system and set carbon emission quotas for various industries in an effort to reduce pollution.

However, overall progress has been slow. Most tech companies are still far away from using renewable energy in their operations. According to the Clean Cloud 2020 report by Greenpeace, which analyzes the Chinese tech industry’s clean energy scores, Alibaba and Tencent were specified for their lack of initiative to switch to cleaner energy sources.

Another issue that Chinese tech companies need to solve is ESG reporting. Chinese firms do not publish enough data to show whether they qualify for ESG funds. When they do, the quality of information is uneven, making it hard for investors with an ESG mandate to make judgments on suitability.

“While there are discrepancies in ESG reporting internationally, these differences are greater in China compared to the West,” Larsen told KrASIA.

“Chinese companies follow different frameworks in reporting and they usually find the measures that would make their performance look better. For instance, they often report how much CO2 was saved, but they don’t report how much CO2 was released. Also, they wouldn’t make clear ‘how much was saved’ in comparison to what metric. Is it compared to the industry average or to the technology available etc,” he added.

According to Larsen, in Europe and the US, more companies are disclosing their ESG performance in a relatively more uniform format, which allows investors and rating agencies to make a better assessment. Whereas in China, the situation is rather complicated.

In 2019, 85% of Chinese Securities Index (CSI) 300 companies released annual ESG reports. However, among those companies, only 12% had audited reports, according to a report by Ping An Digital Economic Research Center on ESG disclosure in China. This means that most of the companies were measuring their progress by themselves.

It’s not all bad news, though. There are some Chinese firms like Lenovo which are doing better in terms of embedding ESG standards. According to the Red Pulse market intelligence platform, Lenovo (HKEX: 0992) improved its ESG performance compared to previous years. The company decreased its carbon emission while implementing energy efficiency systems.

At the same time, Lenovo increased its net employee creation, improved health and safety policies for workers, and revealed the details regarding their governance. The company ranks high level at corporate social responsibility metrics.

Another company that ranks high in corporate social responsibility metrics is China Mobile Limited. According to the firm’s sustainability report, its overall energy consumption per unit of information flow decreased by 57% while the overall energy consumption per unit of telecom business decreased by 53%, compared to previous years. The company also established an employee assistance program where they provide all-year-round psychological consultation for employees, among other ESG measures.

Future of ESG disclosure

The good news is that sustainable investing deploys more than USD 30 trillion worldwide, and the Chinese government wants to enable Chinese companies to raise capital from ESG funds. Therefore, authorities are urging companies to say more about their ESG risks.

The country has seen a significant uptake of ESG investing in the last couple of years. While current practices are below the ESG standards abroad, the situation might improve through government-supported initiatives. This might require Chinese companies to substantially improve their treatment and disclosure of ESG risks and to remain accountable to the environmental and social commitments.

“This hands-on approach to green finance is very efficient in China. Although the country launched its green finance policies only in 2016, China is now the biggest market across many of the green finance instruments. This determination and support from the government showed its effects much faster than what we’ve seen in Europe. And in terms of ESG disclosure, Chinese companies will have to take it seriously as the government demands it,” Larsen explained.