Netti Husna is a public high school biology teacher in South Tangerang, on the southwestern border of Jakarta. In the evenings, Husna teaches Arabic on her front porch, where the children of Muslim families gather to read the Quran’s formal language. A devoted Muslim, Husna does her best to live her life according to Islamic teachings. She follows the rules that have been mapped out by generations of holy men, including how she handles her financial matters. The 50-year-old is meticulous about selecting financial services that match her needs.

“I don’t use a credit card and I never borrowed money from conventional financial institutions as they charge interest, which is part of riba, a practice that is prohibited in my religion,” Husna told KrASIA. The caution she exercises now extends to fintech products too. “I’m okay with mobile payment platforms because it is allowed by the Indonesian Ulema Council [MUI], but I don’t use their ‘pay later’ feature because it carries a principle like credit cards,” she said.

In the past few years, sharia-based fintech platforms have sprung up in Indonesia, offering a basket of services such as loans for micro, small, and medium enterprises (MSMEs), as well as financing for hajj and umrah (pilgrimage to Mecca). Collaborating with Islamic banks, sharia fintech firms bring Muslim communities into the fold for financial services. However, sharia fintech is nowhere near as comprehensive as conventional platforms.

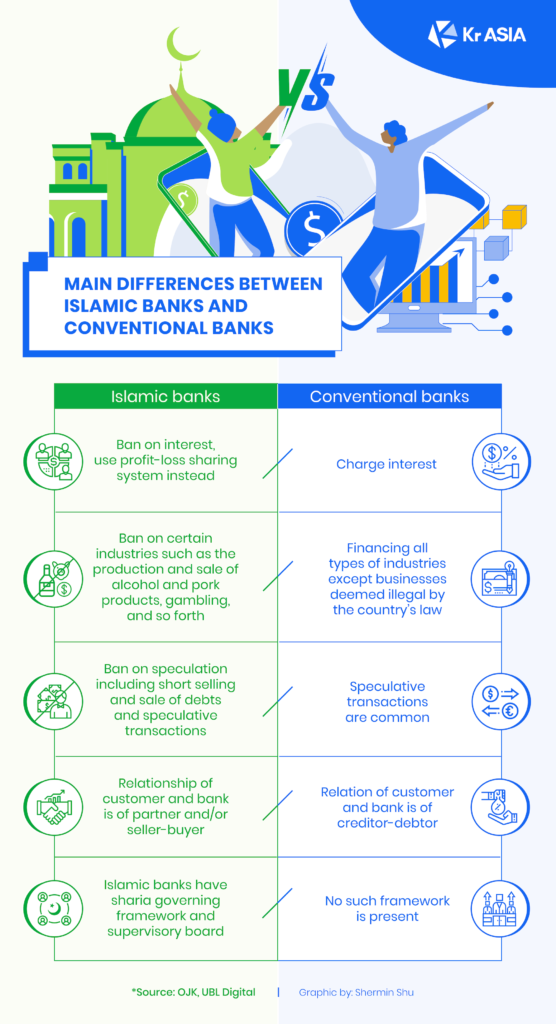

Husna and millions of other Muslims in Indonesia rely on sharia finance and banking options that adhere to Islamic law. One fundamental principle is the prohibition of interest charged by lenders and investors. Instead, sharia banking invokes a system where profits and losses are shared. Any form of income from speculation (qimar) or chance (maysir) is also forbidden, as well as the participation in contracts that carry excessive risk (gharar), like short selling in stock and commodity markets. Moreover, funds deposited into sharia-compliant banking institutions are not used to support industries that are haram—sinful according to Islamic law—such as the production or sale of alcoholic beverages and pork products, gambling, and anything related to pornography.

There are 225 million Muslims residing in Indonesia, the largest Muslim population in a single country. In order to advance the sharia economy, President Joko Widodo launched Bank Syariah Indonesia (BSI) on February 1 by merging three state-owned banks—Bank BRI Syariah, Bank Syariah Mandiri, and Bank BNI Syariah—making it the largest Islamic bank in the country. BSI is a new milestone for the Islamic economy in Indonesia. The government and other stakeholders expect BSI to become one of the largest Islamic banking institutions in the world.

Husna is a long-standing customer of Bank Syariah Mandiri. She is not sure how the merger will impact customers like her, but she hopes that BSI will provide better and more comprehensive sharia services for Muslims.

Sharing infrastructure for sharia fintech

BSI has core capital of around IDR 20.4 trillion (USD 1.4 billion). It aims to bump that amount up to IDR 30 trillion (USD 2.1 billion) by 2022. This will strengthen the sharia fintech infrastructure, according to Lutfi Adhiansyah, CEO of fintech platform Ammana.

“There are no Islamic banks that issue their own e-money, because some digital services such as lender fund accounts and payment gateways can only be issued by BUKU 4 banks [which have the prerequisite of holding IDR 30 trillion in core capital]. Current mobile banking services are also quite limited, customers can’t open online accounts or use digital signatures. The technology of sharia banks is not as sophisticated as conventional banks,” Adhiansyah told KrASIA. He also serves as the head of sharia cluster at AFPI, the Indonesian fintech lending association.

With some fundamental changes that BSI can provide momentum for, fintech platforms can mesh with the halal megabank and tap segments outside of lending, such as credit scoring, e-KYC, digital signatures, and so on, said Adhiansyah. Simply put, the scale of BSI gives it the opportunity to reach further than the three institutions that form its foundation.

The banks forming the backbone of BSI will integrate their customer data, making it easier for fintech companies that work with BSI to offer services to its customers. At the macro level, the presence of Bank Syariah Indonesia shows the government’s intention to make Indonesia a center for sharia economies at a regional and global scale, on par with Malaysia and its Maybank Islamic, the biggest sharia bank in Southeast Asia, or even Saudi Arabia and its Al Rajhi Bank, which is the largest Islamic bank globally.

Dima Djani, co-founder and CEO of P2P lending platform Alami Sharia, expects that BSI will formulate newfound support for the sharia fintech ecosystem, especially when it comes to previously limited options for funding, which includes institutional lenders for P2P lending and equity financing for the company itself. “If we look at conventional banks like Bank BRI or Bank Mandiri, they provide end-to-end infrastructure to regular P2P lending platforms. They have corporate VC arms that provide equity for fintech. On operational side, they provide lender’s fund accounts that make it easier for lenders to make funding transactions in fintech platforms. These are still lacking in sharia fintech.” Djani added that with an increase in assets, BSI can direct more funds through fintech platforms.

However, he tempered that prediction with an expectation of slowness. “The merger process is very complicated, especially when it involves three large banks. They have to integrate systems, databases, as well as teams, including those related to fintech partnership. It takes time for the banks to complete the integration before they move to the next plans,” Djani said.

Djani believes many sharia financial institutions find it difficult to compete with entities that offer conventional services, whether in terms of pricing, range, or technology. “That’s why the government is very supportive of BSI. But it needs to speed up, run twice as fast as conventional banks that are already equipped with advanced technology. Maybe, one day, BSI will also transform into a sharia-compliant digital bank, but it is unlikely to happen in the near future,” he said.

The struggles of sharia fintech and the Islamic economy

Indonesia is home to 12.7% of the world’s Muslims, a bigger portion than any other country. But that itself is apparently insufficient to invigorate the country’s sharia economy. Indonesia still lags behind Malaysia, which leads the industry globally, according to the State of the Global Islamic Economy Report published in 2020 by Salaam Gateway, a news platform that covers developments in the Muslim-focused economy. Indonesia trailed behind in fourth place.

As of June 2020, Islamic banking assets sit at IDR 545.39 trillion (USD 39.22 billion), 9.22% higher year-on-year, and total funding distributed reached IDR 377 trillion (USD 27.1 billion), according to data compiled by the country’s financial authority, the OJK. The market share of Islamic banking is 6.18%, with 196 institutions consisting of 14 Islamic commercial banks, 20 Islamic business units, and 162 sharia smallholder financing banks.

Among the population, Islamic financial literacy is low, at around 8% in 2019, while the nation’s general financial literacy is at 38%, according to OJK’s data.

Fintech startups that operate within this niche segment must weather various challenges such as low Islamic financial literacy and incomplete infrastructures. Out of the 149 fintech lenders that are licensed and registered with the OJK as of January 2021, only ten are fully sharia-compliant. Last year, the OJK revoked the license of sharia fintech platform Syarfi Teknologi, and cancelled the registration for another called Danakoo as they couldn’t meet the OJK’s requirements.

Nonetheless, Lutfi Adhiansyah is optimistic that sharia fintech, especially lending, will see wider usage and stabilize in the coming years. “During the pandemic, sharia lending platforms distributed around IDR 1.7 trillion, up from last year’s IDR 1 trillion. This shows surging demand in this sector,” he said.

There are financial institutions and fintech firms that offer conventional as well as sharia financial services. The diversification is meant to cater to different types of clients, but at times backfires—conservative customers cast doubt on the authenticity of sharia-compliant financial products if they believe their money might be blended with cash that is handled in non-Islamic ways.

Adhiansyah believes there is a need for strict separation between conventional and sharia financial services in order to build and maintain trust among customers. This is key to making Islamic finance broadly serviceable.

Yet another snag is the lack of funding. So far, there are no venture capital firms dedicated to supporting sharia platforms, and investors have favored financial service providers that run Islamic financial options alongside conventional services. That means dedicated platforms are often overlooked when investors seek targets to write checks for.

The only sharia fintech startup that recently raised new capital is Alami, which bagged USD 20 million in an equity and debt funding round last month, following its seed round led by Golden Gate Ventures in 2019. The startup claimed to be the first to raise a “sharia-based VC funding scheme,” referring to a structure in its capital arrangement as compliant with Islamic rules. In a previous interview with KrASIA, Djani explained that sharia profit-sharing scheme is similar to equity financing.

“There are several VCs who are interested in exploring sharia fintech, but they eventually prefer to make an investment in regular companies with sharia business units, as it is considered to be easier and less risky. I think it is important for regulators to separate the two types of business, and I hope BSI will inspire other institutions, including fintech, to spin off their sharia business units into fully sharia-compliant companies,” said Adhiansyah.

In spite of the many challenges, industry insiders believe that the newly established mega sharia bank can be a foundation for sharia fintech in Indonesia and beyond, helping this niche segment grow and compete with established conventional players.