KrASIA’s Morning Briefing is a closed-door presentation that delves into a different industry every 1st and 3rd Tuesday of the month. Register here for the upcoming episode on the growing plant-based meat industry in China, June 1, 9 – 9.30am (GMT +8).

In this episode, the team gave a brief overview of the sportswear industry in China and delved into trends that have influenced development over the years. To round things off, ANTA was discussed as the case study.

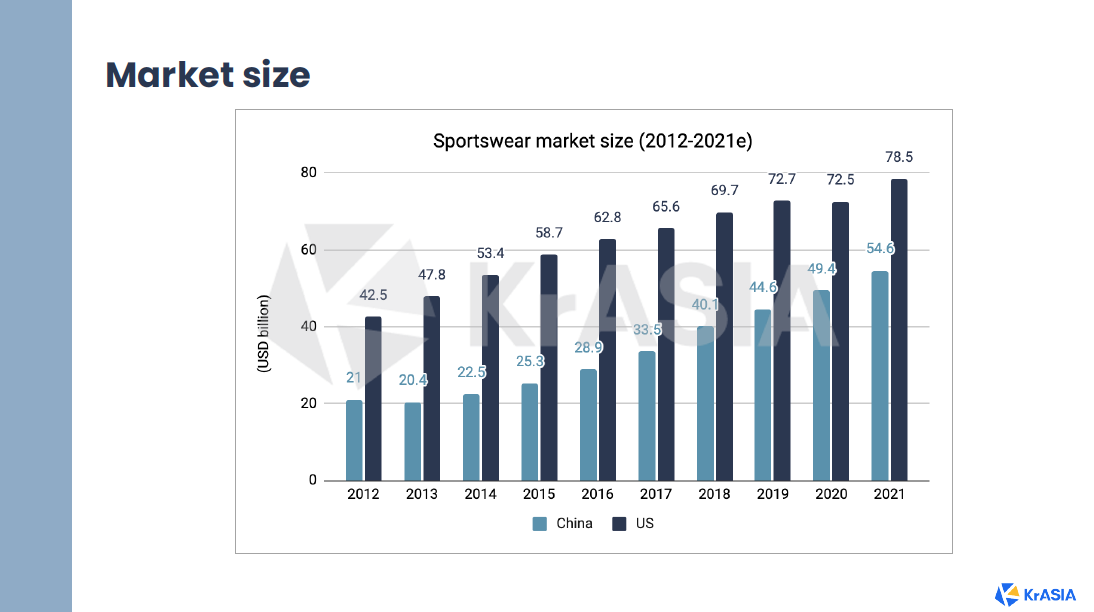

By way of introduction, the size of the Chinese market was compared to that of the US, demonstrating the exponential growth seen in the past in the past decade.

Macro conditions such as a higher awareness of fitness and consumers changing preferences for sportswear have contributed to such market expansion. Trends such as athleisure has opened more channels for sportswear brands to create and market the image of an active yet fashionable and comfortable, aspirational lifestyle to consumers, ultimately opening up more occasions for which consumers can shop for.

Additionally, as consumers’ spending power increases and show preference for more premium products, brands and manufacturers follow suit and launch higher-end products with prices to match. With consumers preferences upgrading and prices inflating, market scale is set for continual growth. Industry consolidation is also expected due to the high barriers of entry in the sportswear industry — given the technical and functional attributes of the products and uneven distribution of marketing resources, it is capital intensive in nature. Moreover, there are already many different brands competing in different spaces of the industry.

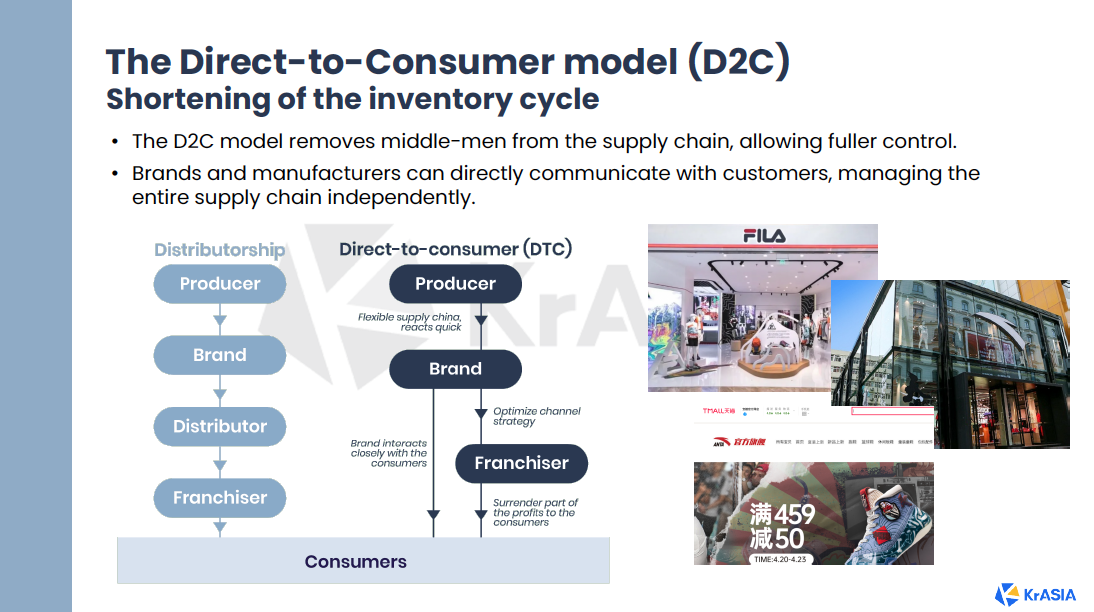

The team then zoomed in a little closer into the aforementioned factors that have been influencing the industry. This included expounding on the growing versatility of sportswear and apparel, the direct-to-consumer (D2C) model and the rise of the national trend (国潮).

The D2C model, in particular, brings about operational changes as it shortens the inventory cycle. In a nutshell, D2C removes middle men from the supply chain, allowing brands and manufacturers fuller control and flexibility over their products. It is characterized by manufacturers directly communicating with customers and independently fulfilling the entire chain from design to production, to marketing and sales.

However, not all brands and manufacturers have the resources to adopt the DTC model at a large scale as it requires comprehensive reform of the supply chain which includes aspects such as warehouse and inventory management as well as distribution channels and frequency.

Moving on, the team discussed ANTA as the case study for the episode.

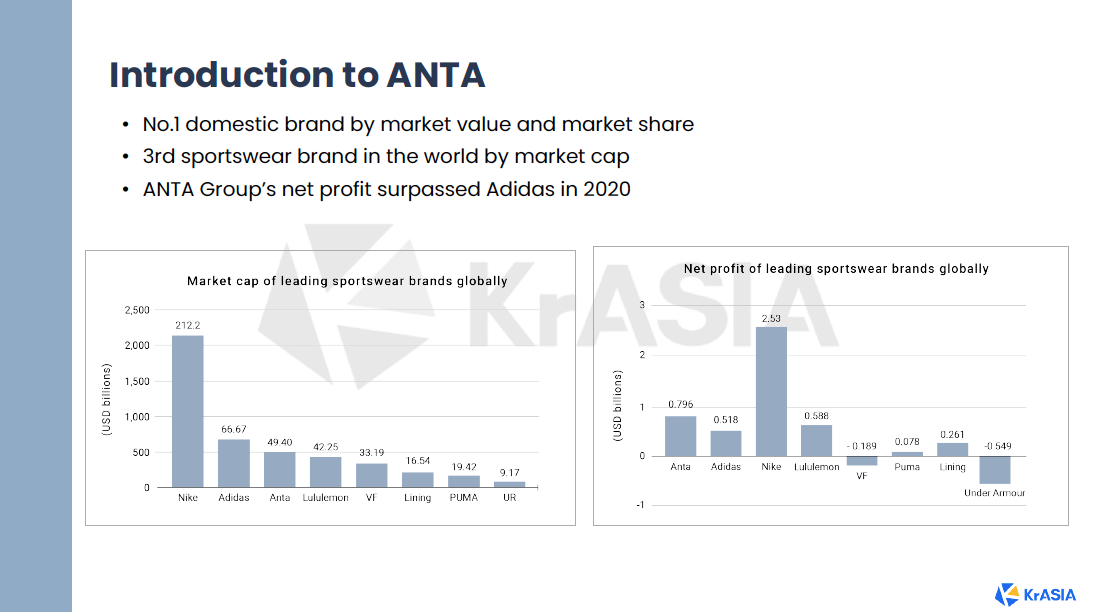

ANTA is currently China’s leading domestic sportswear brand by market share and is third in the world by market cap. In 2020, based on net profit alone, ANTA surpassed Adidas for the first time in China, recording USD 796 million to Adidas’ 518 million.

Delving into strategies that have contributed to ANTA’s success, the team first discussed ANTA’s management over its entire supply chain.

At the beginning of its establishment, the company was mainly a shoe OEM factory, coming from CEO Ding’s family roots as a shoe factory. Overtime, however, the company has built up its capabilities across the entire supply chain, from R&D to design, manufacturing, distributorship and even its own dedicated logistics team. This was a key differentiator against domestic competitor Li-Ning.

ANTA was a shoe manufacturer before becoming a full-fledged brand and despite costs in maintaining their own facilities, Anta was able to reduce third-party manufacturing and have better control over the supply chain. Li-Ning on the other hand did not have any proprietary production facilities until 2019. Both companies were bullish on market growth due to their growth in revenue spurred by the Beijing Olympics in 2008. Over-expansion during that period, had led to both opening too many stores and over-stocking on their product lines, costing both companies heavily.

Given the extensive control and purview of their entire supply chain, ANTA was able to quickly implement its own ERP (enterprise resource planning) system for the distributors and used their sales data to better manage the sales channels. This allowed the company to give advice to distributors on which clothes to purchase and at what quantity, with prompt feedback. Thus maintaining trust with distributors after observing how ANTA was working in tandem with them. Li-Ning on the other hand was unable to come up with a system that was able to benefit both parties.

ANTA was also able to new ways of growth through its acquisition of FILA China. At the time of acquisition, FILA was making a loss in China. ANTA was able to offer its expertise in the Chinese market and supply chain advantages. In return, FILA was able to be that high-end market entry point for ANTA. FILA now stands as its most successful acquisition, accounting for almost half of the group’s revenue.

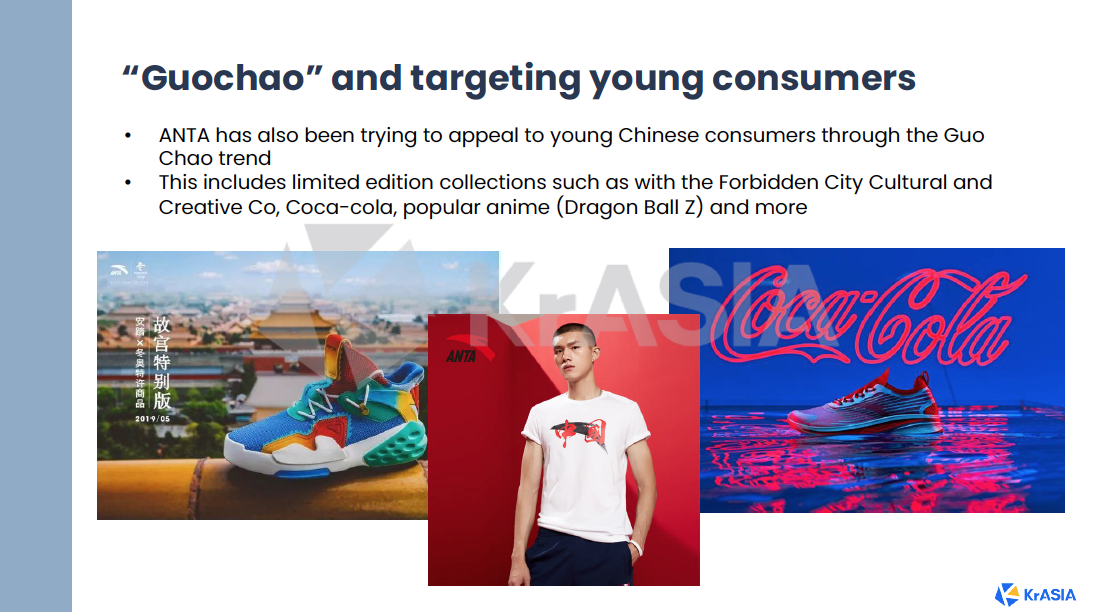

Other factors such as successful endorsements from superstar athletes and high-profile sponsorships have also further cemented ANTA’s position as the top domestic brand. Examples include signing with table tennis superstar Kong Linghui in 1999 and winning the bid with China’s Olympic committee for the period of 2009 – 2024. Getting onboard with the national trend, guo chao (国潮), has also raised its profile amongst young consumers.

ANTA subsequently acquired Amer Sports in 2019 for USD 5.15 billion, as a way to continue its growth and strengthen internationalisation efforts. To date, ANTA has more than 25 brands under its umbrella and hopes to achieve 10-15% CAGR in the next 5 years.

However, ANTA is likely to face challenges in the future. Domestically, it’s the question of can ANTA’s own brand grow or will it be outperformed by FILA or the other newly acquired brands? Additionally, how far can the D2C model take the company? On the international playing field, it remains to be seen if the investment into Amer Sports will play out the way ANTA hopes it will, like how it did with FILA, and does the group have the management capabilities to unify so many brands under a single vision?