Last week, Anghami became the first Arab technology company to announce that it’s going public through a listing on the Nasdaq in New York later this year after merging with a SPAC. As part of the deal, the company is expected to receive anywhere between USD 40 million and USD 210 million in cash from the SPAC and a separate PIPE investment.

Yes, I also had to reread this paragraph to digest it fully. What’s a SPAC, a PIPE, and why was this deal structured this way instead of like a traditional IPO route that most companies undertake when going public?

This piece aims to answer these questions and is split into two parts. The first is an overview of the music streaming industry and a deep dive into Spotify and Anghami’s strategies and paths towards profitability. The second section unpacks the Anghami SPAC deal and the fine print behind it.

Overview of music streaming

The conventional distribution model of music was disrupted in 1999 when Sean Parker unleashed peer-to-peer file-sharing and sucked profits out of the industry. To protect their profits, record labels sued Napster (Sean’s company) into bankruptcy. However, the genie was out of the bottle, and by 2008, 95% of music was downloaded illegally.

Around the time, Spotify and Pandora launched subscription-based streaming, which played a fundamental role in saving the industry and restoring some of its profits. Unfortunately, the lion’s share of profits remained with record labels, and streaming platforms struggled to turn profits and make their business model work.

The economics of music streaming

Streaming platforms make money through two main streams.

One is the premium model: charge customers a subscription fee for full ad-free access to content.

The other is the ad-based model: charge advertisers to target free users with ads on the platform.

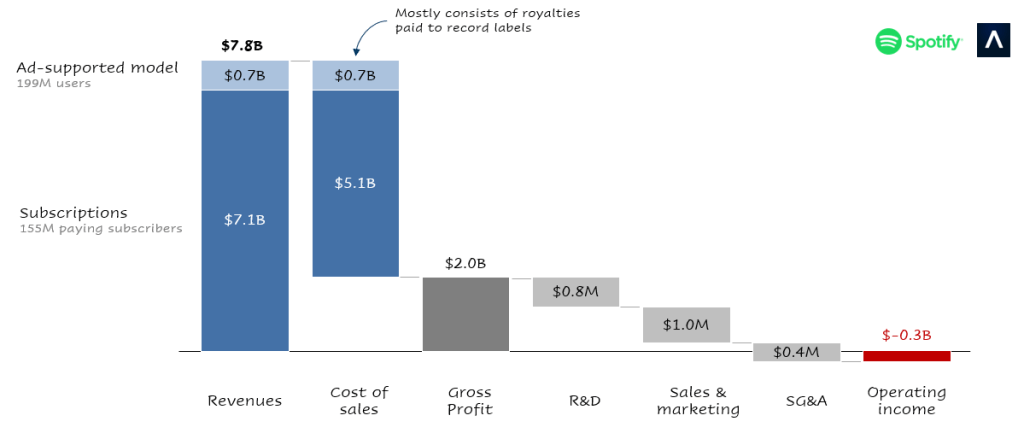

Platforms license music from record labels and pay them a small royalty fee whenever a user listens to one of their songs. In aggregate, these fees add up to around 70% of total revenues, which puts a massive strain on streaming platforms’ profitability. As a result, all streaming platforms lose money as their thin gross margins can’t cover their operational expenses (R&D, marketing, and SG&A costs).

With 155 million paying subscribers and 199 million free users, Spotify is the largest and most recognized independent music streamer. Yet the company has never turned a profit, and recently posted a USD 300 million loss on USD 7.8 billion of revenues.

Spotify: Podcasts as a moat

To overcome the high royalty fees and pave a sustainable path towards profitability, Spotify took a page out of Netflix’s book and turned its attention towards original content. Its new strategy was centered around two core pillars:

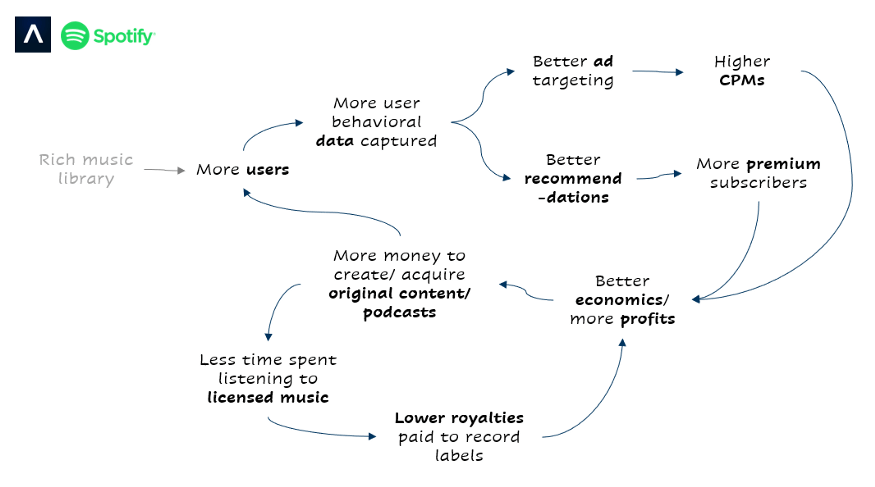

1) Podcasts: Spotify recently embarked on an acquisition spree to establish a podcast-centered ecosystem (The Ringer, Anchor, Parcast) and built a rich content library (featuring Joe Rogan, Kim Kardashian, Barack Obama). As podcasts capture a higher portion of users’ time, Spotify will pay lower royalties to record labels and improve its gross margins (if I listen to a podcast on my drive to work instead of a song, Spotify doesn’t have to pay royalties). Beyond royalty payments, podcasts are also proven to increase user retention and user conversion to premium.

2) Data: An average user spends 25 hours a month on Spotify, creating a ton of behavior data (Spotify collected 200 petabytes of user data up until 2018, compared to only 60 petabytes by Netflix by 2016). This data is used to improve recommendations (today, recommendations account for 30% of music streamed), leading to higher engagement and higher conversions to premium subscriptions. Data also improves ad targeting (better knowledge of users through which music or podcasts they listen to allows Spotify to serve them more relevant ads), which increases return on ad spend, enabling Spotify to charge higher rates from its advertisers.

Visually, Spotify’s flywheel looks something like this:

So far, the new strategy has been working. Spotify has gradually improved its gross margins (by around 100 basis points a year), and investor excitement towards the company has renewed. Its stock nearly doubled since April 2020 after showing no growth in the first two years since the company’s IPO.

Anghami: Regionally focused and lean

Founded in 2012 by Eddy Maroun and Elie Habib, Anghami is the first music streaming player in the Middle East. Since then, the company has built a strong regional footprint, adding 39,000 Arabic artists (600,000 songs) and 4 million international artists (56 million songs) to its platform, which it serves to its 8 million monthly active users.

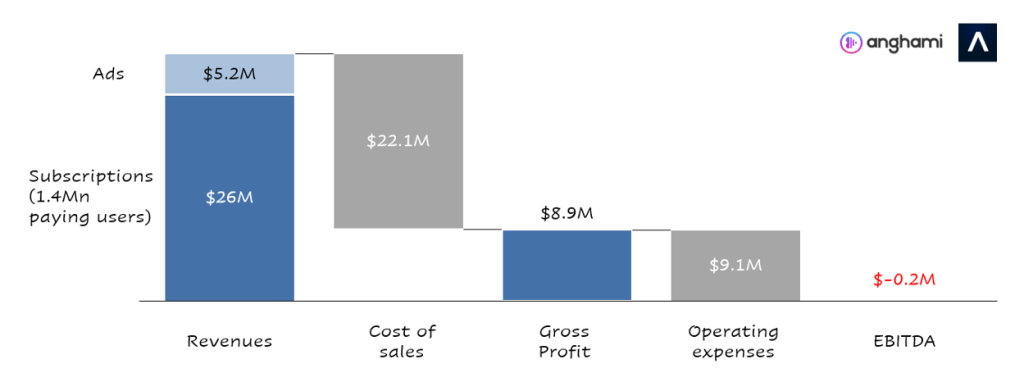

Similar to Spotify, Anghami has lost money since its inception. However, the company has been on a great trajectory over the past four years (2017–2020), as it has significantly improved unit economics by nearly doubling revenues, mostly through new premium subscriptions; increasing gross profits by 400%; and reducing EBITDA losses by 97%. In 2020, the company lost a mere USD 200,000 on USD 31 million of revenues.

Today, the company’s income statement looks like this:

Building on its strong footprint, partnerships with artists and telco providers, and its data, Anghami aspires to:

1) Triple its user base by 2023 by reinforcing its position in existing markets (mostly Egypt and Saudi Arabia) and expanding into new geographies (neighboring countries in South Asia except India and the Arab diaspora in the West).

2) Nearly double the share of paid subscribers from 17.5% today to 30% in 2023, while increasing ad revenues by fivefold through improved targeting.

3) Launch new revenue streams such as live radio, live concerts, and branded content.

Achieving these targets won’t be easy, especially if Anghami wants to do so while maintaining a sustainable competition position (instead of just focusing on growth). As such, the management team needs to keep an eye on four priorities:

Efficient marketing: As Spotify, Deezer, and others (YouTube, Apple, Amazon) expand their footprint in the region, the competitive rivalry between music streaming platforms will intensify. As a result, customer acquisition costs will likely spike, driven by higher marketing spend and more discounts, which will dilute profits across the board. Striking a balance between growth and profitability will remain a key challenge for Anghami. Thus, maintaining high marketing efficiency and a reasonable LTV/CAC (lifetime value/customer acquisition cost) ratio should be a priority.

Continuous product improvement: User engagement is one of the most important metrics in music streaming, given its influence on retention and user growth. To maintain high user engagement, Anghami should adopt a rapid product development cycle to upgrade its recommendation engine and bring new features to customers. The company should also regularly tweak its ad-targeting algorithms to maximize return on ad spend for its partnering brands.

Original Arabic content: Like Spotify, Anghami can’t solely rely on external content to drive its growth. It can’t also win focusing on foreign content. Instead, the Middle Eastern player should double down on its Arabic-first advantage and build or sponsor a rich library of original Arabic content (music and podcasts) catered to its core userbase (Arabic content accounts for 1% of Anghami’s catalog, but 50% of streams).

Focused and lean approach: Anghami paved a path towards profitability by focusing on a sustainable growth model and maintaining a lean structure. Costs related to geographical expansion, new product releases, and running a public company can run out of hand. The leadership team should stick to their previous way of doing things by maintaining a lean structure and adopting a very tactical approach to the technological and product bets they make. A focused, frugal approach remains the right one.

Most importantly, Anghami will need a lot of cash going forward to fund growth marketing, product innovation, and content creation.

Thus the SPAC.

Anghami’s SPAC deal

What’s a SPAC? What’s a PIPE?

The below is an excerpt from Sharif Farha’s primer on SPACs. Sharif is one of the region’s best consumer investors and was the first to draw my attention to the beauty of Spotify’s flywheel and the company’s potential. Check out his company deep-dives at safehousecap.com.

A Special Purpose Acquisition Company (SPAC) is a shell company that lists on the stock market with the goal of acquiring or merging with a private company. By acquiring or merging with a private company, that private company (or target) in turn becomes a publicly traded company.

Here’s an example:

1. “SPAC A” raises USD 100 million from investors at USD 10 per share.

2. “SPAC A” lists on the market with 10 million share.

3. “SPAC A” identifies an interesting company “Target” worth USD 1 billion.

4. “SPAC A” acquires 10% of “Target” for USD 100 million.

5. “Target” is now listed on the market and open to any investor to buy shares.

6. Investors in “SPAC A” have a choice of redeeming their shares and get their USD 10 back (the original share price) or get a share in “Target.”

Private investment in public equity (PIPE) is an instrument that public companies use to raise money from private investors. In the process, private investors receive shares in the company in exchange for the money they invest.

Companies elect to go public or raise money through a SPAC or a PIPE as opposed to conventional methods (IPOs or secondary offerings) for multiple reasons.

SPACs and PIPEs offer companies a quicker route to public markets, due to fewer regulatory requirements. SPACs and PIPEs grant companies more control over their valuation and share price, given they negotiate with one entity. SPACs and PIPEs tend to have lower transaction costs than IPOs. Going public through an IPO would require the company’s management team to go on roadshows to pitch the company to investors, thus distracting them from running the business.

Details of Anghami’s SPAC

As part of the deal, Anghami will receive cash through two separate instruments:

1) VMAC special purpose acquisition corporation (SPAC), a publicly listed entity that has raised USD 100 million in cash from investors. The final amount of money given to Anghami will depend on the number of investors that redeem their shares for cash (see point 6 in the example above). Therefore, Anghami can receive anywhere between zero dollars (if all investors are unhappy with the deal and decide to redeem their shares) and USD 100 million (if all investors decide to go through with the deal and turn their shares into Anghami shares).

2) Private investment from external investors in the form of a PIPE (private investment in public equities) of up to USD 110 million. Shuaa Capital and Vistas Media Capital (parent of VMAC) are leading the PIPE raise and have already gathered commitments of USD 40 million. As such, Anghami expects anywhere between USD 40 million (already committed) and USD 110 million (target amount) through this PIPE.

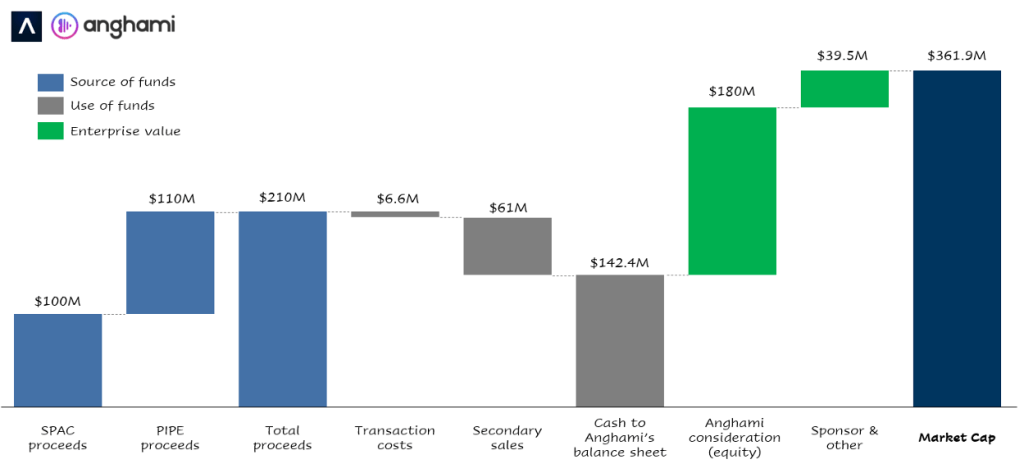

As such, the deal’s total proceeds could fall anywhere between USD 40 million (assuming all SPAC investors redeem their shares and PIPE commitments remain at USD 40 million) and USD 210 million (assuming no SPAC investor redeems their share and PIPE commitments increase to the target of USD 110 million).

Proceeds will be partly used to cover the transaction cost, estimated at USD 6.6 million, as well as pay existing investors that wish to sell some of their shares (secondary sales). The secondary sales size is expected to range from USD 11 million (if proceeds are limited to USD 40 million) to USD 61 million (if proceeds equal USD 210 million).

The remaining cash (USD 142.4 million in the best case) will be given to Anghami’s management team to fund the company’s initiatives.

In this deal, Anghami’s Enterprise value was set at around USD 220 million, valuing the company at seven times enterprise value over 2020 sales, a slight premium to Spotify’s current six time enterprise value over 2020 sales (albeit, Spotify’s stock price recently dropped 25% following the recent growth stocks sell-off).

Adding the cash received to the company’s enterprise value yields a market cap of USD 361.9 million (assuming all USD 210 million is received).

Overall, the deal structure looks like this:

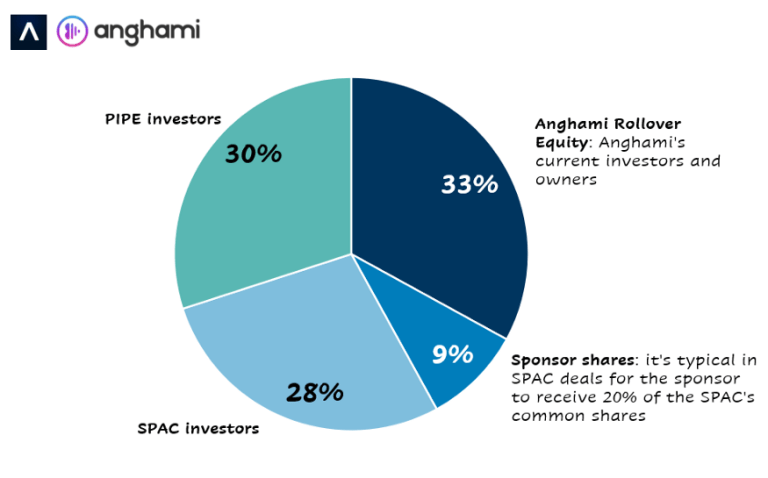

Following the deal closing, Anghami’s ownership structure will look like this:

I hope this piece helped answer some of your questions on a pivotal moment for our region. Feel free to reach out if you’d like to discuss further.

This article was written by Imad El Fay. It was first published by MENAbytes.