June 29, 2020, saw a true rarity in the capital markets.

At 9:30 am, just as the Shanghai Stock Exchange’s market-opening gong was about to ring, 72-year old Gan Zhongru, was beside himself with excitement in anticipation of his company’s public offering.

As the founder of Gan & Lee Pharmaceutical, the first Chinese company that managed to master the technology for the industrialized production of recombinant insulin analogues, his team had made China one of the few countries around the world capable of such production.

Almost simultaneously, the gongs of the Hong Kong Stock Exchange rung again to welcome the listing of more two giants. China’s largest oncology medical group, Hygeia Medical, and China’s largest minimally invasive surgical instruments and accessories group, Kangji Medical, both made their debuts on the Hong Kong Stock Exchange as well.

With three giants listing on the same day, the Chinese medical industry had reached fever-pitch in a sight unseen for several years. This abundance of listings was not only a feast for Chinese medical industry insiders but also, for the bevy of top venture capital (VC) and private equity (PE) firms that had placed their bets on Chinese medical care.

Star-studded players such as Qicheng Venture Capital, Warburg Pincus, TPG, Boyu Capital, CITIC Capital, and Huagai Capital had all struck jackpot on this front.

In recent years, the capital markets in China have been on a general decline. The counter-cyclical nature of the medical industry has therefore held a constant appeal to VCs and PEs.

Was the explosion of IPOs in 2020 therefore, an inevitability? How should one confront the problem of overinflated valuations in the primary market? Can investing in the medical industry truly be a panacea for VC and PE risk-hedging strategy?

Bounty crop for companies and financiers alike

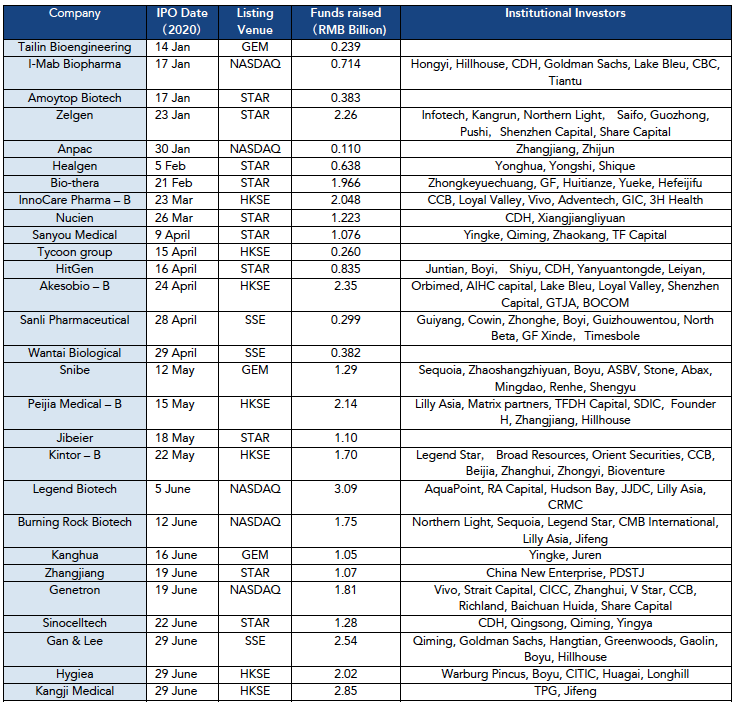

According to data from CVSource, there were 28 medical companies that listed in the first half of 2020, a 155% increase compared to the 11 that listed in the same period of 2019.

Institutional shareholders all scored when it came to IPO exits. CDH Investments attained 4 IPOs and remains the biggest winner. Following closely behind were Qiming Venture Capital, Hillhouse Capital, and Boyu Capital, each scoring 3 IPOs.

Sequoia China, Northern Light Venture Capital, Legend Star, Highlight Capital, Jifeng Capital, Loyal Valley Capital, and Lake Bleu Capital each scored 2 IPOs.

Rumour is that the return on investment (ROI) for those lucky investors that got in during the early stages of some of these companies may be more than 50 times.

Fertile groundwork generated a listing explosion

Liang Yongyu, head partner of Qiming Venture Capital, believes that the sudden explosion in medical industry IPOs sends a strong signal to investors.

“This phenomenon was mainly due to the reform of listing regimes for the Hong Kong Stock Exchange, the Growth Enterprise Market (GEM) board, and the Science and Technology Innovation (STAR) Board,” said Liang, referring to three popular stock exchanges available in the domestic market. “Listing using A-shares and H-shares is an ideal channel for medical companies, and is a positive signal to investment institutions.”

Fang Min, a partner at Warburg Pincus, also mentioned the positive effects wrought by policy changes. “The reform of the listing regime also makes it easier for the secondary market to accept emerging medical companies.”

In addition, Fang Min also mentioned that major reforms to the medical industry in recent years have broken the shackles of an older, obsolete system, and enabled long-term positive trends for the healthy development of the industry to take off.

This is evinced by how over the past decade, a large number of innovative and entrepreneurial medical companies have sprung up in China. Many of them have been supported by funds from the primary market and have now blossomed into full-fledged, listed enterprises of their own.

COVID-19 pandemic an obvious accelerator

In addition to the twin drivers of policy reform and counter-cyclical hedging, the sudden advent of the global COVID-19 pandemic has accelerated this phenomenon of medical industry listings.

“The emergence of the virus has made the public more mindful of healthcare investment. In addition, the counter-cyclical nature of the healthcare industry is also especially appealing in an uncertain economic environment,” Fang Min explained.

“Therefore, the secondary markets are particularly interested in the listing of medical companies.”

Demand from the secondary market has directly translated into the explosive popularity of medical industry listings in the primary market.

According to CVSource, VC and PE activity generally declined in May 2020. The number of investments decreased by 23% month-on-month and experienced a 60% decrease compared to the same period in 2019. Despite this slowdown in investment activity, the medical industry is still a hotspot of investment, leading all industries in terms of transaction volume.

In addition, large-scale investments occur more frequently, while the average value of investments is also increasing significantly.

“Since 2020, the amount of funds put towards new investment projects has increased. For instance, the amount invested towards a single project has increased by about 50%,” said Wu Pingqing*, a managing director of a well-known VC.

“Capital will be simultaneously more scarce, and more in search of true industry leaders. The core competitiveness of investments will be tested and investors will have higher requirements for funding. The COVID-19 situation has not affected our tempo, but has instead, made our process more firm and decisive.”

Has the golden age for medical investments passed?

With enthusiasm in medical investments reaching fever-pitch, one could be forgiven for feeling skeptical about this craze. Much like the gold rush of the 1800s, many VCs and PEs are now clamoring to get a piece of this potentially lucrative pie.

“We feel that many investors are now competing very fiercely for projects,” said Fang Min, attesting to this craze. “The explosion in the number of medical IPOs will definitely attract more primary market funds into this industry.”

However, the charm of the capital markets lies in its ability to prove ripened bets on future trends. Once a trend has become apparent to all, mature players may have already entered and reaped their rewards. This could signify that the golden age for a winning investment may have already passed.

After all, the fierce competition for medical-industry projects by VCs and PEs has already led to a significant increase in valuations.

Fang Min, who has worked at Warburg Pincus for 13 years, bluntly explained that his team sometimes had to give up investing in overvalued projects.

Based on his experience, entry at different stages of an industry’s valuation cycle leads to large differences in final investment returns.”For latecomers in medical investments, my advice is not to blindly pursue short-term returns but do solid industry research. You need to have long-term investment expectations from day 1 of investment,” Fang Min emphasized.

Wu Pingqing suggested that the current situation in China’s stock markets is somewhat reminiscent of Nasdaq 30 years ago, with no stakeholders really knowing how to judge a proposed valuation.

Ultimately, however, the true test of valuation will depend on a company’s ability to generate cash flow. Therefore, a well-oiled ecosystem should be able to score capital to support its further growth.

Survival of the fittest potentially culls unproven contenders

Several seasoned investors have stated that based on the idea of maximizing value, their investment teams will prioritize companies whose products have already been on the market for a certain amount of time, and which have a certain potential market size.

This is because even under normal circumstances, early-stage projects in R&D or clinical stages require huge amounts of funds to sustain, a situation which is further exacerbated by a high uncertainty in success or failure.

Yu Zhengkun, the founding partner of Jifeng Capital, however, believes that if early-stage and unproven projects are indeed technically innovative and meet clinically unmet needs, it is possible to make investments in them. “However, the proportion of such projects will be controlled to within 20% of our portfolio.”

The difficulty of investing in unproven medical investments is exacerbated by limited partners’ (LP) pressures.

“It is difficult to raise funds in the market now and we still need to account for LPs. Therefore, we do not dare to rush to invest in medical companies that have no income, or long return periods. This is even if I am personally certain that a company will be able to succeed in the future,” said Liu Kai*, fund manager focusing on medical investments.

When probed about whether he regrets this situation, Liu thought for a few seconds.

“No regrets. Choosing the best of the best, and survival of the fittest is the very first law of the venture capital circle.”

Betting on the medical industry is not a magic bullet

Even with capital support, however, China’s medical industry still has a long way to go.

Liang Yongyu recalled that Gan Zhongru, the founder of Gan & Lee Pharmaceutical, was well known for frequently saying that almost all industries in China had caught up with (or far exceeded) those of foreign countries, with the distressing exception of the pharmaceutical industry.

“When the domestic market first opened up, foreign companies selling medicine in the mainland domestic funds were also required to account for 51% of shares in joint ventures. However, some foreign-funded pharmaceutical companies only took up shareholdings in name and did not really introduce new technology to China,” Gan once said.

Consequently, Gan has always regarded technological innovation as a core driver of Gan & Lee Pharmaceutical. He believes that this is key to winning over the Chinese medical market. However, placing bets on the medical industry is not necessarily a long-term risk-free bet for advisors.

‘The medical industry is composed of multiple, non-synchronized, sub-sectors, and each sub-sector has its own particular characteristics and development cycle,” Fang Min explained.

“As an investment institution, we need to accurately grasp and analyze the development points of each specific sub-sector. We also need to pick from specific projects across specific timings. Only by maximizing rational decisions can we truly achieve excellent returns on investment that can withstand economic cycles.”

Capital markets are learning to be patient

On the whole, China’s domestic pharmaceutical industry will take a long time to come to fruition. Investors will, therefore, need to learn patience —a virtue especially prized in the medical industry, which values accuracy over speed.

Wang Mingyao, the general manager and managing partner of Lenovo Star, once echoed similar thoughts. “Although the development of medical projects is slower, the money we invest will generate real R&D results. Even if a drug’s Phase III clinical trials do not succeed, results can be obtained from Phase I and Phase II, so we are not returning to square one. In this way, we are also considered winners.”

In other words, the capital markets, which prioritize speed, are gradually coming to accept the relative slowness of the medical industry.

From Fang Min’s point of view, the development of the medical industry is a long-term trend with firm fundamentals. As long as investing institutions have a good grasp of the fundamentals, they can maintain their long-term advantage over the ebbs and flows of the economic cycle.

“We strongly believe that the next area where we will see BAT-like companies (Referring to Baidu, Alibaba, and Tencent) is likely to be the medical industry,” said Liu Kai.

“The market consensus is that healthcare is a sunrise industry. As long as there are medical companies with investment potential, the capital markets will rise to their needs.”

*At Liu Kai and Wu Pingqing’s requests, their real names have been changed to preserve anonymity.

The original article was written by Chai Jiayin for China Venture and published by 36Kr. The English version was adapted by Lin Lingyi.