Chinese tech giant Tencent test launched and abruptly scrapped its credit scoring service over a short period of two days, signifying Beijing is tightening its control over local social credit reporting services.

The service, available by following a public account named “Tencent Credit” on WeChat, was officially launched on January 30 and was taken down on the night of January 31 in a rush.

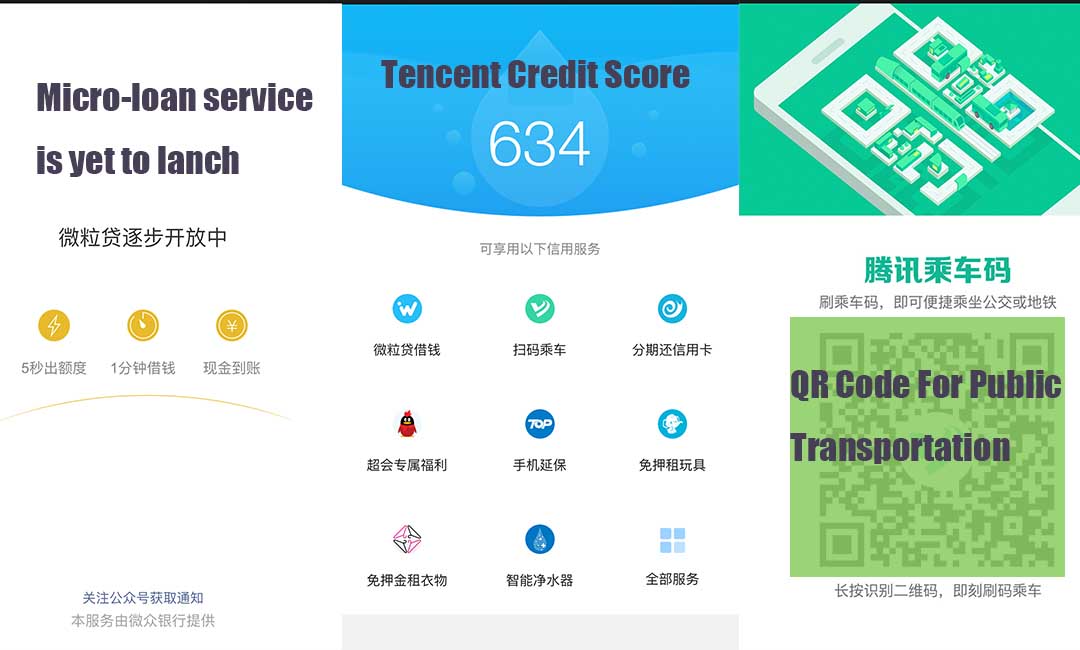

Accessing the service now will only prompt a message reading “Hello, thanks for following Tencent Credit. The nationwide limited-time public testing is now closed, thanks for your participation.”

Previously, Tencent has been doing similar but smaller scale tests in a handful of Chinese cities, gauging user feedbacks for tweak-up.

According to local media reports, Chinese authorities brought Tencent’s water testing to an immediate halt over concerns that a large armada of online lenders have been leveraging on credit-scoring services, such as Alibaba’s Sesame Credit, to market suspicious financial products.

China’s central bank, PBoC, initiated a pilot of Internet-based social credit reporting in 2015 to tap into the help from local businesses, including Alibaba, Tencent, and Ping An, which own a wealth of personal transaction data that are usually indicative of one’s creditworthiness. The initiative is part of the country’s push to extend financial services to Chinese with no collateral or proper credit history.

Holding the central bank’s olive branch, Alibaba officially launched its Sesame Credit system the same year, which banks on the Hangzhou e-commerce behemoth’s wide access to online consumers and has outpaced its rivals to become the most popular tech credit system in China.

Alibaba’s Sesame Credit has a score for everyone ranging from 350 to 950 points. The score is calculated by measuring five factors: credit history, behavior preference, fulfillment ability, personal characteristics and relationships. Scoring high on Sesame would entitle one to rewarding services such as, renting a shared bike with no deposits (ranging from RMB 99 yuan to 299 yuan, or between US$ 16 and US$ 48) required.

In addition to renting a bunch of things devoid of upfront payment, high scores also give one eligibility for faster and easier online loans.

And that’s what has been worrying China’s regulatory bodies.

In recent years, credit score has been tapped by online lenders to judge trustworthy borrowers, small businesses and individuals alike, which is a good move for those who are out of China’s formal banking system.

According to iResearch, around 160 million Chinese netizens borrowed RMB 1.2 trillion yuan (US$ 174b) from online channels in 2016. And the business of online financing was expected to grow 10% per year over next three years.

However, such breakneck growth was partially bolstered by some lenders’ illicit and (purposely) careless leverage of credit systems to sell potentially risky products to online borrowers that might cause widespread defaults.

For example, NYSE-listed Qudian, backed by Alibaba, which specializes in micro-loans, was accused of exploiting student and blue-collar customers in addition to selling customers’ personal information.

Yet calling off Tencent’s credit service is not the only and ultimate remedy for Beijing to safeguard against defaults. Keep developing, instead of curbing, a more accurate and comprehensive social credit system, goes a longer way to addressing such concerns and granting credit access to trustworthy but unorthodox borrowers.